- United States

- /

- Food and Staples Retail

- /

- NasdaqGS:CART

Instacart (CART): Revisiting Valuation After a 14% Monthly Share Price Rebound

Reviewed by Simply Wall St

Maplebear (CART) has been quietly grinding higher, with the stock up around 14% over the past month after a choppy past 3 months. That move has investors revisiting Instacart’s fundamentals.

See our latest analysis for Maplebear.

Zooming out, that recent 14.1% 1 month share price return has only modestly improved Maplebear’s 1 year total shareholder return of 7.6%. This suggests momentum is building but not yet euphoric at around $44.96 a share.

If Instacart’s move has you rethinking what “quiet compounders” can look like, it is worth scanning fast growing stocks with high insider ownership as a next step for fresh ideas.

With profits rising and shares still trading below analyst targets and some intrinsic value estimates, the key question now is whether Instacart remains undervalued or whether the market is already pricing in most of its future growth.

Most Popular Narrative: 11.3% Undervalued

With Maplebear closing at $44.96 against a most-followed fair value of $50.70, the narrative points to upside that hinges on execution and durability of growth.

Deepening enterprise partnerships and a growing suite of omnichannel retailer integrations (such as Storefront, Carrot Ads, Caper Carts, Carrot Tags) are increasing stickiness with major retail chains, creating new recurring revenue streams and driving higher margin, non transaction based revenues (e.g., advertising, in store tech). This is making the business model less volatile and supporting sustainable margin expansion and earnings resilience.

Curious how steady, mid single digit growth and rising margins can still justify a richer future earnings multiple than many retailers enjoy today? The narrative leans heavily on expanding high margin revenue streams and a confident outlook for profit scalability. Want to see the exact earnings and revenue path that underpins that fair value call, plus the multiple it assumes years from now? Dive into the full narrative to unpack the numbers behind this valuation story.

Result: Fair Value of $50.70 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, rising labor and regulatory pressures, alongside intensifying competition and retailer-led delivery, could squeeze margins and derail that optimistic earnings trajectory.

Find out about the key risks to this Maplebear narrative.

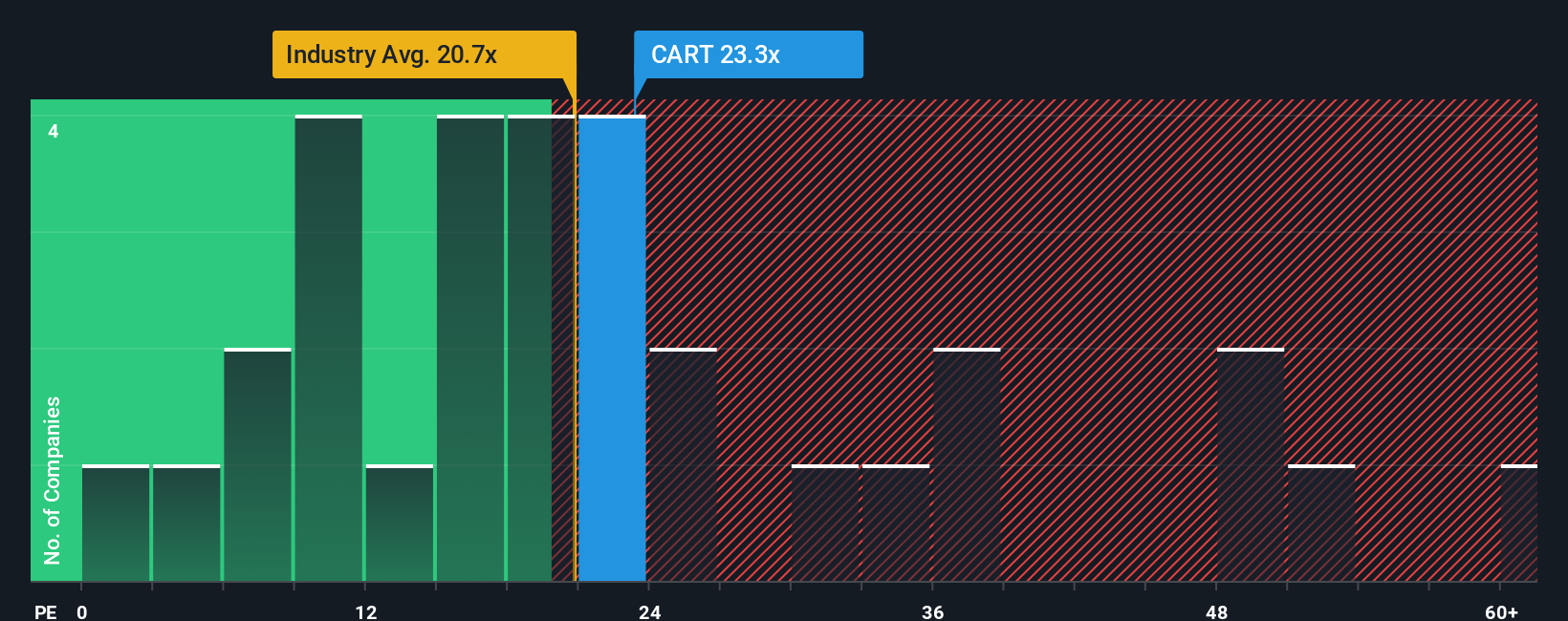

Another Lens on Valuation

On earnings, Maplebear looks less generous. Its P E of 23.4x is only slightly above the Consumer Retailing average of 22.9x and above its own fair ratio of 18.1x, suggesting the market already prices in a lot of good news. Is that enough margin of safety for you?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Maplebear Narrative

If this framework does not quite match your view, or you simply prefer hands on research, you can build a custom narrative in minutes: Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Maplebear.

Ready for your next investing move?

Before you stop at Maplebear, consider putting your capital to work by scanning fresh ideas on Simply Wall St’s screener so tomorrow’s winners do not slip past you.

- Target reliable income streams by reviewing these 13 dividend stocks with yields > 3% that could strengthen your portfolio’s cash flow and reduce reliance on market swings.

- Explore potential growth opportunities by evaluating these 26 AI penny stocks that sit at the crossroads of innovation, data, and long term earnings power.

- Look for potential valuation opportunities by filtering these 903 undervalued stocks based on cash flows that the market has not fully appreciated yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CART

Maplebear

Maplebear Inc., doing business as Instacart, engages in the provision of online grocery shopping services to households in North America.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)