- United States

- /

- Hospitality

- /

- NasdaqGS:DPZ

Domino's Pizza, Inc. Just Recorded A 5.4% EPS Beat: Here's What Analysts Are Forecasting Next

Investors in Domino's Pizza, Inc. (NYSE:DPZ) had a good week, as its shares rose 10.0% to close at US$529 following the release of its first-quarter results. The result was positive overall - although revenues of US$1.1b were in line with what the analysts predicted, Domino's Pizza surprised by delivering a statutory profit of US$3.58 per share, modestly greater than expected. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Domino's Pizza after the latest results.

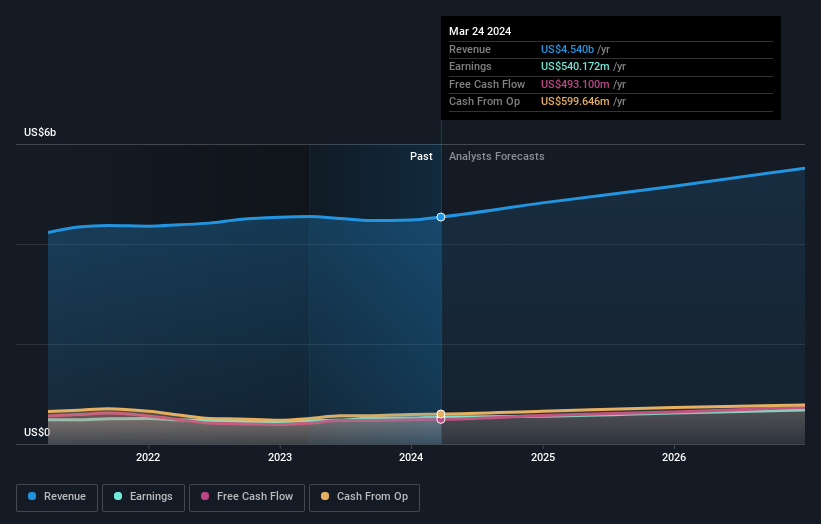

View our latest analysis for Domino's Pizza

Taking into account the latest results, the current consensus from Domino's Pizza's 29 analysts is for revenues of US$4.82b in 2024. This would reflect a reasonable 6.2% increase on its revenue over the past 12 months. Statutory earnings per share are predicted to increase 2.4% to US$15.89. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$4.81b and earnings per share (EPS) of US$15.78 in 2024. The consensus analysts don't seem to have seen anything in these results that would have changed their view on the business, given there's been no major change to their estimates.

The consensus price target rose 8.1% to US$536despite there being no meaningful change to earnings estimates. It could be that the analystsare reflecting the predictability of Domino's Pizza's earnings by assigning a price premium. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on Domino's Pizza, with the most bullish analyst valuing it at US$626 and the most bearish at US$425 per share. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

Of course, another way to look at these forecasts is to place them into context against the industry itself. The analysts are definitely expecting Domino's Pizza's growth to accelerate, with the forecast 8.4% annualised growth to the end of 2024 ranking favourably alongside historical growth of 5.7% per annum over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 9.8% annually. Domino's Pizza is expected to grow at about the same rate as its industry, so it's not clear that we can draw any conclusions from its growth relative to competitors.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with the analysts reconfirming that the business is performing in line with their previous earnings per share estimates. They also reconfirmed their revenue estimates, with the company predicted to grow at about the same rate as the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

With that in mind, we wouldn't be too quick to come to a conclusion on Domino's Pizza. Long-term earnings power is much more important than next year's profits. We have forecasts for Domino's Pizza going out to 2026, and you can see them free on our platform here.

That said, it's still necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Domino's Pizza , and understanding them should be part of your investment process.

If you're looking to trade Domino's Pizza, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:DPZ

Domino's Pizza

Operates as a pizza company in the United States and internationally.

Solid track record average dividend payer.

Similar Companies

Market Insights

Community Narratives