Advertisement

- United States

- /

- Hospitality

- /

- NasdaqGS:WING

Wingstop (WING): Assessing Valuation Prospects After Recent Share Price Rebound

Wingstop (WING) shares have seen movement recently, drawing some investor interest as the company’s year-over-year revenue growth remains steady at 15%. The stock’s performance has fluctuated over the past month and this has prompted closer attention to its valuation outlook.

See our latest analysis for Wingstop.

Wingstop’s recent bounce, with a 9% share price return over the past month, hints at renewed optimism following a rough patch earlier this year. While momentum has improved in the short term, the one-year total shareholder return is down 19%, showing that many investors are still waiting for a more convincing turnaround, particularly after such impressive three- and five-year total returns.

If you’re curious about what’s gaining traction beyond the usual names, this is a great moment to broaden your investing radar and check out fast growing stocks with high insider ownership

So after this period of mixed returns and steady revenue growth, is Wingstop trading at a compelling discount for investors? Or has the market already factored in all of its future expansion prospects?

Most Popular Narrative: 16.8% Undervalued

Wingstop’s most widely followed narrative sees its fair value comfortably above the last close, suggesting the market is not fully crediting future potential. With analyst expectations pointing to meaningful expansion, this sets the stage for strong debate around the company's real growth trajectory.

The rapid roll-out and full system implementation of the Wingstop Smart Kitchen platform is significantly improving operational efficiency, order throughput, guest satisfaction, speed of service, and consistency. This is expected to drive higher same-store sales, increased delivery frequency, and better net margins as restaurants ramp to the new model.

Curious what kind of aggressive growth forecast is reflected in that price? The narrative’s key numbers combine digital shifts, earnings upgrades, and a future valuation multiple that may surprise even seasoned sector watchers. What is the boldest bet behind this fair value? Only one way to find out.

Result: Fair Value of $318 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent consumer demand softness and limited menu innovation could undermine the upbeat outlook and temper investor enthusiasm for Wingstop’s expansion story.

Find out about the key risks to this Wingstop narrative.

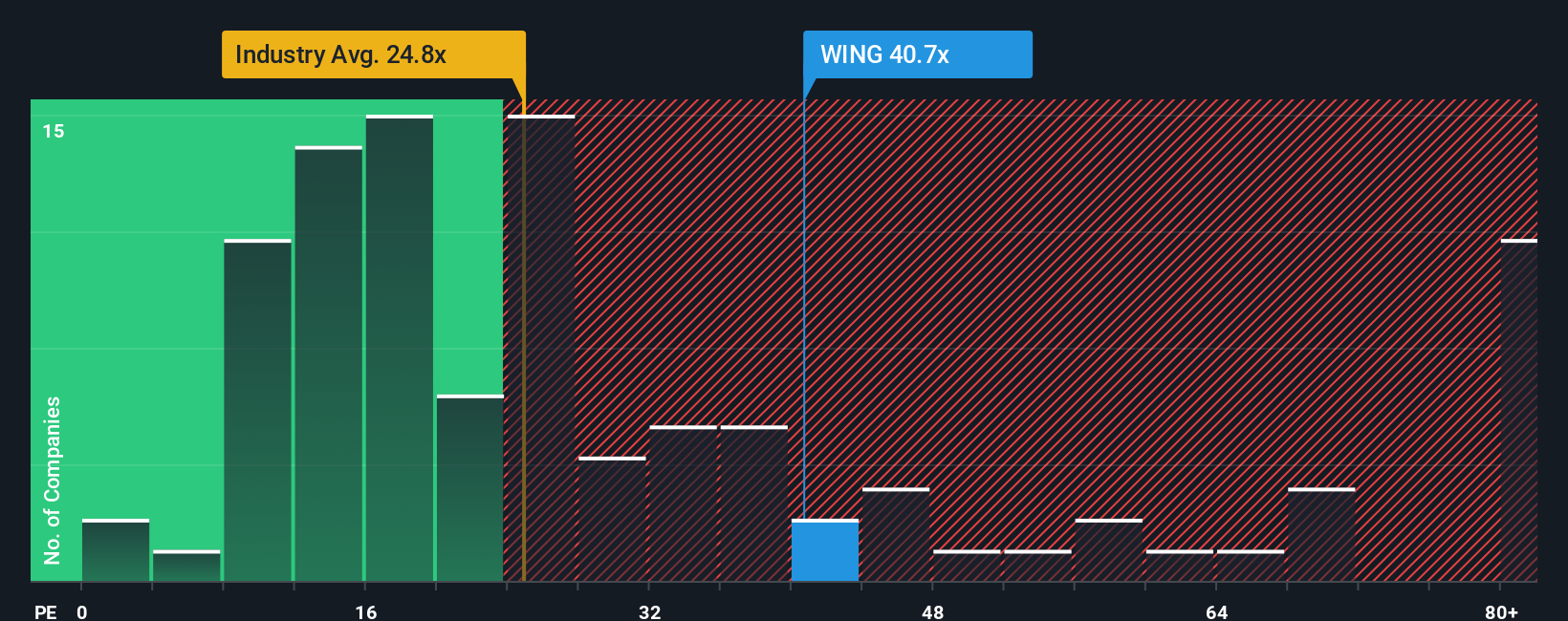

Another View: The Market’s Multiple Sends a Warning

Looking at how Wingstop is valued compared to its peers, the stock trades on a price-to-earnings ratio of 42.2x. This is double the US Hospitality industry average of 21.4x and well above the fair ratio of 18.7x. This means investors are paying a steep premium. What happens if the market mood shifts?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Wingstop Narrative

If you see things differently or want to dive deeper into the numbers on your own terms, building your own perspective takes just a few minutes. Do it your way

A great starting point for your Wingstop research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t miss out on unique opportunities. Smart investors cast a wide net. Let Simply Wall Street’s Screener show you where innovation and value are thriving right now.

- Capitalize on market inefficiencies and target promising businesses by checking out these 920 undervalued stocks based on cash flows that stand out for their strong cash flows and attractive valuations.

- Accelerate your portfolio's growth by tapping into these 25 AI penny stocks powering breakthroughs in automation and artificial intelligence across several industries.

- Start building reliable income streams with these 15 dividend stocks with yields > 3% offering yields above 3% for those seeking more stability from their investments.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Wingstop might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:WING

Wingstop

Wingstop Inc., together with its subsidiaries, franchises and operates restaurants under the Wingstop brand in United States, Australia, Bahrain, Kuwait, Puerto Rico, Saudi Arabia, and The Netherlands.

Low risk and slightly overvalued.

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2540.2% undervalued

94 followersusers have followed this narrative

0 commentsusers have commented on this narrative

23 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.828.5% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23059.3% overvalued

37 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32040.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Recently Updated Narratives

DA

DaneDruss on Cloudflare ·

Q-Day: Quantum Hype vs Quantum-Safe Infrastructure

Fair Value:US$167.4547.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BU

Bullish4YaMotha on Celsius Holdings ·

Celsius Holdings ($CELH): $33.04 – Swing Trading Timeframe: 1–2 Months. Score: 8.8/10

Fair Value:US$47.3730.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WE

WealthAP on Alphabet ·

The "Easy Money" Is Gone: Why Alphabet Is Now a "Show Me" Story

Fair Value:US$386.435.2% undervalued

71 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.9% undervalued

84 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9631.8% undervalued

64 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5453.8% undervalued

58 followersusers have followed this narrative

1 commentusers have commented on this narrative

10 likesusers have liked this narrative

Trending Discussion

MW

mwod31 on Greatland Resources ·

A great comment, WSB have not done the research imo. I intend to buy more shares in 2026.

0

|0