- United States

- /

- Commercial Services

- /

- NYSE:VSTS

Why Vestis (VSTS) Is Up 8.6% After Posting Wider Losses And Flat 2026 Revenue Guidance

Reviewed by Sasha Jovanovic

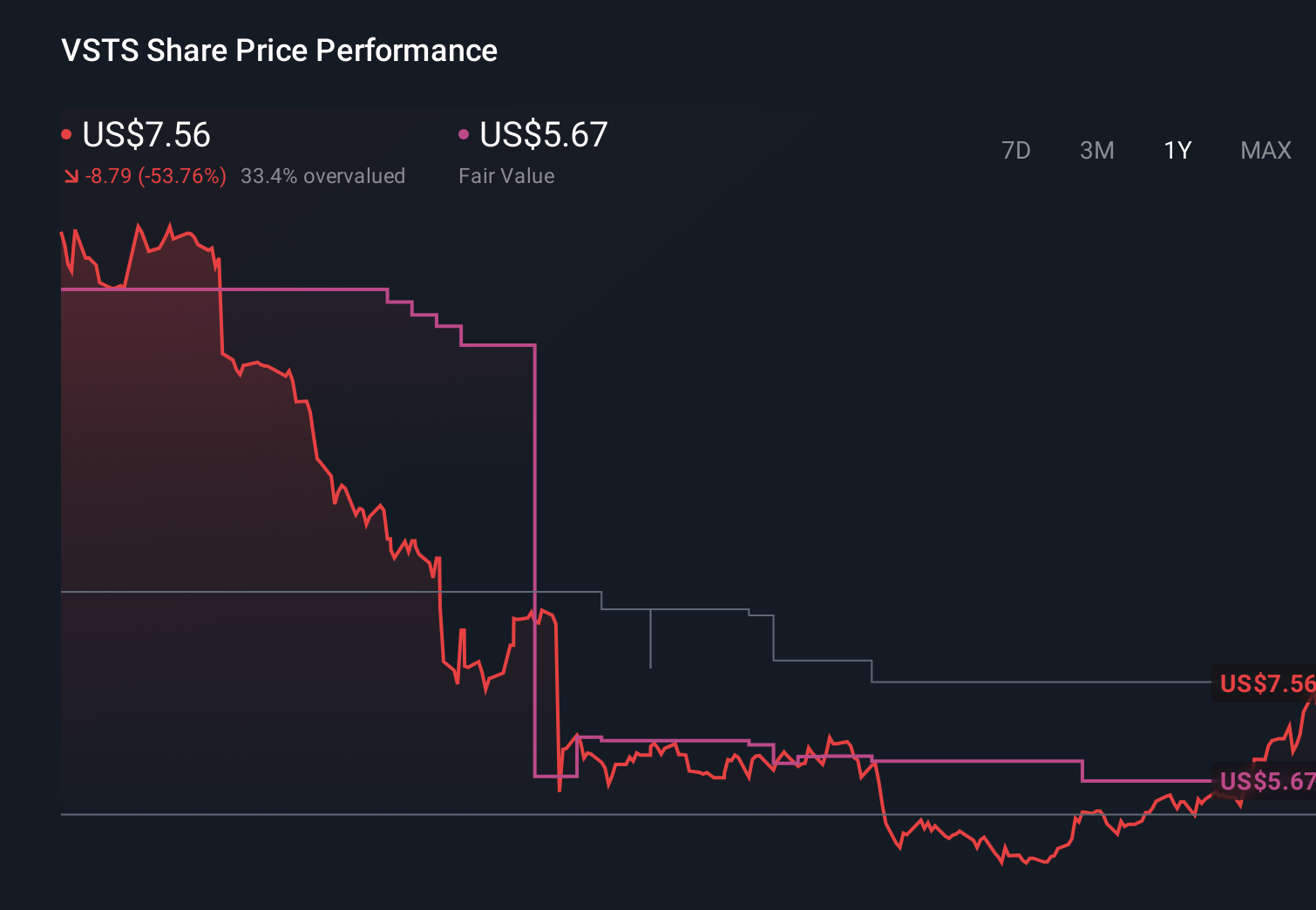

- In December 2025, Vestis Corporation reported fourth-quarter sales of US$712.01 million and a quarterly net loss of US$12.55 million, alongside a full-year net loss of US$40.22 million on sales of US$2,734.84 million, reversing the prior year’s profitability.

- Alongside these widened losses, Vestis guided for fiscal 2026 revenue to be flat to down 2% versus normalized 2025 levels, underscoring management’s cautious outlook on demand and execution.

- We’ll now examine how Vestis’s wider losses and flat-to-down 2026 revenue outlook might reshape the company’s investment narrative.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Vestis Investment Narrative Recap

To own Vestis today, you need to believe that its uniform rental and workplace supplies business can return to steady growth and healthier margins despite a swing to losses in 2025. The fresh guidance for flat to slightly lower 2026 revenue does not fundamentally change the near term story: the key catalyst remains execution on pricing and efficiency initiatives, while the biggest risk is that revenue softness and margin pressure persist long enough to strain an already leveraged balance sheet.

The latest full year 2025 results, showing US$2,734.84 million in sales but a US$40.22 million net loss versus a prior year profit, are central to this shift in narrative. They tie directly into concerns about customer churn, weaker pricing on new contracts, and the need for operational upgrades, which together will likely shape whether Vestis can stabilize revenue and margins before leverage and interest costs become a more serious constraint.

Yet investors should be aware that if customer churn keeps outpacing new wins and leverage stays high, Vestis could...

Read the full narrative on Vestis (it's free!)

Vestis’ narrative projects $2.9 billion revenue and $62.5 million earnings by 2028.

Uncover how Vestis' forecasts yield a $5.67 fair value, a 25% downside to its current price.

Exploring Other Perspectives

The single Simply Wall St Community fair value estimate of US$7.86 for Vestis shows how one retail view can differ from current pricing. You should weigh that against the risk that ongoing contract churn and weaker pricing could prolong revenue and margin pressure, with clear implications for how the business performs over the next few years.

Explore another fair value estimate on Vestis - why the stock might be worth as much as $7.86!

Build Your Own Vestis Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Vestis research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Vestis research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vestis' overall financial health at a glance.

Interested In Other Possibilities?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- We've found 13 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:VSTS

Vestis

Provides uniform rentals and workplace supplies in the United States and Canada.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)