Advertisement

- United States

- /

- Hospitality

- /

- NYSE:CCL

How Carnival’s Sustainability Push and Brand Momentum Could Shape Carnival Corporation & (CCL) Investors

Simply Wall St

Reviewed by Sasha Jovanovic

- Carnival Corporation has recently showcased strong cruise demand, progress on its "Less Left Over" food waste program cutting waste by 44% over five years, and ongoing debt reduction efforts across its global brands.

- Together with record holiday bookings at Holland America Line, new Alaska accolades for Princess, and enhanced travel advisor initiatives, these developments underline how Carnival is using sustainability, brand differentiation, and partner engagement to reinforce its position in an evolving cruise industry.

- Now we’ll examine how Carnival’s food waste cuts and sustainability push feed into its existing investment narrative and outlook.

Find companies with promising cash flow potential yet trading below their fair value.

Carnival Corporation & Investment Narrative Recap

To own Carnival, you need to believe strong cruise demand and higher-margin brands can outweigh its still-heavy debt load and ongoing capex needs. The recent “Less Left Over” food waste progress mainly reinforces Carnival’s sustainability credentials and may modestly support margins, but it does not materially change the key near term catalyst of pricing and booking strength, or the central risk that elevated leverage and refinancing obligations continue to weigh on the share price and financial flexibility.

Within that context, Carnival’s 44% reduction in food waste over five years is the clearest link between its sustainability push and cost discipline. By tightening purchasing, batch cooking, and using biodigesters and dehydrators across the fleet, Carnival is trying to squeeze more efficiency out of existing capacity rather than relying solely on new ships, which fits with the catalyst of “same ship” margin improvement while capex and debt remain significant constraints.

Yet, while this sustainability story is encouraging, investors also need to be aware that Carnival’s high debt load still...

Read the full narrative on Carnival Corporation & (it's free!)

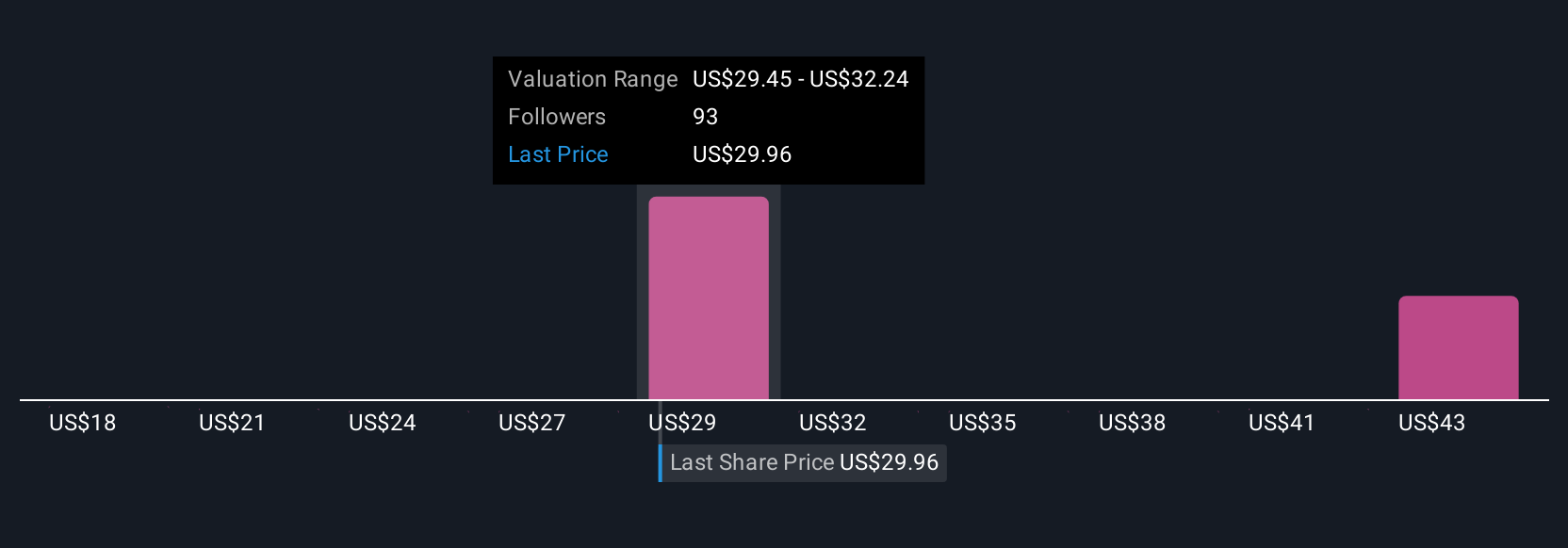

Carnival Corporation &'s narrative projects $29.0 billion revenue and $3.7 billion earnings by 2028. This requires 3.8% yearly revenue growth and about a $1.2 billion earnings increase from $2.5 billion today.

Uncover how Carnival Corporation &'s forecasts yield a $35.76 fair value, a 39% upside to its current price.

Exploring Other Perspectives

Ten Simply Wall St Community fair value estimates for Carnival range from US$24.61 to US$41.57, highlighting sharply different views on upside. Set against this is the shared concern that Carnival’s sizeable pandemic era debt could continue to constrain flexibility and shape performance for years, which is worth weighing as you compare these viewpoints.

Explore 10 other fair value estimates on Carnival Corporation & - why the stock might be worth as much as 61% more than the current price!

Build Your Own Carnival Corporation & Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Carnival Corporation & research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Carnival Corporation & research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Carnival Corporation &'s overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CCL

Carnival Corporation &

A cruise company, provides leisure travel services in North America, Australia, Europe, and internationally.

Undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

43 followersusers have followed this narrative

6 commentsusers have commented on this narrative

15 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

SC

scm on Text ·

TXT will see revenue grow 26% with a profit margin boost of almost 40%

Fair Value:zł8049.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.7% undervalued

955 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.6% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative