- United States

- /

- Food and Staples Retail

- /

- NasdaqGS:CART

Instacart (CART): Revisiting Valuation After Recent Outperformance and Flat Year-to-Date Share Price

Reviewed by Simply Wall St

Maplebear (CART) has quietly outperformed the broader market over the past month, climbing about 19%, even as its past 3 months remain slightly negative. That mix has investors revisiting Instacart’s underlying fundamentals.

See our latest analysis for Maplebear.

Looking beyond the recent jump, Maplebear’s roughly flat year to date share price return but negative 1 year total shareholder return suggests momentum is only just starting to rebuild as investors reassess its growth and risk profile.

If Instacart’s recent move has you thinking about what else could be re rating, it might be worth exploring high growth tech and AI stocks as potential next wave beneficiaries.

With shares hovering near flat for the year despite solid revenue and profit growth, plus a double digit discount to analyst targets, is this still an underappreciated grocery tech platform, or is the market already pricing in its next leg of expansion?

Most Popular Narrative Narrative: 14.9% Undervalued

With the narrative fair value sitting notably above the last close of $43.13, the story leans toward meaningful upside if its growth thesis holds.

Deepening enterprise partnerships and a growing suite of omnichannel retailer integrations (such as Storefront, Carrot Ads, Caper Carts, Carrot Tags) are increasing stickiness with major retail chains, creating new recurring revenue streams and driving higher margin, non transaction based revenues (e.g., advertising, in store tech). This development is making the business model less volatile and supporting sustainable margin expansion and earnings resilience.

To see the math behind this confidence boost, from mid single digit top line expansion to richer margins and a premium earnings multiple, review the full narrative for a detailed breakdown.

Result: Fair Value of $50.70 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, rising labor and regulatory pressures, alongside intensifying competition from retailer-led delivery, could compress margins and slow the expected earnings trajectory.

Find out about the key risks to this Maplebear narrative.

Another Take On Valuation

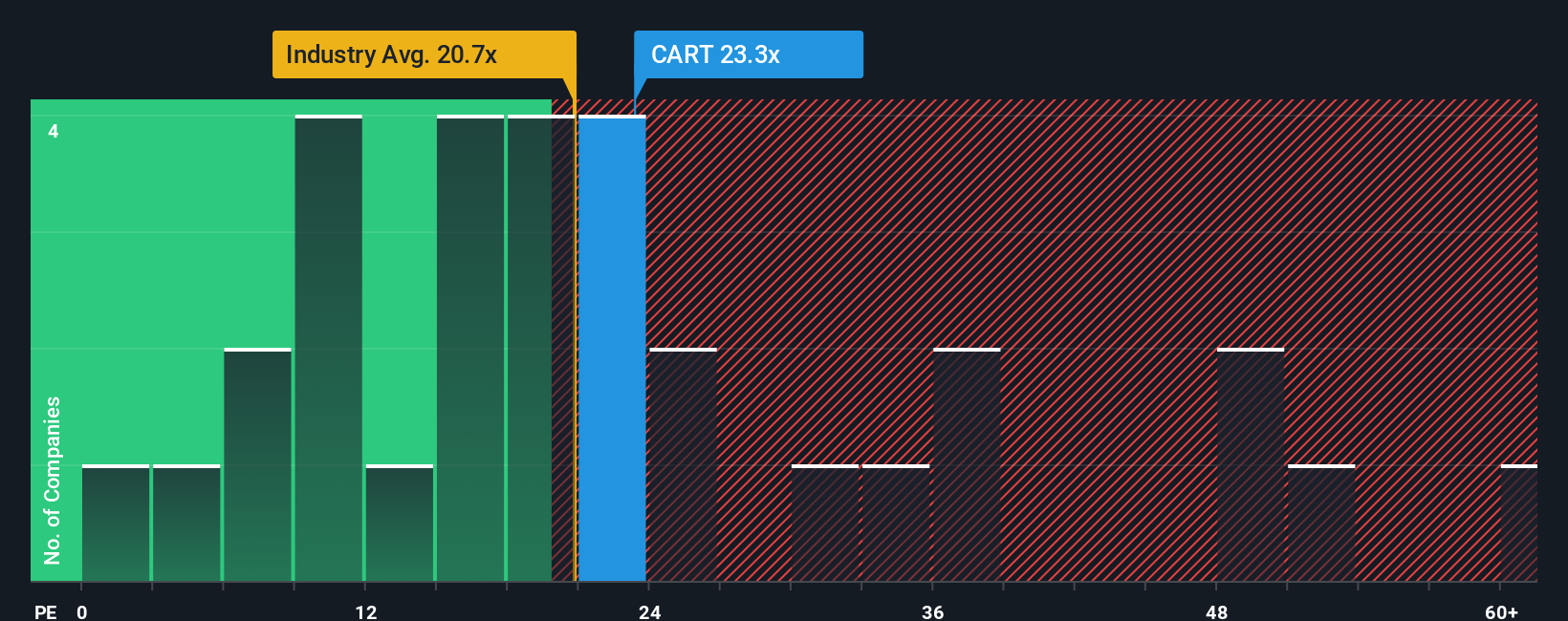

On simple earnings metrics, the picture flips. Maplebear trades on a 22.4x P/E, richer than both the US consumer retailing industry at 20.7x and peers at 19.4x. This is also above a fair ratio of 18x, suggesting investors may be paying up today for execution risk.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Maplebear Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a custom view in minutes with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Maplebear.

Ready for your next investing edge?

Before markets move on without you, put Simply Wall St’s screener to work and line up your next wave of high conviction ideas today.

- Capitalize on potential mispricing opportunities by targeting companies flagged as trading below intrinsic value with these 912 undervalued stocks based on cash flows.

- Ride the momentum of innovation by focusing on cutting edge names shaping the future of automation and machine learning through these 26 AI penny stocks.

- Strengthen your income strategy by pinpointing reliable payers with sustainable cash flows using these 15 dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CART

Maplebear

Maplebear Inc., doing business as Instacart, engages in the provision of online grocery shopping services to households in North America.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)