Advertisement

- United States

- /

- Hospitality

- /

- NasdaqGS:LOCO

El Pollo Loco Holdings, Inc. Just Recorded A 19% EPS Beat: Here's What Analysts Are Forecasting Next

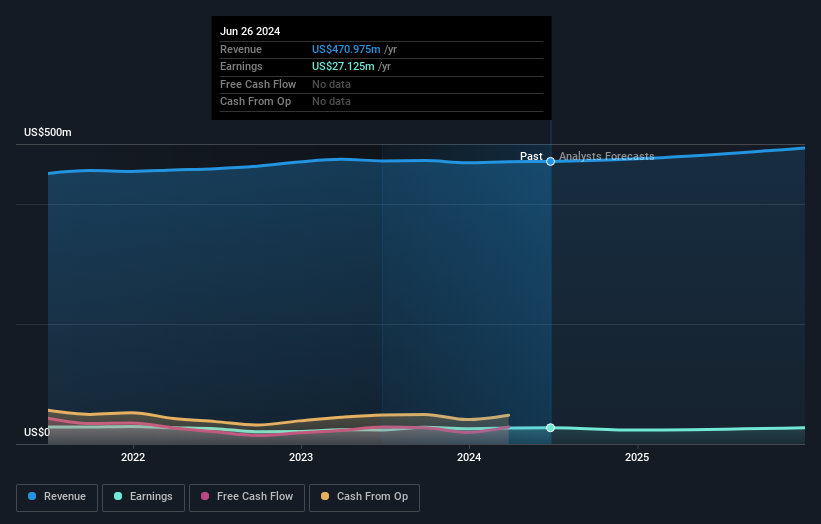

It's been a good week for El Pollo Loco Holdings, Inc. (NASDAQ:LOCO) shareholders, because the company has just released its latest second-quarter results, and the shares gained 3.6% to US$11.96. It looks like a credible result overall - although revenues of US$122m were in line with what the analysts predicted, El Pollo Loco Holdings surprised by delivering a statutory profit of US$0.25 per share, a notable 19% above expectations. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

Check out our latest analysis for El Pollo Loco Holdings

Taking into account the latest results, El Pollo Loco Holdings' four analysts currently expect revenues in 2024 to be US$475.3m, approximately in line with the last 12 months. Statutory earnings per share are expected to decline 16% to US$0.76 in the same period. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$473.1m and earnings per share (EPS) of US$0.69 in 2024. There was no real change to the revenue estimates, but the analysts do seem more bullish on earnings, given the nice gain to earnings per share expectations following these results.

The consensus price target rose 12% to US$13.75, suggesting that higher earnings estimates flow through to the stock's valuation as well. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. The most optimistic El Pollo Loco Holdings analyst has a price target of US$14.50 per share, while the most pessimistic values it at US$13.00. With such a narrow range of valuations, the analysts apparently share similar views on what they think the business is worth.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. The period to the end of 2024 brings more of the same, according to the analysts, with revenue forecast to display 1.9% growth on an annualised basis. That is in line with its 2.1% annual growth over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenues grow 9.7% per year. So although El Pollo Loco Holdings is expected to maintain its revenue growth rate, it's forecast to grow slower than the wider industry.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around El Pollo Loco Holdings' earnings potential next year. On the plus side, there were no major changes to revenue estimates; although forecasts imply they will perform worse than the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have forecasts for El Pollo Loco Holdings going out to 2025, and you can see them free on our platform here.

And what about risks? Every company has them, and we've spotted 1 warning sign for El Pollo Loco Holdings you should know about.

Valuation is complex, but we're here to simplify it.

Discover if El Pollo Loco Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:LOCO

El Pollo Loco Holdings

Through its subsidiary, El Pollo Loco, Inc., develops, franchises, licenses, and operates quick-service restaurants under the El Pollo Loco name.

Proven track record with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.3% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.0% undervalued

TI

Community Contributor