Advertisement

- United States

- /

- Hospitality

- /

- NasdaqGS:TAST

Carrols Restaurant Group, Inc.'s (NASDAQ:TAST) Share Price Boosted 30% But Its Business Prospects Need A Lift Too

Carrols Restaurant Group, Inc. (NASDAQ:TAST) shares have continued their recent momentum with a 30% gain in the last month alone. The last 30 days were the cherry on top of the stock's 338% gain in the last year, which is nothing short of spectacular.

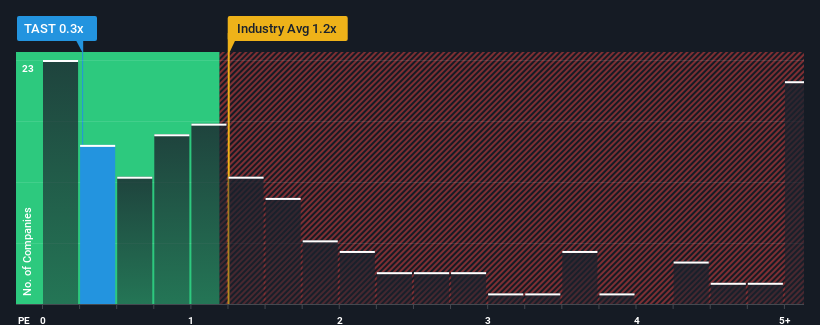

Although its price has surged higher, when close to half the companies operating in the United States' Hospitality industry have price-to-sales ratios (or "P/S") above 1.2x, you may still consider Carrols Restaurant Group as an enticing stock to check out with its 0.3x P/S ratio. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for Carrols Restaurant Group

How Carrols Restaurant Group Has Been Performing

Carrols Restaurant Group could be doing better as it's been growing revenue less than most other companies lately. It seems that many are expecting the uninspiring revenue performance to persist, which has repressed the growth of the P/S ratio. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Carrols Restaurant Group will help you uncover what's on the horizon.How Is Carrols Restaurant Group's Revenue Growth Trending?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Carrols Restaurant Group's to be considered reasonable.

Retrospectively, the last year delivered a decent 8.8% gain to the company's revenues. The latest three year period has also seen a 21% overall rise in revenue, aided somewhat by its short-term performance. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

Shifting to the future, estimates from the four analysts covering the company suggest revenue should grow by 3.6% over the next year. Meanwhile, the rest of the industry is forecast to expand by 17%, which is noticeably more attractive.

In light of this, it's understandable that Carrols Restaurant Group's P/S sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Key Takeaway

Despite Carrols Restaurant Group's share price climbing recently, its P/S still lags most other companies. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We've established that Carrols Restaurant Group maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. The company will need a change of fortune to justify the P/S rising higher in the future.

You need to take note of risks, for example - Carrols Restaurant Group has 2 warning signs (and 1 which is potentially serious) we think you should know about.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:TAST

Carrols Restaurant Group

Through its subsidiaries, operates restaurants in the United States.

Moderate growth potential with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.8% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.5% undervalued

GM

Community Contributor