Advertisement

- United States

- /

- Hospitality

- /

- NYSE:BROS

Does Dutch Bros' Self-Funded Expansion Shift the Growth Narrative for BROS?

Simply Wall St

Reviewed by Sasha Jovanovic

- Earlier this week, Dutch Bros announced plans to roughly double its store footprint by 2029, building on double-digit annual expansion and a strong focus on internally funded growth.

- An interesting aspect is the company's growing reliance on its customer loyalty program, which now drives more than 70% of its system transactions and supports engagement with younger demographics.

- We'll assess how Dutch Bros' accelerated self-funded expansion could shape the assumptions in its existing investment narrative.

Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

Dutch Bros Investment Narrative Recap

To be a Dutch Bros shareholder, you need to believe in the company’s ability to balance rapid store expansion with disciplined operational execution while maintaining strong same-store sales growth. The news of doubling its store footprint by 2029 highlights the short-term catalyst around sustained self-funded growth, but does not materially change the immediate risk: persistent labor cost inflation and margin pressure, especially as the chain reaches into new markets.

Among Dutch Bros’ recent announcements, the raised financial guidance for 2025 stands out the most in relation to these expansion plans. Management now expects fiscal year revenues of US$1.59 billion to US$1.60 billion and same shop sales growth of around 4.5%, reflecting confidence tied to both existing shop performance and the upcoming stores that underpin the company’s growth narrative.

By contrast, investors should be aware of the risk that Dutch Bros’ aggressive unit growth could introduce the potential for market saturation and shop cannibalization if…

Read the full narrative on Dutch Bros (it's free!)

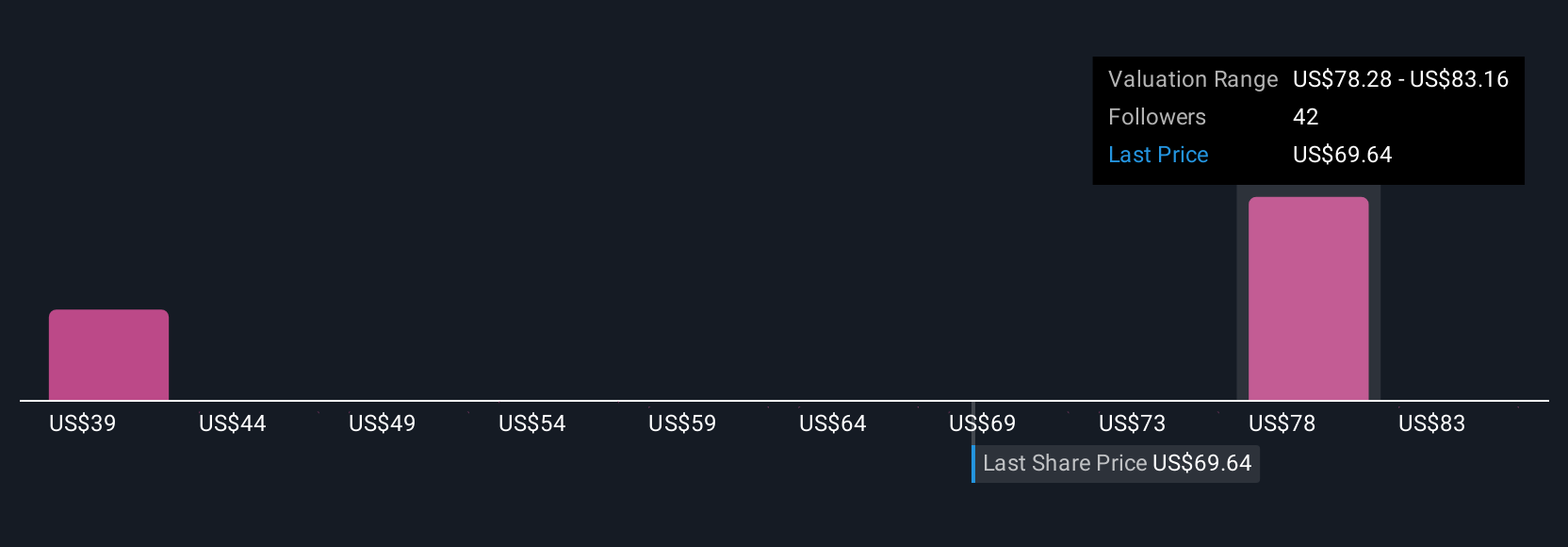

Dutch Bros' outlook calls for $2.6 billion in revenue and $197.4 million in earnings by 2028. This is based on analysts' assumptions of 21.8% annual revenue growth and an increase in earnings of $140.2 million from the current $57.2 million.

Uncover how Dutch Bros' forecasts yield a $82.62 fair value, a 58% upside to its current price.

Exploring Other Perspectives

Nine fair value estimates from the Simply Wall St Community range from US$50.58 to US$88.05 per share, showing a wide spread in investor opinion. While many see growth potential, some are focused on risks like rising labor costs that could impact long-term margins, reminding you that assessing different views is crucial in forming your own outlook.

Explore 9 other fair value estimates on Dutch Bros - why the stock might be worth as much as 68% more than the current price!

Build Your Own Dutch Bros Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Dutch Bros research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Dutch Bros research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Dutch Bros' overall financial health at a glance.

Contemplating Other Strategies?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BROS

Dutch Bros

Operates and franchises drive-thru shops in the United States.

High growth potential with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.1% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|11.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|39.4% undervalued

TR

Community Contributor