- United States

- /

- Hospitality

- /

- NasdaqGS:MLCO

Melco Resorts (NasdaqGS:MLCO): Assessing Valuation Following Recent Surge in Investor Interest

Reviewed by Simply Wall St

Price-to-Earnings of 66.2x: Is it justified?

Melco Resorts & Entertainment's shares are currently trading at a price-to-earnings (P/E) ratio of 66.2x. This is significantly higher than both the US Hospitality industry average of 23.9x and the peer average of 40.1x. This elevated P/E ratio suggests the company is being valued at a considerable premium compared to its sector and industry peers.

The price-to-earnings multiple is a common metric used to assess whether a stock is trading at a reasonable price relative to its earnings. A high P/E often reflects strong investor expectations for future growth, while a lower P/E can indicate skepticism about the company's prospects. For hospitality companies like Melco, P/E offers insight into how much investors are willing to pay for a dollar of current earnings.

This premium valuation could mean the market is pricing in robust future profit growth or a turnaround story; however, it also raises the bar for future performance. Investors should consider whether current earnings justify such a high multiple or if momentum and sentiment are playing a greater role than fundamentals.

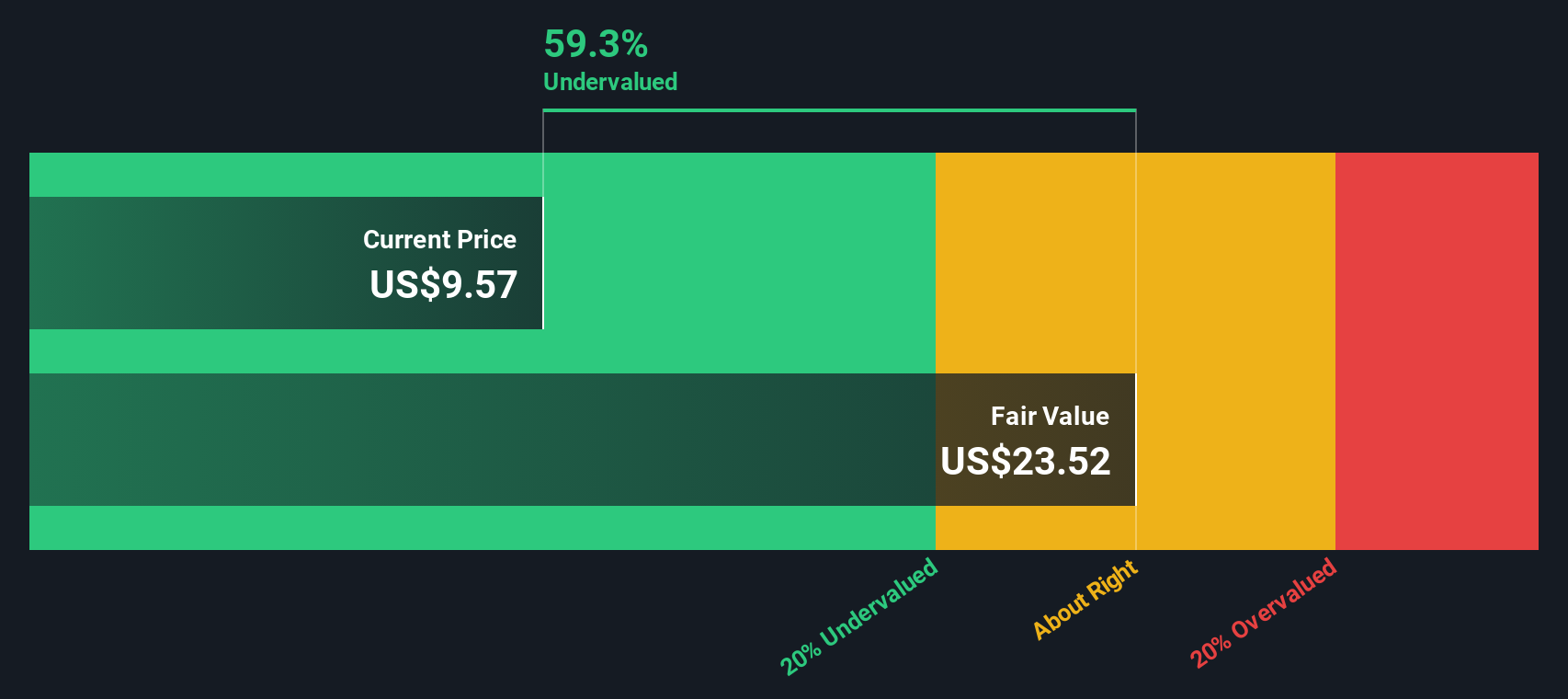

Result: Fair Value of $9.61 (OVERVALUED)

See our latest analysis for Melco Resorts & Entertainment.However, a sudden shift in broader market sentiment or any slowdown in revenue growth could quickly challenge the optimism that is currently fueling Melco's valuation.

Find out about the key risks to this Melco Resorts & Entertainment narrative.Another View: What Does Our DCF Model Suggest?

Taking a different perspective, the SWS DCF model points to a much more optimistic assessment compared to the high earnings-based valuation. This approach suggests Melco could actually be undervalued right now. With two very different pictures, which outlook will prove closer to reality as the company moves forward?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Melco Resorts & Entertainment Narrative

If you see things differently or would rather come to your own conclusions, you can craft your own perspective in just a few minutes using Do it your way.

A great starting point for your Melco Resorts & Entertainment research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Expand your horizons and get ahead of the curve by tapping into strategies that other investors might miss. These smart screens can put you on the fast track to opportunities that match your ambitions.

- Capture potential early-stage winners by using penny stocks with strong financials to spot companies showing surprising financial strength in the micro-cap space.

- Fuel your portfolio’s growth with future-focused businesses that are leading advances in medicine and technology through healthcare AI stocks.

- Target reliable returns by scanning for standout companies delivering yields above 3% with the help of dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NasdaqGS:MLCO

Melco Resorts & Entertainment

Develops, owns, and operates casino gaming and resort facilities in Asia and Europe.

Good value with reasonable growth potential.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion