Advertisement

- United States

- /

- Leisure

- /

- NasdaqGS:HAS

Hasbro (HAS): Evaluating Valuation After Boston Relocation and New Disney Partnership Announcements

Reviewed by Simply Wall St

If you’re wondering what to make of Hasbro (HAS) after a flurry of major announcements, you’re not alone. The company’s decision to relocate its Rhode Island operations to Boston’s Seaport District is a significant step, aimed at fueling innovation and making Hasbro an even bigger draw for top talent. Add expanded brand partnerships, including a deeper collaboration with Disney and fresh launches of iconic names like EASY-BAKE and PLAYSKOOL at Walmart, and you have a company clearly focused on recharging its core business and pushing into new territory.

For shareholders, the moves come on the back of a strong year in the stock. Over the past year, Hasbro’s shares are up roughly 22%, with momentum building. Shares are up 15% in the past three months and more than 40% year-to-date. Recent launches and strategic shifts are sending signals that the company is serious about longer-term growth, though swings earlier in the year have shown investors remain sensitive to how these moves translate into actual performance.

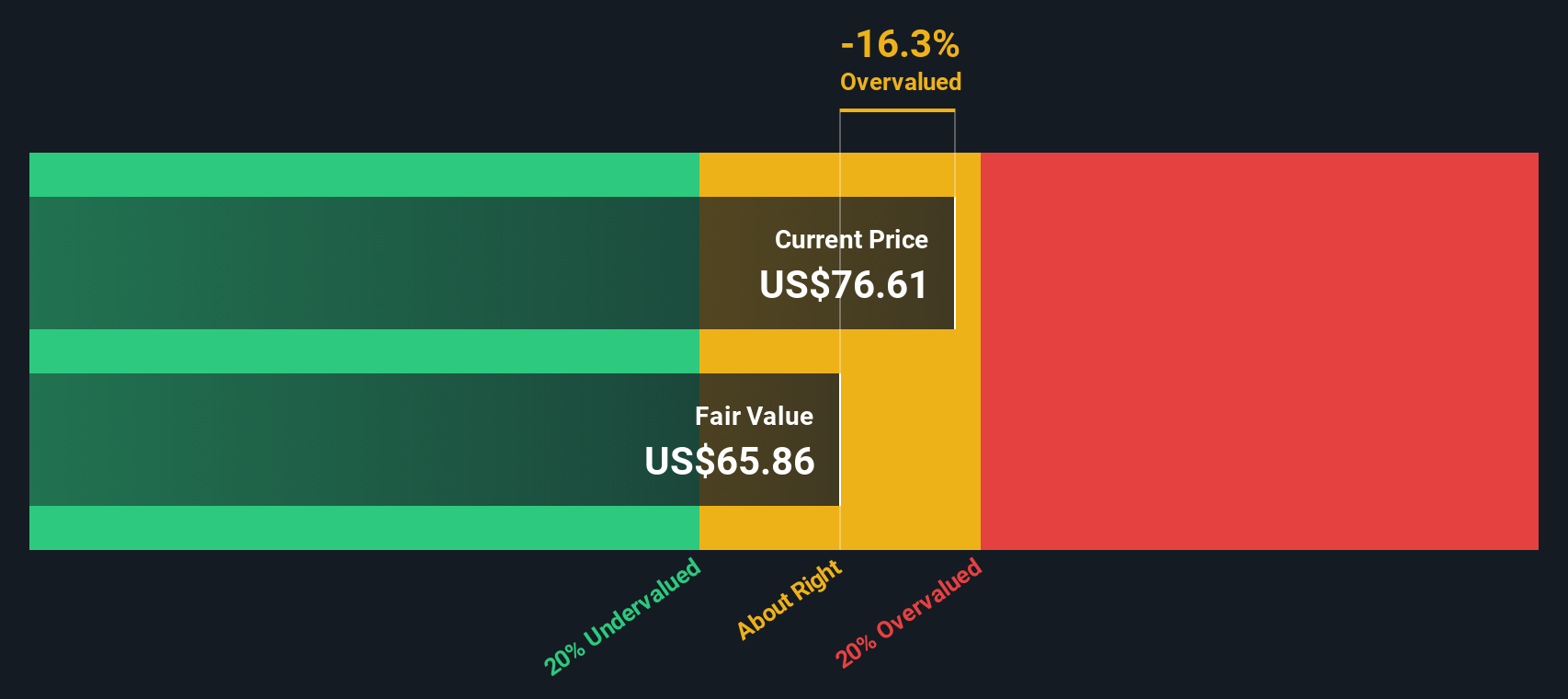

So the big question is, with shares already rallying this year, is Hasbro undervalued after this burst of activity, or are investors already baking future growth into the current price?

Most Popular Narrative: 4076.8% Overvalued

According to the most widely discussed narrative, Hasbro's current valuation is far detached from business reality, with the stock considered vastly overvalued compared to fair value.

Almost none of these brands I listed are making a profit. Yes, I am oversimplifying their stories, but a deep dive into each of them would render novels hundreds of pages thick, brimming with examples of these brands being underutilized and damaged because of poor business decisions.

Think you understand Hasbro's true worth? There is a twist that turns the usual financials on their head. The narrative draws from dramatic changes in forward earnings and a radical recalibration of future profit margins, leading to its shocking conclusion. Curious what drives the mountain of overvaluation claims, or which assumptions are behind this massive mismatch? Press on to see the controversial calculations that set this price target.

Result: Fair Value of $1.90 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, a sudden turnaround in key brands or unexpected licensing revenue growth could quickly challenge even the most bearish outlook.

Find out about the key risks to this Hasbro narrative.Another View: What Does the SWS DCF Model Say?

While the popular narrative paints Hasbro as highly overvalued, our SWS DCF model offers a strikingly different perspective. This approach suggests the shares may actually be trading below estimated fair value. Which story matches reality: numbers or narrative?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Hasbro Narrative

If you have your own perspective or want to dig into the details yourself, you can build your own Hasbro view in just a few minutes. Do it your way

A great starting point for your Hasbro research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Ready for More Smart Investment Ideas?

Don’t let great opportunities slip by. Use the Simply Wall Street Screener to quickly access stocks backed by solid trends and future-focused insights. Open up new possibilities now, before they take off.

- Grow your wealth with steady income by scanning for promising dividend stocks with yields > 3% that consistently deliver yields above 3%.

- Ride the momentum of tomorrow’s innovation by pinpointing groundbreaking quantum computing stocks that are making waves in the quantum computing space.

- Target long-term winners by uncovering smartly priced undervalued stocks based on cash flows based on their future cash flow potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hasbro might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NasdaqGS:HAS

Hasbro

Operates as a toy and game company in the United States, Europe, Canada, Mexico, Latin America, Australia, China, and Hong Kong.

Very undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Optimi Health ·

The Only Psychedelic Company Already Selling MDMA and Psilocybin to Real Patients, Yet Priced Like It Doesn’t Exist

Fair Value:US$1158.7% undervalued

32 followersusers have followed this narrative

2 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7721.6% undervalued

50 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9220.2% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$1908.3% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

Recently Updated Narratives

RE

Reex on Unibap Space Solutions ·

Long-term bet on Europe's strategic space autonomy (2030–2055)

Fair Value:SEK 36.0176.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AV

Averagemike on Samsara ·

Samsara's Future PE Will Soar to 337.7x and the Future is Bright

Fair Value:US$57.34k99.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

John_Eric on ServiceNow ·

The Company Nobody Brags About

Fair Value:US$266.0164.1% undervalued

32 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75029.1% undervalued

103 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6514.6% undervalued

69 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5449.5% undervalued

64 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

PI

PittTheYounger on International Consolidated Airlines Group ·

IAG is a surefire investment in the airline space, once and if the Iran War is finally over in the sense of a lasting peace agreement or at least a reliable ceasefire. Before that, however and by the same token, IAG ranks among the most vulnerable if spring's kerosene fears return to the fore, as is very likely right now.

0

|0