David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Franklin Covey Co. (NYSE:FC) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Franklin Covey

What Is Franklin Covey's Debt?

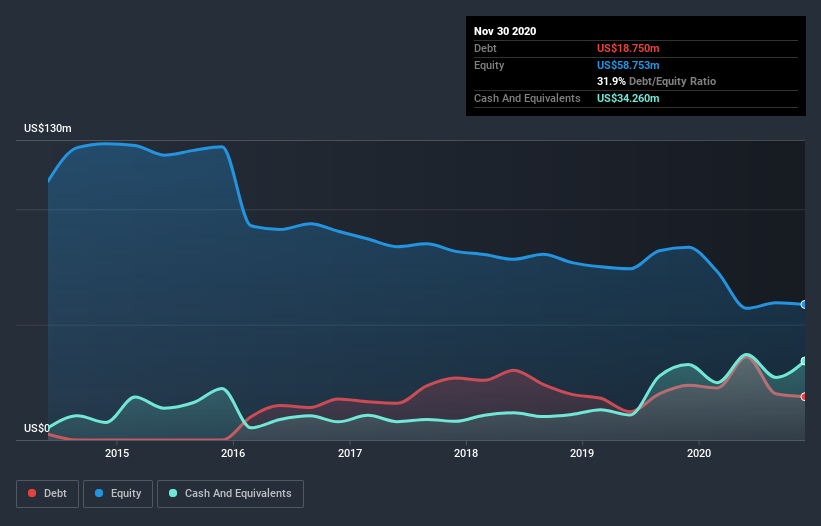

You can click the graphic below for the historical numbers, but it shows that Franklin Covey had US$18.8m of debt in November 2020, down from US$23.8m, one year before. But it also has US$34.3m in cash to offset that, meaning it has US$15.5m net cash.

How Strong Is Franklin Covey's Balance Sheet?

The latest balance sheet data shows that Franklin Covey had liabilities of US$96.6m due within a year, and liabilities of US$41.0m falling due after that. Offsetting these obligations, it had cash of US$34.3m as well as receivables valued at US$43.1m due within 12 months. So its liabilities total US$60.3m more than the combination of its cash and short-term receivables.

Of course, Franklin Covey has a market capitalization of US$379.3m, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Despite its noteworthy liabilities, Franklin Covey boasts net cash, so it's fair to say it does not have a heavy debt load!

Unfortunately, Franklin Covey saw its EBIT slide 9.4% in the last twelve months. If that earnings trend continues then its debt load will grow heavy like the heart of a polar bear watching its sole cub. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Franklin Covey's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. Franklin Covey may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Happily for any shareholders, Franklin Covey actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Summing up

Although Franklin Covey's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of US$15.5m. The cherry on top was that in converted 723% of that EBIT to free cash flow, bringing in US$29m. So we don't have any problem with Franklin Covey's use of debt. Even though Franklin Covey lost money on the bottom line, its positive EBIT suggests the business itself has potential. So you might want to check out how earnings have been trending over the last few years.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you decide to trade Franklin Covey, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NYSE:FC

Franklin Covey

Provides training and consulting services in the areas of execution, sales performance, productivity, customer loyalty, leadership, and educational improvement for organizations and individuals worldwide.

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Community Narratives