If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. So when we looked at Bowlero (NYSE:BOWL) and its trend of ROCE, we really liked what we saw.

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on Bowlero is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.12 = US$225m ÷ (US$2.0b - US$147m) (Based on the trailing twelve months to April 2023).

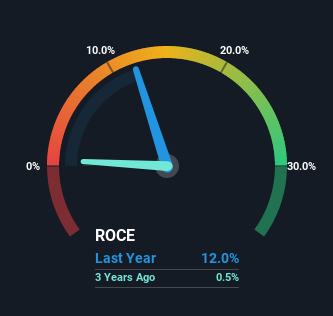

So, Bowlero has an ROCE of 12%. On its own, that's a standard return, however it's much better than the 8.7% generated by the Hospitality industry.

View our latest analysis for Bowlero

Above you can see how the current ROCE for Bowlero compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Bowlero.

SWOT Analysis for Bowlero

- Debt is well covered by cash flow.

- Interest payments on debt are not well covered.

- Expensive based on P/S ratio and estimated fair value.

- Shareholders have been diluted in the past year.

- Expected to breakeven next year.

- Has sufficient cash runway for more than 3 years based on current free cash flows.

- Significant insider buying over the past 3 months.

- No apparent threats visible for BOWL.

What Does the ROCE Trend For Bowlero Tell Us?

Bowlero is displaying some positive trends. The numbers show that in the last five years, the returns generated on capital employed have grown considerably to 12%. The amount of capital employed has increased too, by 81%. The increasing returns on a growing amount of capital is common amongst multi-baggers and that's why we're impressed.

The Key Takeaway

To sum it up, Bowlero has proven it can reinvest in the business and generate higher returns on that capital employed, which is terrific. And investors seem to expect more of this going forward, since the stock has rewarded shareholders with a 25% return over the last year. Therefore, we think it would be worth your time to check if these trends are going to continue.

On a final note, we've found 1 warning sign for Bowlero that we think you should be aware of.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:LUCK

Lucky Strike Entertainment

Provides location-based entertainment platforms under the AMF, Bowlero, Lucky X Strike, Boomers, and PBA brand names in North America.

Good value with moderate growth potential.

Market Insights

Community Narratives