- United States

- /

- Consumer Services

- /

- NYSE:DAO

3 US Growth Companies With High Insider Ownership That Insiders Favor

Reviewed by Simply Wall St

As U.S. markets navigate a period of uncertainty with the Federal Reserve maintaining interest rates and investors closely watching major tech earnings, attention turns to identifying promising growth opportunities. In such a climate, companies with high insider ownership can be appealing, as they often signal confidence from those most familiar with the business's potential.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Atour Lifestyle Holdings (NasdaqGS:ATAT) | 26% | 25.2% |

| Super Micro Computer (NasdaqGS:SMCI) | 14.4% | 24.3% |

| On Holding (NYSE:ONON) | 19.1% | 29.7% |

| Kingstone Companies (NasdaqCM:KINS) | 20.8% | 24.9% |

| Clene (NasdaqCM:CLNN) | 21.6% | 59.1% |

| BBB Foods (NYSE:TBBB) | 22.9% | 40.4% |

| Credit Acceptance (NasdaqGS:CACC) | 14.1% | 48% |

| Smith Micro Software (NasdaqCM:SMSI) | 23.9% | 85.4% |

| Neonode (NasdaqCM:NEON) | 22.6% | 110.9% |

| CarGurus (NasdaqGS:CARG) | 16.6% | 42.3% |

Let's uncover some gems from our specialized screener.

Alphatec Holdings (NasdaqGS:ATEC)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Alphatec Holdings, Inc. is a medical technology company specializing in the design, development, and advancement of technologies for the surgical treatment of spinal disorders globally, with a market cap of approximately $1.62 billion.

Operations: The company's revenue is primarily derived from its Medical Products segment, which generated $572.74 million.

Insider Ownership: 11.9%

Revenue Growth Forecast: 14.9% p.a.

Alphatec Holdings is poised for growth, with insider ownership aligning interests with shareholders. The company expects significant revenue growth of approximately 20% in 2025, reaching US$732 million. Despite a volatile share price and current losses, Alphatec is forecast to become profitable within three years and shows strong earnings potential with an expected annual profit growth of 53.6%. Trading at a substantial discount to its estimated fair value also suggests good relative value compared to peers.

- Take a closer look at Alphatec Holdings' potential here in our earnings growth report.

- Our expertly prepared valuation report Alphatec Holdings implies its share price may be lower than expected.

Clover Health Investments (NasdaqGS:CLOV)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Clover Health Investments, Corp. offers Medicare Advantage plans in the United States and has a market cap of approximately $2.30 billion.

Operations: Clover Health Investments generates revenue through its provision of Medicare Advantage plans in the United States.

Insider Ownership: 21.6%

Revenue Growth Forecast: 10.4% p.a.

Clover Health Investments is positioned for potential growth, with insider ownership aligning interests. The company reported a reduced net loss of US$9.16 million for Q3 2024, down from US$41.47 million the previous year, indicating improving financials. Revenue is projected to grow at 10.4% annually, surpassing the broader US market's growth rate of 9%. Trading significantly below its estimated fair value suggests attractive valuation prospects despite current losses and no recent insider trading activity.

- Click here to discover the nuances of Clover Health Investments with our detailed analytical future growth report.

- Upon reviewing our latest valuation report, Clover Health Investments' share price might be too pessimistic.

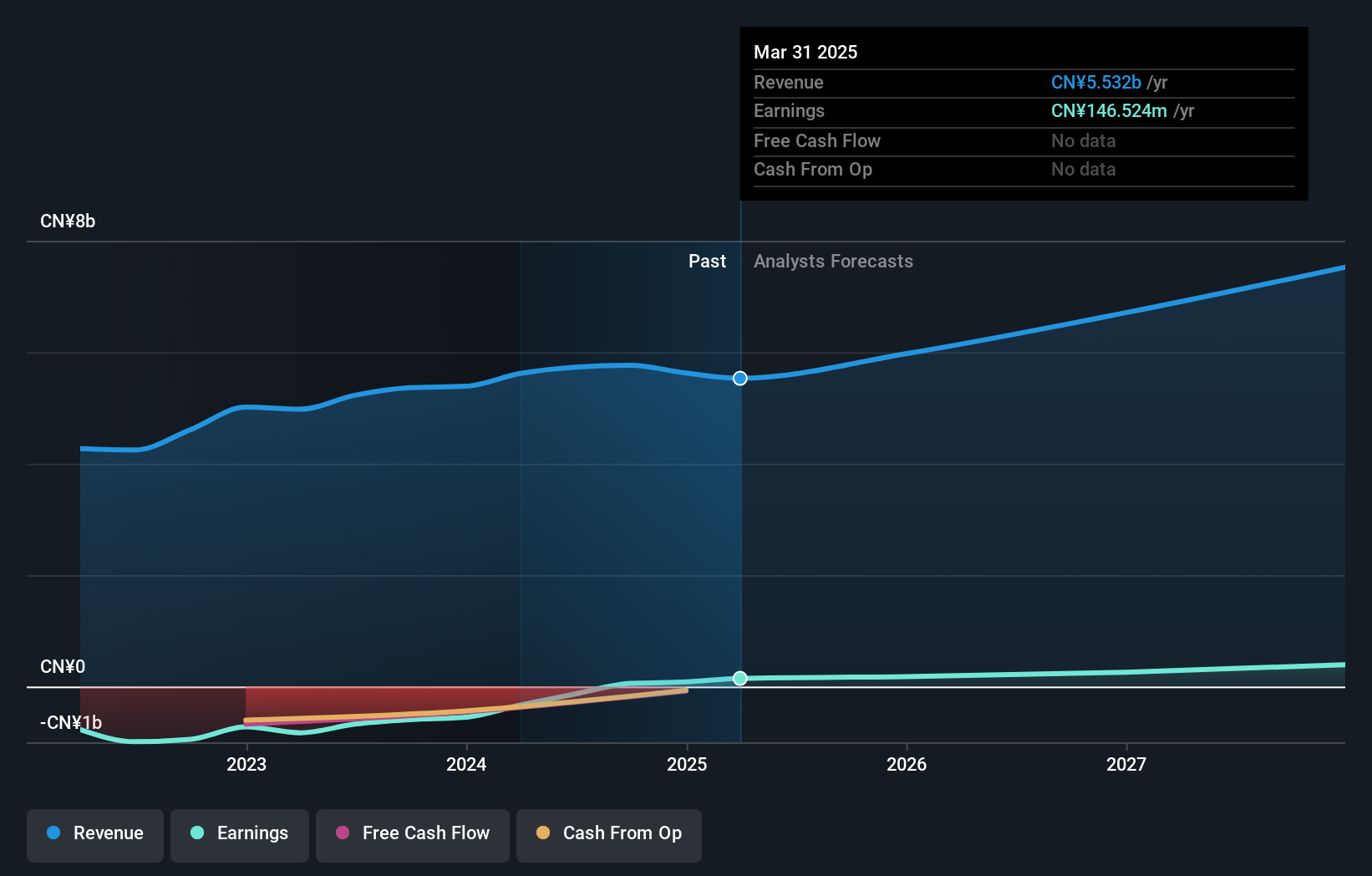

Youdao (NYSE:DAO)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Youdao, Inc. is an internet technology company offering online services in content, community, communication, and commerce in China with a market cap of approximately $903.56 million.

Operations: The company's revenue segments include CN¥2.91 billion from Learning Services, CN¥1.97 billion from Online Marketing Services, and CN¥885.63 million from Smart Devices.

Insider Ownership: 20.3%

Revenue Growth Forecast: 11.8% p.a.

Youdao's earnings are forecast to grow significantly at 98.6% annually, outpacing the US market, though revenue growth of 11.8% lags behind high-growth benchmarks. The company recently became profitable, reporting a net income of CNY 86.25 million for Q3 2024 compared to a loss last year, indicating improving financial health despite large one-off items affecting results. There has been no substantial insider trading activity recently and interest payments remain poorly covered by earnings.

- Delve into the full analysis future growth report here for a deeper understanding of Youdao.

- According our valuation report, there's an indication that Youdao's share price might be on the expensive side.

Taking Advantage

- Unlock more gems! Our Fast Growing US Companies With High Insider Ownership screener has unearthed 201 more companies for you to explore.Click here to unveil our expertly curated list of 204 Fast Growing US Companies With High Insider Ownership.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:DAO

Youdao

An internet technology company, provides online services in the fields of content, community, communication, and commerce in China.

Reasonable growth potential low.

Similar Companies

Market Insights

Community Narratives