Advertisement

- United States

- /

- Hospitality

- /

- NYSE:EAT

Brinker International, Inc.'s (NYSE:EAT) P/E Is Still On The Mark Following 29% Share Price Bounce

Brinker International, Inc. (NYSE:EAT) shareholders would be excited to see that the share price has had a great month, posting a 29% gain and recovering from prior weakness. The annual gain comes to 144% following the latest surge, making investors sit up and take notice.

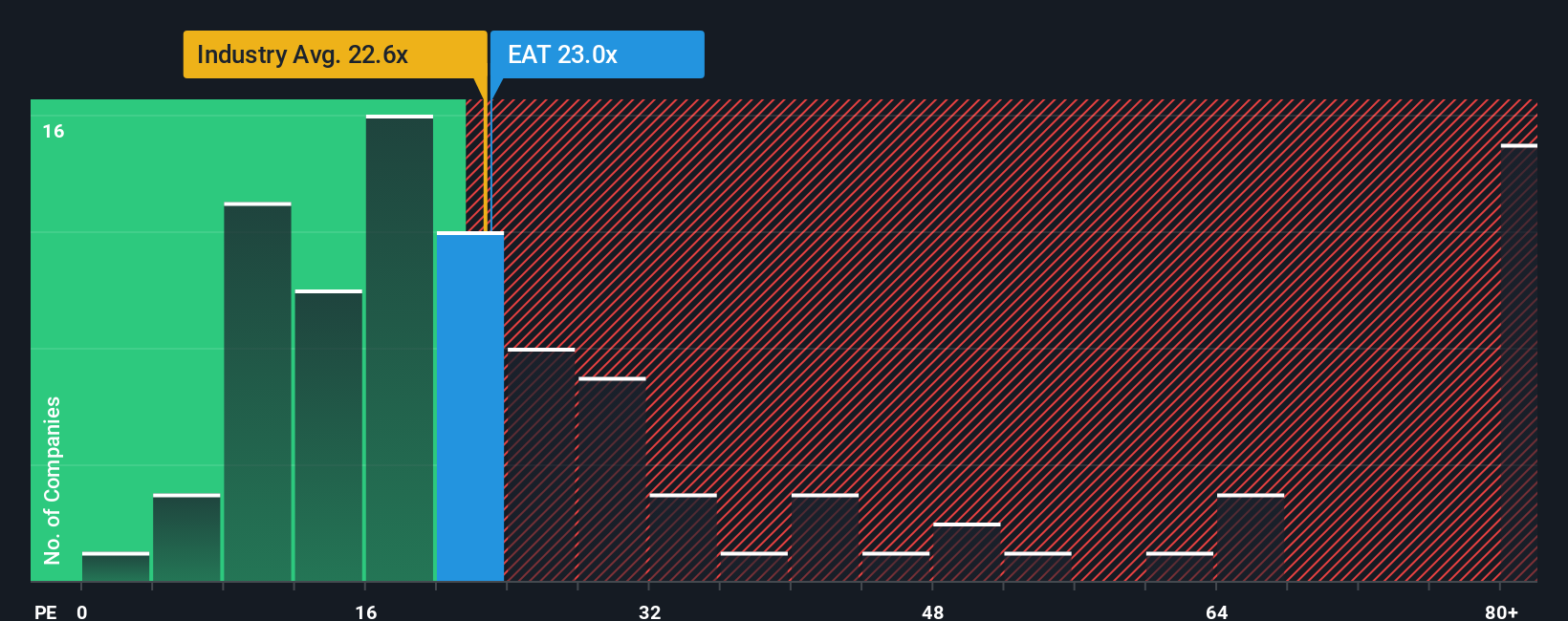

Following the firm bounce in price, Brinker International may be sending bearish signals at the moment with its price-to-earnings (or "P/E") ratio of 23x, since almost half of all companies in the United States have P/E ratios under 17x and even P/E's lower than 10x are not unusual. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

With earnings growth that's superior to most other companies of late, Brinker International has been doing relatively well. The P/E is probably high because investors think this strong earnings performance will continue. If not, then existing shareholders might be a little nervous about the viability of the share price.

View our latest analysis for Brinker International

How Is Brinker International's Growth Trending?

The only time you'd be truly comfortable seeing a P/E as high as Brinker International's is when the company's growth is on track to outshine the market.

If we review the last year of earnings growth, the company posted a terrific increase of 118%. Pleasingly, EPS has also lifted 124% in aggregate from three years ago, thanks to the last 12 months of growth. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 27% over the next year. That's shaping up to be materially higher than the 13% growth forecast for the broader market.

With this information, we can see why Brinker International is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Final Word

Brinker International shares have received a push in the right direction, but its P/E is elevated too. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Brinker International maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for Brinker International that you should be aware of.

You might be able to find a better investment than Brinker International. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Brinker International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:EAT

Brinker International

Owns, develops, operates, and franchises casual dining restaurants in the United States and internationally.

Very undervalued with outstanding track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|26.1% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|21.3% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|61.2% undervalued

ME

Community Contributor