Advertisement

- United States

- /

- Luxury

- /

- NYSE:HBI

Will Premiumization and Category Expansion Change Hanesbrands' (HBI) Narrative?

Simply Wall St

Reviewed by Sasha Jovanovic

- In recent days, Hanesbrands has drawn attention from investors as it pushes forward with premiumization efforts and expands into new categories like loungewear and scrubs amid operational headwinds.

- This shift comes as the company seeks higher margins and pricing power, but persistent softness in core categories and challenges in sustaining cost reductions continue to raise questions about its path to recovery.

- We'll explore how Hanesbrands' renewed focus on premiumization and category expansion could reshape its long-term investment outlook.

We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Hanesbrands Investment Narrative Recap

To be a Hanesbrands shareholder, you need to believe the company’s premiumization and category expansion will drive sustained earnings growth, despite its exposure to mature product lines and industry headwinds. The recent share price momentum highlights growing investor optimism on these turnaround efforts, but softness in U.S. intimates remains the most important near-term catalyst, and the company’s ability to protect margins through cost efficiencies continues to be the biggest risk. The driver for lasting recovery remains execution on product innovation and brand elevation, while the risk of margin compression from fading cost reductions still overshadows results in the short run; the recent positive news does not materially change these dynamics. As for announcements, the proposed acquisition by Gildan Activewear stands out: this US$2.2 billion deal, valuing Hanesbrands at US$4.4 billion enterprise value, could alter the investment case and near-term catalysts, shifting focus from operational recovery to deal closure and integration. Yet despite recent gains, investors should contrast this optimism with the reality that persistent core category weakness and top-line challenges can still...

Read the full narrative on Hanesbrands (it's free!)

Hanesbrands is expected to reach $3.6 billion in revenue and $274.0 million in earnings by 2028. This outlook is based on a projected revenue decline of 0.4% annually and a $104.0 million increase in earnings from the current $170.0 million.

Uncover how Hanesbrands' forecasts yield a $6.26 fair value, a 7% downside to its current price.

Exploring Other Perspectives

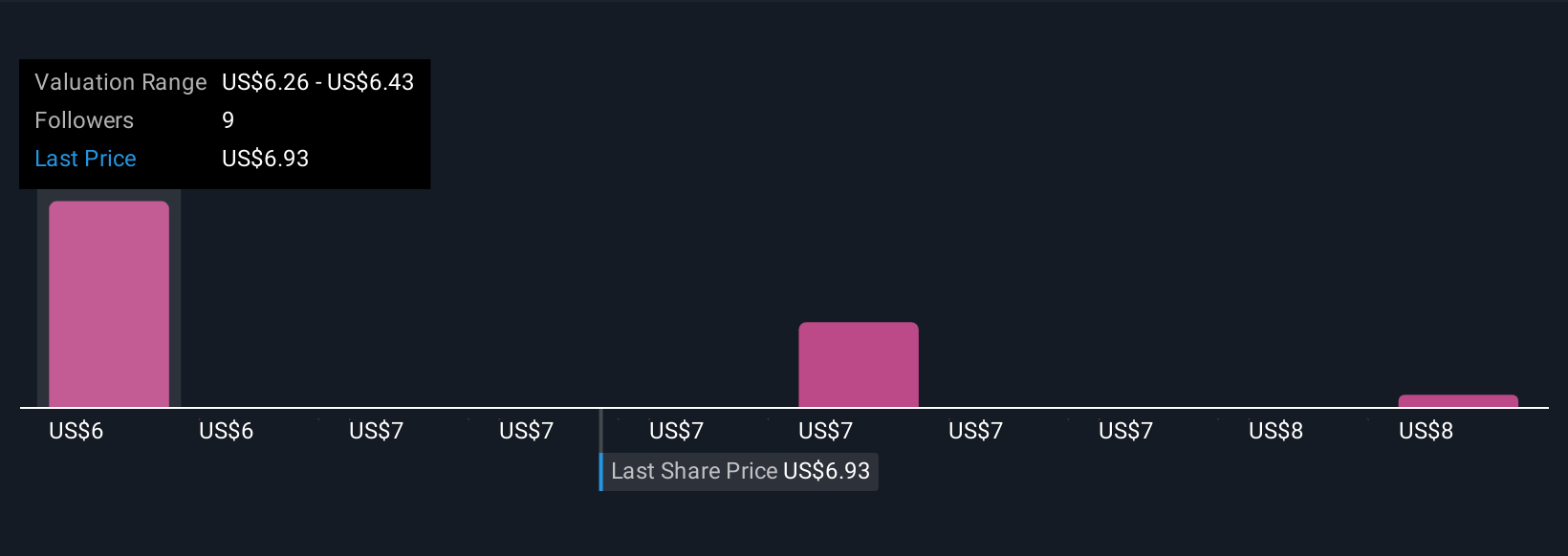

Simply Wall St Community fair value estimates range from US$6.26 to US$8.03 per share, based on 3 individual perspectives. While views vary, ongoing softness in the U.S. intimates segment could continue to weigh on the business, see how others interpret the data and risks.

Explore 3 other fair value estimates on Hanesbrands - why the stock might be worth as much as 19% more than the current price!

Build Your Own Hanesbrands Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Hanesbrands research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Hanesbrands research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hanesbrands' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Find companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hanesbrands might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HBI

Hanesbrands

Designs, manufactures, sources, and sells a range of range of innerwear apparel for men, women, and children in the Americas, Europe, the Asia pacific, and internationally.

Good value with limited growth.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|10.9% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor