Advertisement

- United States

- /

- Consumer Services

- /

- NYSE:ATGE

Adtalem Global Education (ATGE): Exploring Valuation as Options Volatility and Growth Concerns Draw Investor Focus

Simply Wall St

Reviewed by Kshitija Bhandaru

Adtalem Global Education (ATGE) is capturing investor attention as elevated implied volatility in the options market points to expectations of sizable stock moves. Some analysts are now flagging concerns about slower revenue growth and capital efficiency.

See our latest analysis for Adtalem Global Education.

Adtalem Global Education’s share price has surged 54% year-to-date, with the past three months alone delivering a nearly 21% gain as investors reward impressive annual net income growth and a discounted valuation story. However, the pace of momentum has cooled a bit this week. As concerns about future growth and capital efficiency surface, the stock’s lofty 90% total return in the past year is now meeting fresh scrutiny from traders weighing both upside potential and risk.

If you’re curious to see what other fast-rising companies are catching attention, now’s a great time to discover fast growing stocks with high insider ownership

With valuations looking attractive and recent performance turning heads, the question is whether Adtalem remains undervalued or if the market is already factoring in all the future growth, leaving little room for upside.

Price-to-Earnings of 22.3x: Is it justified?

At $142.58, Adtalem Global Education trades at a price-to-earnings (P/E) multiple of 22.3x, which is notably higher than the Consumer Services industry average of 17x and the peer average of 19.7x.

The price-to-earnings ratio shows how much investors are willing to pay for each dollar of the company's earnings. This metric is widely used in the education and services sector, where relative earnings power can attract premium valuations during periods of strong growth.

Despite presenting higher earnings growth over the past year, the market is pricing Adtalem at a significant premium to its peers. Relative to its fair P/E estimate of 23.3x, there is a case that the market valuation could be justified if recent earnings momentum is sustained. Investors should note the fair ratio provides a level the market may aim for if current performance persists.

Explore the SWS fair ratio for Adtalem Global Education

Result: Price-to-Earnings of 22.3x (OVERVALUED)

However, slowing revenue growth and declining capital efficiency could challenge the market's optimistic view of Adtalem’s valuation going forward.

Find out about the key risks to this Adtalem Global Education narrative.

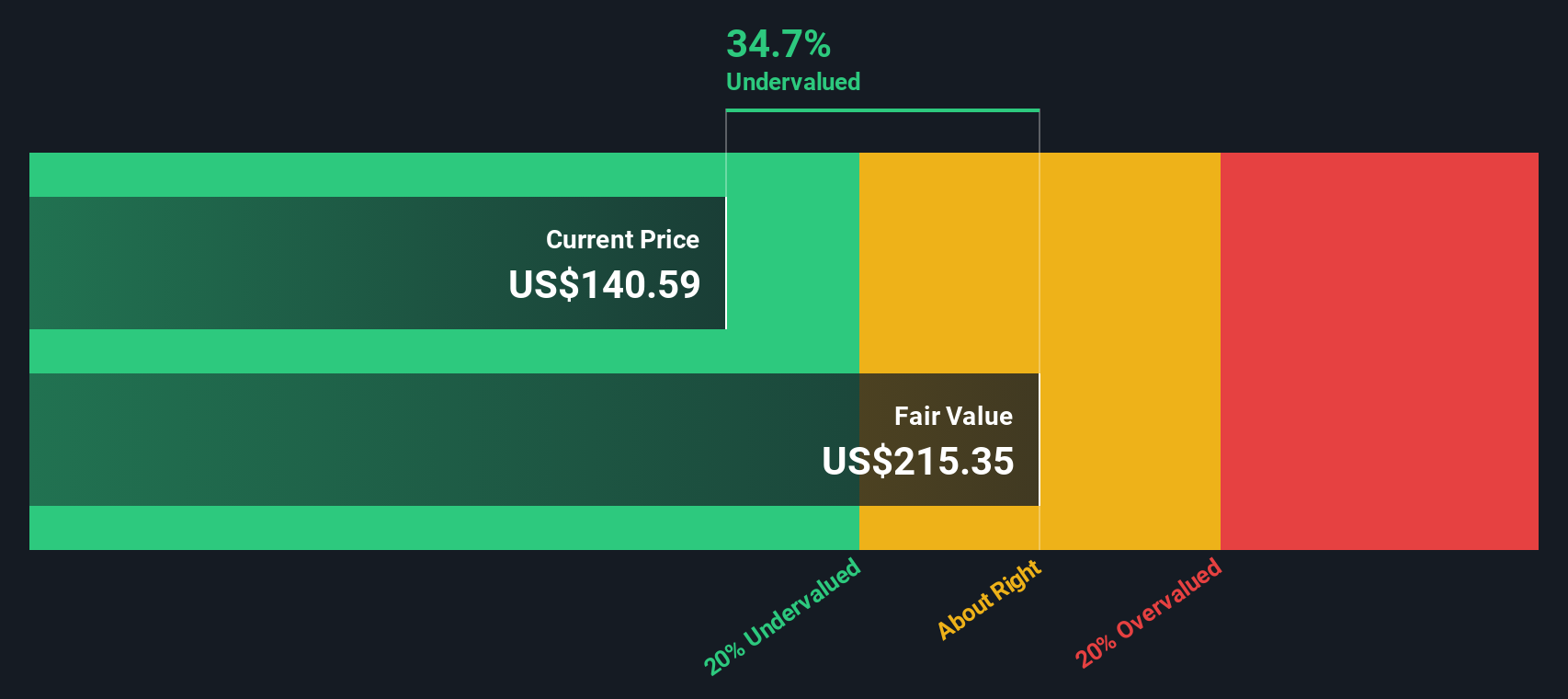

Another View: Discounted Cash Flow Model Points to Undervaluation

Looking beyond earnings multiples, our SWS DCF model estimates Adtalem's fair value at $210.26, which is significantly above its current price of $142.58. This approach suggests the market may be underestimating future cash flows. Could this gap indicate untapped potential, or is it a reflection of different risks?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Adtalem Global Education for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Adtalem Global Education Narrative

If you have a different perspective or want to interpret the numbers yourself, you can quickly build your own view of Adtalem Global Education. Do it your way

A great starting point for your Adtalem Global Education research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Why limit your search to just one opportunity? Smart investors always keep an eye out for market moves that offer big growth, yield, and disruptive potential.

- Capture yield from companies that reward shareholders and see which names offer impressive returns with these 19 dividend stocks with yields > 3%.

- Unlock tech breakthroughs by checking out the innovators transforming artificial intelligence with these 25 AI penny stocks.

- Stay ahead of the curve and spot market mispricings by filtering must-watch bargains using these 897 undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ATGE

Adtalem Global Education

Provides healthcare education in the United States, Barbados, St.

Solid track record and fair value.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|2.3% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|40.4% undervalued

TR

Community Contributor