Advertisement

- United States

- /

- Hospitality

- /

- NasdaqGS:MAR

Has Marriott’s Rally and Travel Recovery Left Limited Room for Future Returns in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Marriott International at around $306 a share is still a smart buy or if most of the upside is already priced in? You are not alone. This stock divides opinion among value focused investors.

- Over the last month the stock has climbed 12.6%, adding to a strong 3 year gain of 96.7% and a 5 year gain of 141.3%, while the 1 year return of 5.9% and 7 day move of 0.7% suggest momentum has cooled a little.

- Recently, investors have been digesting a mix of travel industry updates, from continued strength in global leisure and business travel to ongoing consolidation talks and expansion of loyalty partnerships across major hotel brands. For Marriott, developments around network expansion, brand refreshes and shifting expectations for interest rates and consumer spending have all fed into changing views on the stock's risk and growth profile.

- Despite that backdrop, Marriott currently scores just 0/6 on our valuation checks for being undervalued. This raises the question of whether traditional methods are missing something important. Next we will walk through the standard valuation approaches investors use, then finish with a more complete way to think about what this business might really be worth over time.

Marriott International scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Marriott International Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow model estimates what a business is worth today by projecting the cash it can generate in the future and discounting those cash flows back to their value in $ today.

For Marriott International, the latest twelve month Free Cash Flow is about $1.9 Billion. Analysts and internal forecasts expect this to grow steadily over the next decade, with projected Free Cash Flow reaching roughly $5.5 Billion by 2035, based on a 2 stage Free Cash Flow to Equity approach that blends analyst estimates for the next few years with longer term growth assumptions from Simply Wall St.

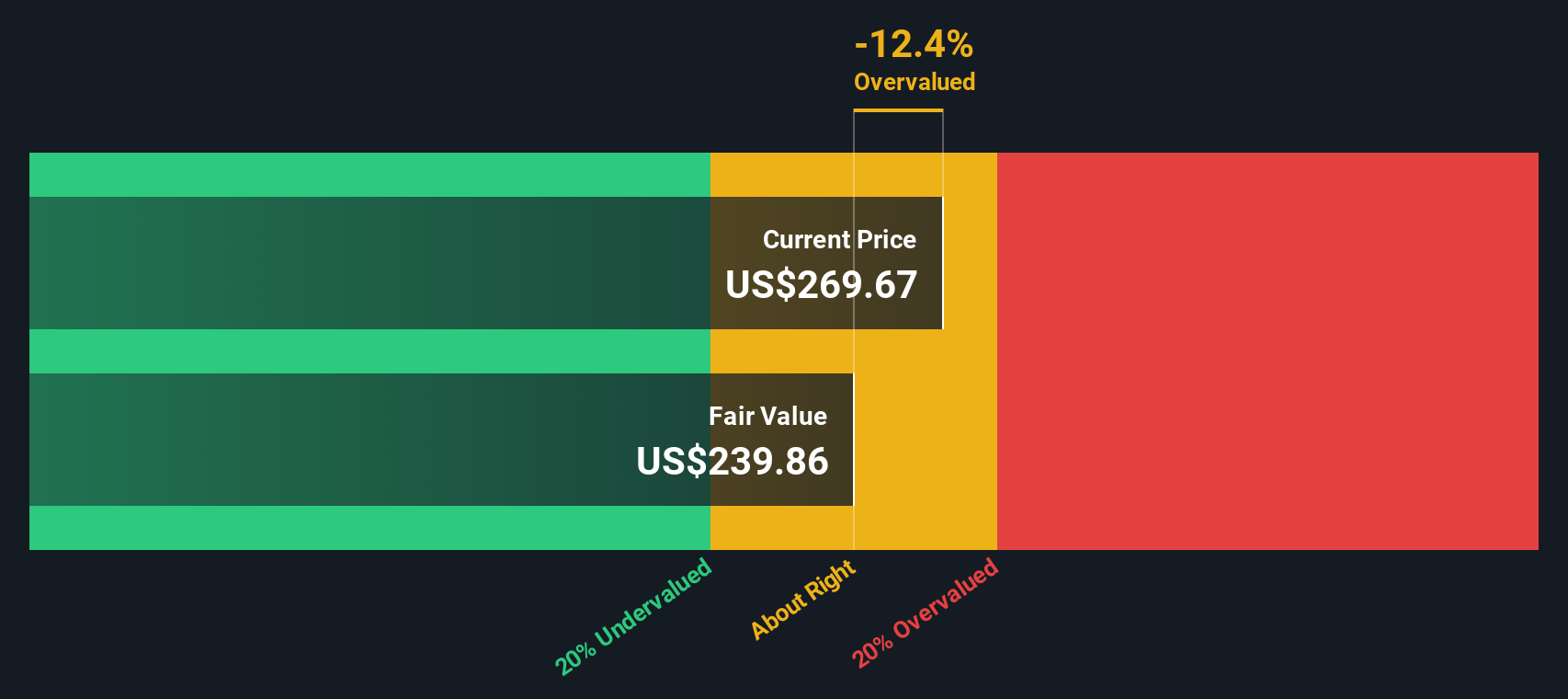

When these projected cash flows are discounted back, the model arrives at an intrinsic value of about $267 per share, compared with a current market price around $306. That suggests the shares are roughly 14.8% above the value indicated by the DCF model, which may indicate that a significant portion of expected future growth is already reflected in the price.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Marriott International may be overvalued by 14.8%. Discover 916 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Marriott International Price vs Earnings

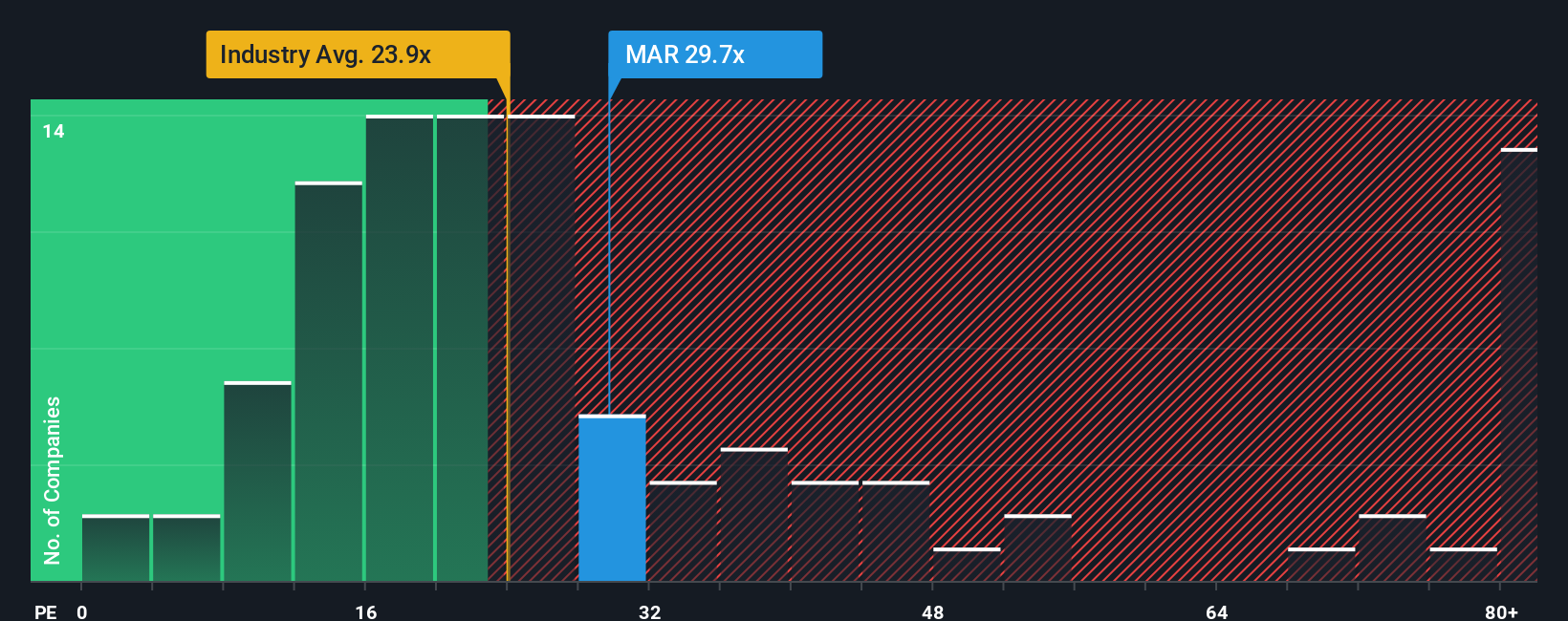

For profitable companies like Marriott International, the Price to Earnings, or PE, ratio is a useful way to judge whether investors are paying a reasonable price for each dollar of current earnings. In general, faster growth and lower risk justify a higher PE, while slower growth and higher uncertainty point to a lower, more conservative multiple.

Marriott currently trades on a PE of about 31.5x. That is well above the broader Hospitality industry average of roughly 21.2x and also ahead of the peer group average of around 29.2x, suggesting investors are already paying a premium for its brand strength, scale and earnings profile.

Simply Wall St also calculates a proprietary Fair Ratio of 28.0x for Marriott, which estimates the PE you would normally expect given its earnings growth outlook, profitability, industry, market value and risk factors. This Fair Ratio is more informative than a simple industry or peer comparison because it adjusts for Marriott’s specific fundamentals rather than assuming all hotel companies deserve similar valuations. Since the current PE of 31.5x sits noticeably above the 28.0x Fair Ratio, the shares look somewhat expensive on this metric.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Marriott International Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of Marriott International’s story with a concrete forecast and fair value. A Narrative is your explanation for what you think will happen to a company’s revenue, earnings and margins over time, and how that should translate into a fair value per share, instead of just accepting a single target price or PE multiple. On Simply Wall St’s Community page, used by millions of investors, Narratives make this process accessible by guiding you to set assumptions, generate a forecast, and instantly compare your Fair Value to the current market price to see if Marriott looks like a buy, hold or sell to you. As new information comes in, such as earnings results, macro data or company news, Narratives update dynamically so your view stays current without starting from scratch. For example, one investor might build a bullish Narrative around rapid APAC and EMEA expansion and assign a fair value near the top of recent targets around $332, while a more cautious investor might focus on margin pressure and macro risks and land closer to the low end around $205.

Do you think there's more to the story for Marriott International? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:MAR

Marriott International

Engages in operation, franchising, and licensing of hotel, residential, timeshare, and other lodging properties worldwide.

Reasonable growth potential second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

41 followersusers have followed this narrative

6 commentsusers have commented on this narrative

13 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

SC

scm on Text ·

TXT will see revenue grow 26% with a profit margin boost of almost 40%

Fair Value:zł8048.3% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

955 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative