Advertisement

- United States

- /

- Hospitality

- /

- NYSE:DRI

Does the Recent Slide Signal Opportunity for Darden Restaurants in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

If you have been watching Darden Restaurants and wondering whether now is the time to make a move, you are not alone. Investors have seen the stock come under pressure in recent weeks, sliding 6.2% over just the past seven days, and down 14.3% for the month. It is enough to give even the most seasoned shareholders pause, especially after an otherwise solid run. Darden shares are up 19.1% over the last year, and an impressive 114.4% when you look back five years.

Some of this recent weakness can be traced to shifting market sentiment around the restaurant sector as a whole, with investors weighing economic signals and looking for companies that can both grow and defend their margins. Still, dips like this are sometimes exactly the moments savvy investors look for. Darden’s long-term growth picture is hardly in doubt, and when the numbers are compared to its peers, the valuation story becomes even more compelling.

By the metrics used to judge how undervalued a company is, Darden checks five out of six boxes, giving it a robust valuation score of 5 out of 6. That is a strong signal, but as you will see, there is more to the valuation puzzle than just these methods alone. Next, we will break down the different valuation approaches and then explore an even smarter way to understand what Darden is really worth.

Approach 1: Darden Restaurants Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's true worth by projecting its future cash flows and then discounting those sums back to today's dollars. In essence, it asks: if you owned Darden Restaurants and collected all its expected future cash flow, what would that be worth right now?

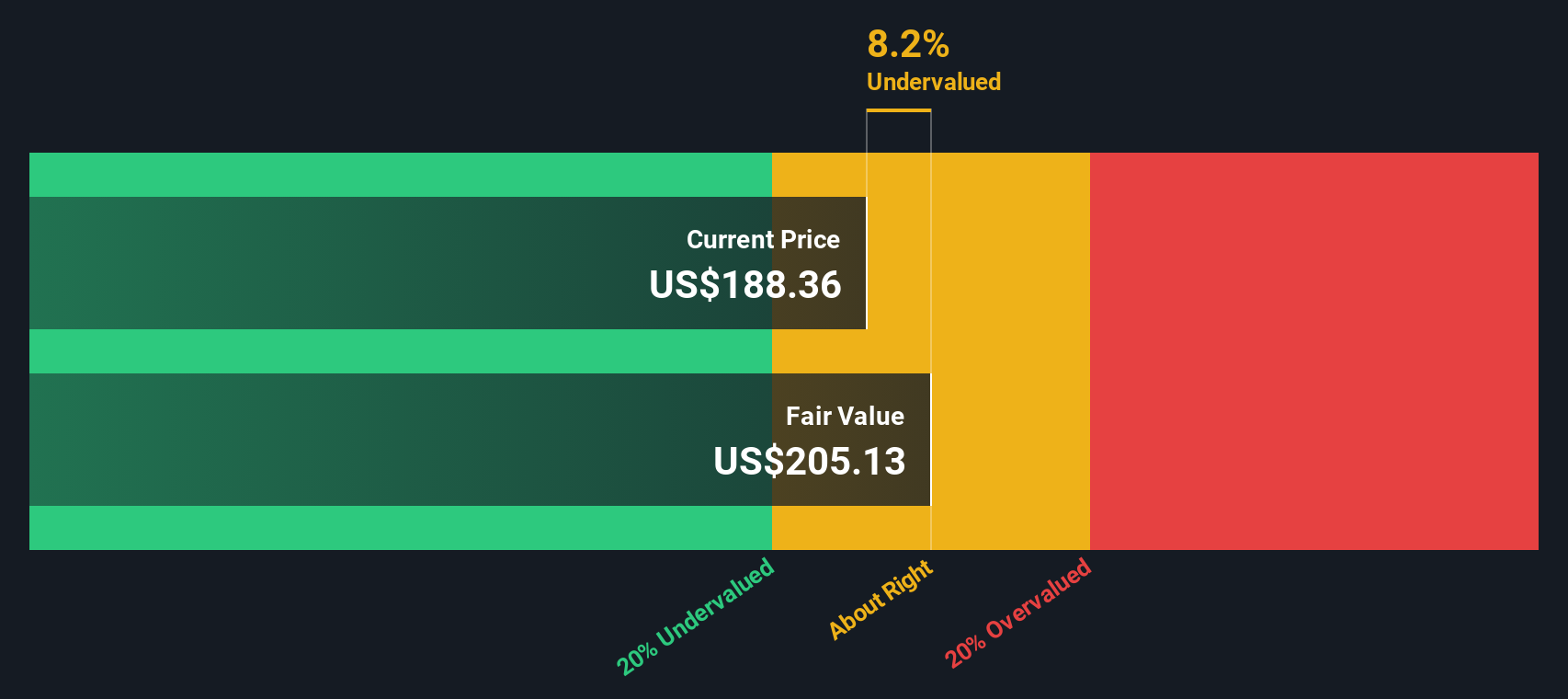

Darden's most recent reported Free Cash Flow stands at $1.07 billion. Analysts anticipate this number will continue to grow over the coming years, projecting a Free Cash Flow of $1.43 billion by 2028. While analyst insights cover only the first five years, additional forecasts using reasonable growth rates extend all the way to 2035. This long-term view is crucial in hospitality, where steady cash generation makes future projections valuable.

After extrapolating all these projections and discounting them to today's value, the model arrives at an intrinsic fair value of $205.47 per share. This figure suggests Darden Restaurants stock is currently priced 11.8% below its estimated true value, signaling an attractive entry point for investors seeking undervalued opportunities.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Darden Restaurants is undervalued by 11.8%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

Approach 2: Darden Restaurants Price vs Earnings

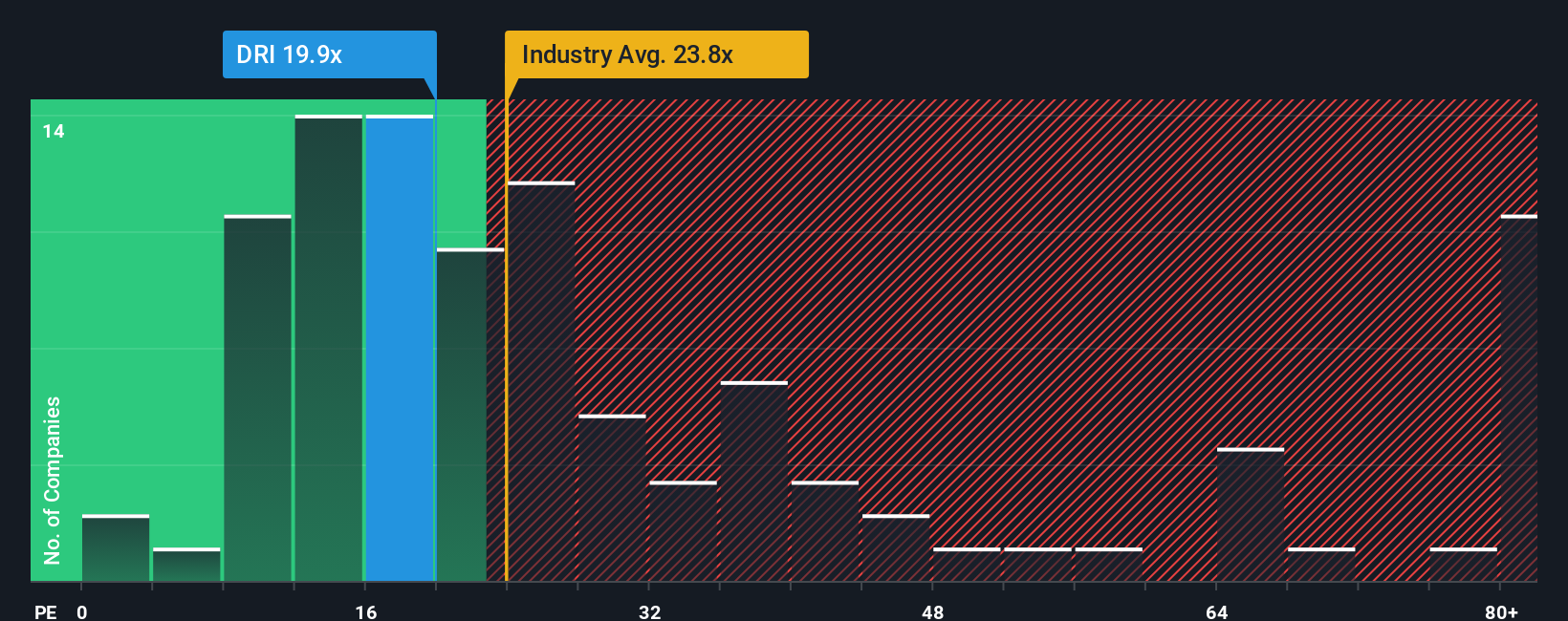

The Price-to-Earnings (PE) ratio is a popular metric for valuing profitable companies like Darden Restaurants because it connects a business’s market value directly to its bottom line earnings. When a company consistently generates profits, as Darden does, comparing its share price to earnings gives a clear window into how much investors are paying for each dollar of profit.

What constitutes a “normal” or “fair” PE ratio depends on a few key factors, such as how quickly earnings are expected to grow in the future and how much risk there is in the business. Companies with stronger growth prospects or lower risk often command higher PE ratios, while those facing slower growth or greater uncertainties tend to trade at lower multiples.

Darden Restaurants currently trades on a PE ratio of 19.1x. This is noticeably lower than the hospitality industry average of 23.1x and also below the average for similar peers, which sits at 23.2x. However, rather than just comparing to industry or peer averages, Simply Wall St uses a “Fair Ratio” approach. This method tailors the expected PE multiple for Darden specifically based on its earnings growth outlook, profit margins, market cap, and sector risks. For Darden, this Fair Ratio is calculated at 24.1x, a robust benchmark that takes far more context into account than a simple average.

The Fair Ratio provides a smarter baseline than industry averages because it accounts for Darden’s unique combination of prospects, profitability, and risks relative to the broader market and its direct competitors. By examining these factors, it offers a more informed view of whether the current multiple reflects the company’s fair value.

With Darden’s actual PE ratio of 19.1x sitting well below the Fair Ratio of 24.1x, the stock appears solidly undervalued on this metric.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Darden Restaurants Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is simply your unique perspective on a company’s future, your story about what will drive its business and what you think that means for its fair value and growth.

While metrics like DCF and PE offer valuable snapshots, Narratives go further by linking a company’s real-world story, such as innovations or challenges, directly to a dynamic financial forecast that updates as new information emerges. With Narratives, investors on Simply Wall St’s Community page can easily outline their reasoning, set their own assumptions for revenue, margins, and multiples, and instantly see how that translates to a fair value. This makes it an accessible and powerful tool used by millions of investors.

Narratives help you cut through the noise when deciding whether to buy, hold, or sell a stock, by comparing your calculated Fair Value to the current price and highlighting when your story signals opportunity or caution. They automatically update when relevant news or earnings are released, so your valuation is always fresh and relevant.

For example, some Darden investors believe new formats and tech partnerships will fuel rapid growth, assigning a fair value as high as $255 per share. Others worry about margin pressures and weak guest counts, valuing the company as low as $157. This demonstrates how Narratives make every investment decision personal, flexible, and more informed.

Do you think there's more to the story for Darden Restaurants? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:DRI

Darden Restaurants

Owns and operates full-service restaurants in the United States and Canada.

Undervalued average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor