Advertisement

- United States

- /

- Hospitality

- /

- NYSE:LVS

Analysts Just Shaved Their Las Vegas Sands Corp. (NYSE:LVS) Forecasts Dramatically

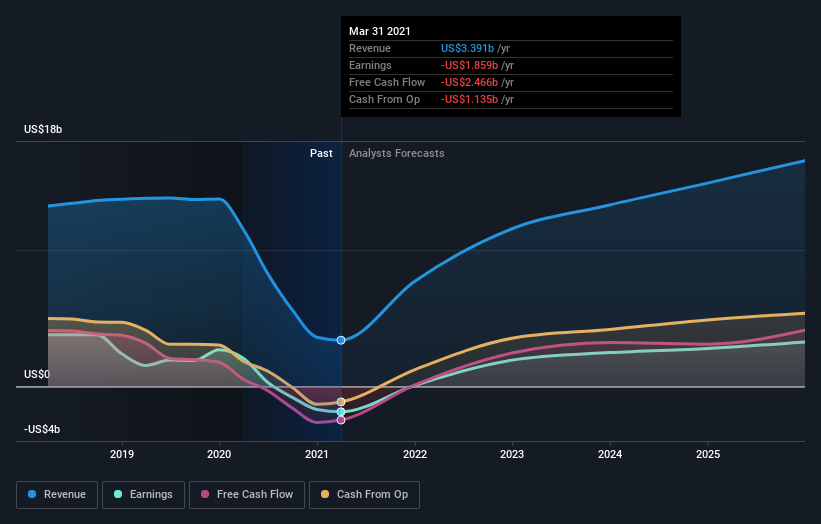

The latest analyst coverage could presage a bad day for Las Vegas Sands Corp. (NYSE:LVS), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. Both revenue and earnings per share (EPS) estimates were cut sharply as the analysts factored in the latest outlook for the business, concluding that they were too optimistic previously.

After this downgrade, Las Vegas Sands' 14 analysts are now forecasting revenues of US$7.5b in 2021. This would be a sizeable 122% improvement in sales compared to the last 12 months. Losses are predicted to fall substantially, shrinking 99% to US$0.024. Prior to this update, the analysts had been forecasting revenues of US$8.5b and earnings per share (EPS) of US$0.42 in 2021. So we can see that the consensus has become notably more bearish on Las Vegas Sands' outlook with these numbers, making a substantial drop in this year's revenue estimates. Furthermore, they expect the business to be loss-making this year, compared to their previous forecasts of a profit.

View our latest analysis for Las Vegas Sands

There was no major change to the consensus price target of US$67.57, signalling that the business is performing roughly in line with expectations, despite lower earnings per share forecasts. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. The most optimistic Las Vegas Sands analyst has a price target of US$86.50 per share, while the most pessimistic values it at US$53.50. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

Of course, another way to look at these forecasts is to place them into context against the industry itself. One thing stands out from these estimates, which is that Las Vegas Sands is forecast to grow faster in the future than it has in the past, with revenues expected to display 189% annualised growth until the end of 2021. If achieved, this would be a much better result than the 9.1% annual decline over the past five years. Compare this against analyst estimates for the broader industry, which suggest that (in aggregate) industry revenues are expected to grow 22% annually. So it looks like Las Vegas Sands is expected to grow faster than its competitors, at least for a while.

The Bottom Line

The biggest low-light for us was that the forecasts for Las Vegas Sands dropped from profits to a loss this year. Unfortunately, analysts also downgraded their revenue estimates, although our data indicates revenues are expected to perform better than the wider market. We're also surprised to see that the price target went unchanged. Still, deteriorating business conditions (assuming accurate forecasts!) can be a leading indicator for the stock price, so we wouldn't blame investors for being more cautious on Las Vegas Sands after the downgrade.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for Las Vegas Sands going out to 2025, and you can see them free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you decide to trade Las Vegas Sands, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NYSE:LVS

Las Vegas Sands

Owns, develops, and operates integrated resorts in Macao and Singapore.

Very undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|40.2% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|62.7% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.1% undervalued

UN

Community Contributor