Advertisement

- United States

- /

- Professional Services

- /

- NYSE:TRU

How Investors May Respond To TransUnion (TRU) Amid Rising Credit Scoring Competition and Price Cuts

Simply Wall St

Reviewed by Sasha Jovanovic

- In recent weeks, heightened competition in the mortgage credit reporting market emerged after FICO enabled direct licensing of its scores to mortgage lenders, prompting Equifax to aggressively cut prices and promote VantageScore 4.0 as an alternative.

- This shift could materially influence TransUnion by impacting market share, pricing power, and the competitive dynamics among major credit bureaus in a regulated industry.

- We'll examine how intensifying rivalry in credit scoring may influence TransUnion's future growth narrative and its positioning in the financial services ecosystem.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

TransUnion Investment Narrative Recap

Owning TransUnion means believing in the long-term value of trusted, scaled consumer credit data and analytics, even as disruptive shifts reshape the mortgage credit reporting market. The recent pricing and access changes introduced by FICO and Equifax bring competitive pressure, particularly in mortgage, but appear unlikely to materially alter the current main revenue driver, global demand for identity, analytics, and risk solutions, or displace the present top risk of pricing pressure and service commoditization affecting profit margins.

Of the recent company updates, TransUnion’s ongoing strategic buybacks, 494,500 shares repurchased for US$41.67 million, are most relevant here. This capital return effort highlights how management continues to support shareholder value as market competition intensifies in certain segments, underscoring that consistent cash flow and measured capital allocation remain a core part of the investment case.

In contrast, pricing pressure and service commoditization may still squeeze margins in ways that ...

Read the full narrative on TransUnion (it's free!)

TransUnion's narrative projects $5.6 billion revenue and $869.9 million earnings by 2028. This requires 8.4% yearly revenue growth and a $477.9 million earnings increase from $392.0 million today.

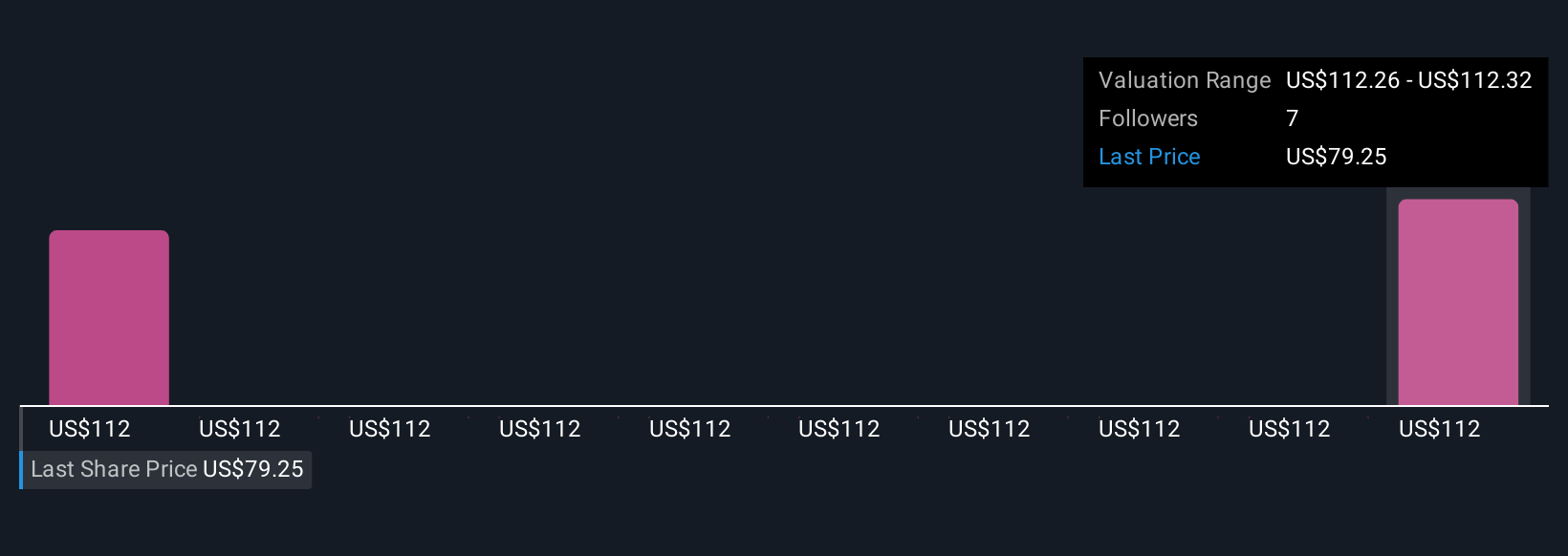

Uncover how TransUnion's forecasts yield a $111.80 fair value, a 44% upside to its current price.

Exploring Other Perspectives

Fair value estimates from the Simply Wall St Community cluster tightly between US$111.80 and US$112.94 based on two individual analyses. While many see revenue growth potential, mounting pricing competition among credit bureaus remains a factor that could reshape profitability longer term, consider how diverse investor outlooks can be and explore several perspectives for a fuller view.

Explore 2 other fair value estimates on TransUnion - why the stock might be worth just $111.80!

Build Your Own TransUnion Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your TransUnion research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free TransUnion research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate TransUnion's overall financial health at a glance.

No Opportunity In TransUnion?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TransUnion might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TRU

TransUnion

Operates as a global consumer credit reporting agency that provides risk and information solutions.

Proven track record and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor