Advertisement

- United States

- /

- Luxury

- /

- NYSE:NKE

NIKE, Inc.'s (NYSE:NKE) Business Is Yet to Catch Up With Its Share Price

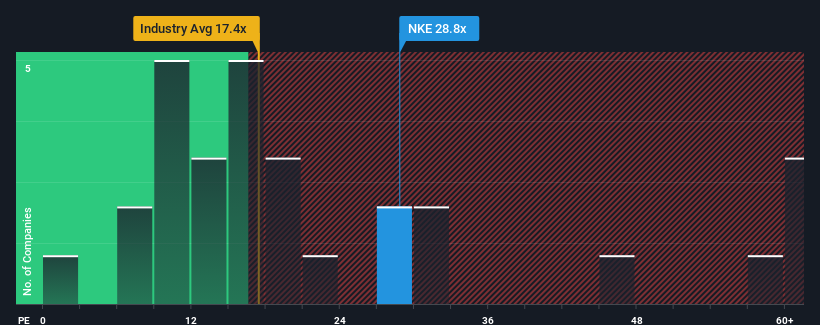

When close to half the companies in the United States have price-to-earnings ratios (or "P/E's") below 16x, you may consider NIKE, Inc. (NYSE:NKE) as a stock to avoid entirely with its 28.8x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

Recent times haven't been advantageous for NIKE as its earnings have been falling quicker than most other companies. It might be that many expect the dismal earnings performance to recover substantially, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for NIKE

What Are Growth Metrics Telling Us About The High P/E?

The only time you'd be truly comfortable seeing a P/E as steep as NIKE's is when the company's growth is on track to outshine the market decidedly.

Retrospectively, the last year delivered a frustrating 3.7% decrease to the company's bottom line. Even so, admirably EPS has lifted 93% in aggregate from three years ago, notwithstanding the last 12 months. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

Looking ahead now, EPS is anticipated to climb by 14% each year during the coming three years according to the analysts following the company. That's shaping up to be similar to the 12% per year growth forecast for the broader market.

In light of this, it's curious that NIKE's P/E sits above the majority of other companies. It seems most investors are ignoring the fairly average growth expectations and are willing to pay up for exposure to the stock. Although, additional gains will be difficult to achieve as this level of earnings growth is likely to weigh down the share price eventually.

The Bottom Line On NIKE's P/E

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

Our examination of NIKE's analyst forecasts revealed that its market-matching earnings outlook isn't impacting its high P/E as much as we would have predicted. When we see an average earnings outlook with market-like growth, we suspect the share price is at risk of declining, sending the high P/E lower. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

Many other vital risk factors can be found on the company's balance sheet. Take a look at our free balance sheet analysis for NIKE with six simple checks on some of these key factors.

Of course, you might also be able to find a better stock than NIKE. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if NIKE might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:NKE

NIKE

Engages in the design, development, marketing, and sale of athletic footwear, apparel, equipment, accessories, and services worldwide.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|5.7% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.0% undervalued

BL

Community Contributor