- United States

- /

- Hospitality

- /

- NasdaqGS:DKNG

DraftKings (NasdaqGS:DKNG) Surges 5% As Net Loss Widens To US$135 Million

Reviewed by Simply Wall St

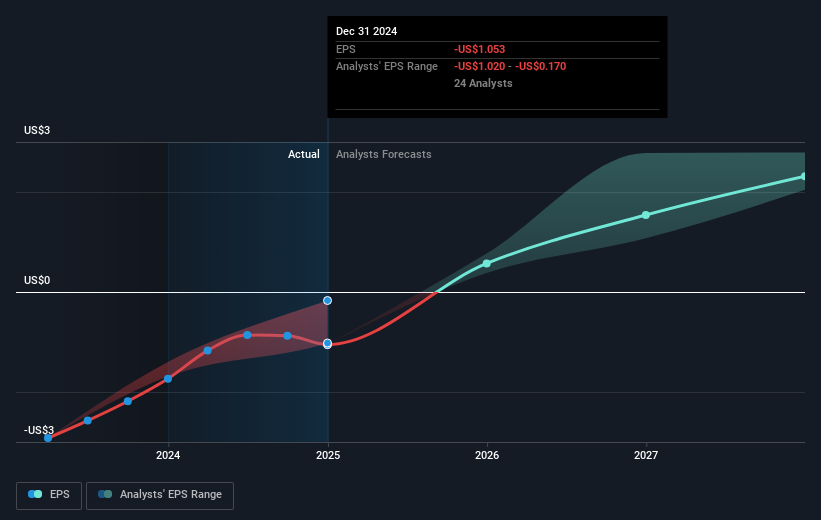

DraftKings (NasdaqGS:DKNG) experienced a price movement of 5.47% over the past month, during which several key events unfolded. The company announced its earnings for Q4 2024, with sales rising substantially from the previous year, yet the net loss widened to USD 135 million compared to the previous year's quarter. Despite the increased loss, DraftKings improved its full-year financials and raised its revenue guidance for 2025, signaling strong future growth potential. Meanwhile, the company completed a share buyback program and initiated a USD 500 million debt financing process that could impact its long-term capital structure. Amidst these company-specific developments, the broader stock market has experienced volatility, with major U.S. indexes mixed as investors reacted to broader economic concerns, including recent tariff announcements. DraftKings' performance contrasts with the 3.6% decline in overall market performance, reflecting investor confidence in its growth trajectory despite macroeconomic uncertainties.

Navigate through the intricacies of DraftKings with our comprehensive report here.

Over the last five years, DraftKings has delivered a total return of 132%, reflecting substantial investor interest. During this period, the company has consistently expanded its revenue, with the most recent earnings report showing full-year sales reaching US$4.77 billion, up significantly from prior years. Despite widening net losses, the company has promising revenue growth forecasts, expected to outperform the broader U.S. market. Analyst expectations back this optimism, as target prices suggest a considerable upside to the current share price, amid a positive consensus among analysts.

DraftKings' share repurchase initiatives, such as the completion of a buyback program, likely supported its stock price over time. Nevertheless, the company's performance has lagged behind the U.S. market and hospitality industry over the past year, where both sectors have seen returns close to 17%. Looking ahead, DraftKings' forecasts suggest a turning point with potential profitability and high return on equity projected within three years, signaling transformational change and potential future upside for long-term shareholders.

- Learn how DraftKings' intrinsic value compares to its market price with our detailed valuation report.

- Assess the downside scenarios for DraftKings with our risk evaluation.

- Is DraftKings part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DKNG

DraftKings

High growth potential and fair value.

Similar Companies

Market Insights

Community Narratives