- United States

- /

- Food and Staples Retail

- /

- NYSE:DG

Dollar General (NYSE:DG) Rises 35% Last Quarter Amid DoorDash SNAP/EBT Integration

Reviewed by Simply Wall St

Dollar General (NYSE:DG) witnessed a notable price increase of 35% over the last quarter, reflecting several impactful corporate events. The company's partnership with DoorDash to integrate SNAP/EBT payments across 16,000 stores marks a significant enhancement in service for SNAP-eligible customers. Concurrently, the forward guidance indicating modest sales growth contrasts with a year-over-year drop in net income. Despite the market's broader stability, Dollar General's strategic business expansions, such as the new distribution center in Arkansas, and product line collaborations with Dolly Parton, may have contributed positively to its stock performance amid mixed corporate earnings reports across the market.

You should learn about the 2 weaknesses we've spotted with Dollar General.

Dollar General's recent partnership with DoorDash to integrate SNAP/EBT payments could enhance service offerings and customer convenience across its vast network of 16,000 stores. This move aligns with the company's ongoing digital initiatives and is anticipated to positively impact revenue and earnings forecasts by broadening its customer base and potentially increasing sales through enhanced accessibility. Despite the past year's total shareholder return being a 26.46% decline, this integration provides a growth opportunity that may counterbalance economic pressures impacting consumer spending.

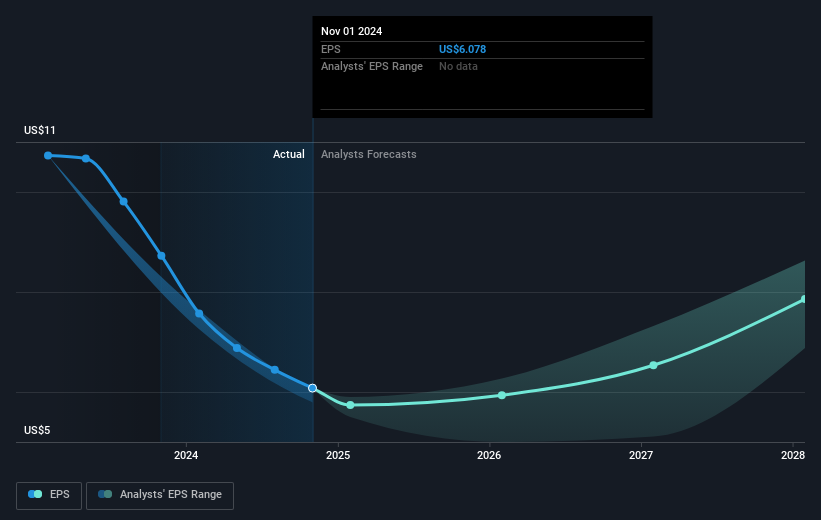

Over a longer-term perspective, Dollar General's share price growth of 35% in the last quarter reflects these efforts, although it trails the broader market's 11.1% return and the Consumer Retailing industry's 31% return over the same period. Analysts anticipate modest growth in revenue and earnings with dollar figures projected to rise from US$40.61 billion in revenue to US$45.8 billion, and earnings from US$1.13 billion to US$1.5 billion by 2028, provided the economic headwinds are managed effectively. Although the current share price of US$93.66 is above the consensus price target of US$90.50, this minor discrepancy suggests analysts see the company as fairly valued amidst its ongoing initiatives and cost challenges.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:DG

Dollar General

A discount retailer, provides various merchandise products in the southern, southwestern, midwestern, and eastern United States.

Undervalued established dividend payer.

Similar Companies

Market Insights

Community Narratives