Advertisement

- United States

- /

- Hospitality

- /

- NasdaqGS:WEN

Expansion, Recovery and Optimization are the Highlights of Wendy's (NASDAQ:WEN) Earnings Analysis

- Sales are expected to grow to 2b in FY 2022, while net income and FCF are recovering, and Wendy's is making more cash than earnings.

- Profitability has dropped to 14.5%, but the company is expected to increase returns as the ERP project matures, and sales as it expands into the U.K.

- The forward P/E suggests the stock is relatively overvalued, but the business development may justify the premium.

The Wendy's Company's (NASDAQ:WEN) released its Q2 earnings report, and we find that the business is stable, with continuous reinvestment into growth and productivity. While the last six months did mark an increase in some expenses, the company is offsetting that with growth and the planned entry into the U.K. market.

See our latest analysis for Wendy's

Wendy's Q2 Earnings Analysis

- Revenue grew 9% YoY to $537.8m

- Adj. revenue (total less advertising revenue) grew 10.7% to $432.9m.

- Restaurant margins dropped to 14.5% from 20.3%.

- Net income dropped by 26.7% to $48.2m

- Free cash flow is down 49% on a half-year basis to $95.2m.

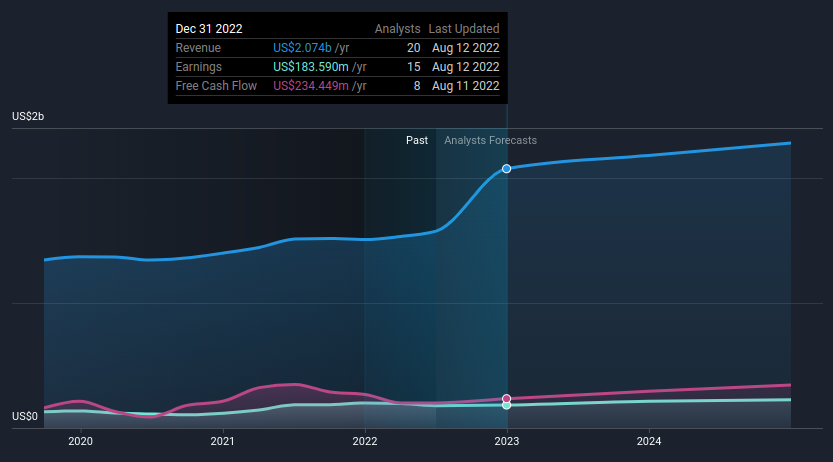

With that in mind, we can also see how analysts are predicting the future of Wendy's in the chart below:

It seems that analysts are expecting Wendy's future revenues to kick off and for the FY 2022, the company is expected to make $2b in sales. The bottom line is also expected to start a recovery, with net income estimated at $184m and free cash flow at $234.5m - both of which are expected to steadily grow through 2025.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Wendy's.

This is roughly in-line with the latest 2022 future outlook issued by management:

- Global sales growth: 6% to 8%

- Cash flows from operations: $305m to $325m

- Capital expenditures: $90m to $100m

- Free cash flow: $215m to $225m

- Adj. EPS: $0.84 to $0.88

Costs Are Rising But Manageable

In the earnings report, we noted an increase in costs (COGS) by 22.9% in the last 6 months, primarily attributable to a decrease in restaurant profitability. The company also noted a general increase in expenses for higher salaries and benefits, it seems that in 2022 Wendy's has indeed suffered the effects of inflation as customers have reduced their spend and costs of running the business have increased.

The earnings report outlined that the company is incurring tech costs due to the implementation of their ERP system. While this is draining profitability at the moment, ERP systems help a company reduce costs and optimize internal operations. This also helps Wendy's better coordinate businesses across countries and legislative compliance, which can help the business with their global expansion - Wendy's opened net 41 restaurants in the first 6 months of 2022 outside the U.S. - Management notes this as the impact of the new locations:

"The increase in revenues was primarily driven by higher sales at Company-operated restaurants driven by the favorable impact of the acquisition of 93 franchise-operated restaurants in Florida during the fourth quarter of 2021 and higher same-restaurant sales, partially offset by the sale of 47 Company-operated restaurants in the New York market."

While the payroll and software expenses from implementing an ERP system count towards operating expenses, some investors may view the complete ERP implementation project as a capital expense, that can increase future value by cutting costs.

What This Means For Investors

At first glance, Wendy's price-to-earnings (or "P/E") ratio of 25.5x might seem on the high end, however EPS is anticipated to climb by 14% per year during the coming three years according to the analysts, which means that there is some future growth holding up the valuation. If we switch to the forward P/E for the company, we see it drop to 23.2x. Additionally, the company has a negative accrual ratio, which means that it makes more cash than is reported by earnings, this is something to consider, as the cash flows may be a more appropriate measure for the company value instead of using a generic P/E ratio.

While the recovering fundamentals are a great aspect of the company, keep in mind that the industry average P/E is at 18.4x, which makes Wendy's relatively overvalued. Don't forget that there may be other risks. For instance, we've identified 2 warning signs for Wendy's you should be aware of.

Valuation is complex, but we're here to simplify it.

Discover if Wendy's might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NasdaqGS:WEN

Wendy's

Operates as a quick-service restaurant company in the United States and internationally.

Established dividend payer and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4727.3% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$481.5% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6410.8% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Alphabet ·

GOOGL: AI Platform Expansion And Cloud Demand Will Support Durable Performance Amid Competitive Pressures

Fair Value:US$323.70.8% undervalued

1342 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative