Advertisement

- United States

- /

- Professional Services

- /

- NYSE:ALIT

Alight (ALIT) Is Up 5.7% After Goldman Partnership and Earnings Beat Are Recurring Revenues Set to Accelerate?

Simply Wall St

Reviewed by Simply Wall St

- Alight, Inc. recently posted stronger-than-expected second-quarter results and announced a partnership with Goldman Sachs Asset Management to enhance its Worklife platform.

- While these developments highlight growing demand for Alight’s cloud-based HR solutions, the company has adjusted its full-year revenue guidance due to slower deal closures.

- We'll explore how the new Goldman Sachs collaboration could shape Alight's long-term investment narrative and prospects for recurring revenue growth.

The latest GPUs need a type of rare earth metal called Terbium and there are only 28 companies in the world exploring or producing it. Find the list for free.

Alight Investment Narrative Recap

For investors considering Alight, Inc., the core story hinges on a recovery in recurring revenue growth driven by increased adoption of integrated, cloud-based HR solutions, despite significant losses and cautious outlooks. While recent strong second-quarter results and the new Goldman Sachs Asset Management partnership offer a positive signal for long-term platform expansion, the biggest short-term catalyst, rebounding deal closures, remains tempered by continued delays in the sales cycle and revised full-year guidance; recent news does not materially change this risk profile.

Among recent announcements, the partnership to enhance the Worklife platform stands out. This move directly addresses one of Alight’s primary growth catalysts: expanding its suite of integrated HR and wealth management services to existing large enterprise clients, with the aim of driving higher recurring revenue and improving earnings visibility as deal flow eventually recovers.

Yet, despite this potential, lengthening sales cycles still raise concerns investors should be aware of...

Read the full narrative on Alight (it's free!)

Alight's narrative projects $2.5 billion in revenue and $142.2 million in earnings by 2028. This requires 3.0% yearly revenue growth and a $1.24 billion increase in earnings from the current earnings of -$1.1 billion.

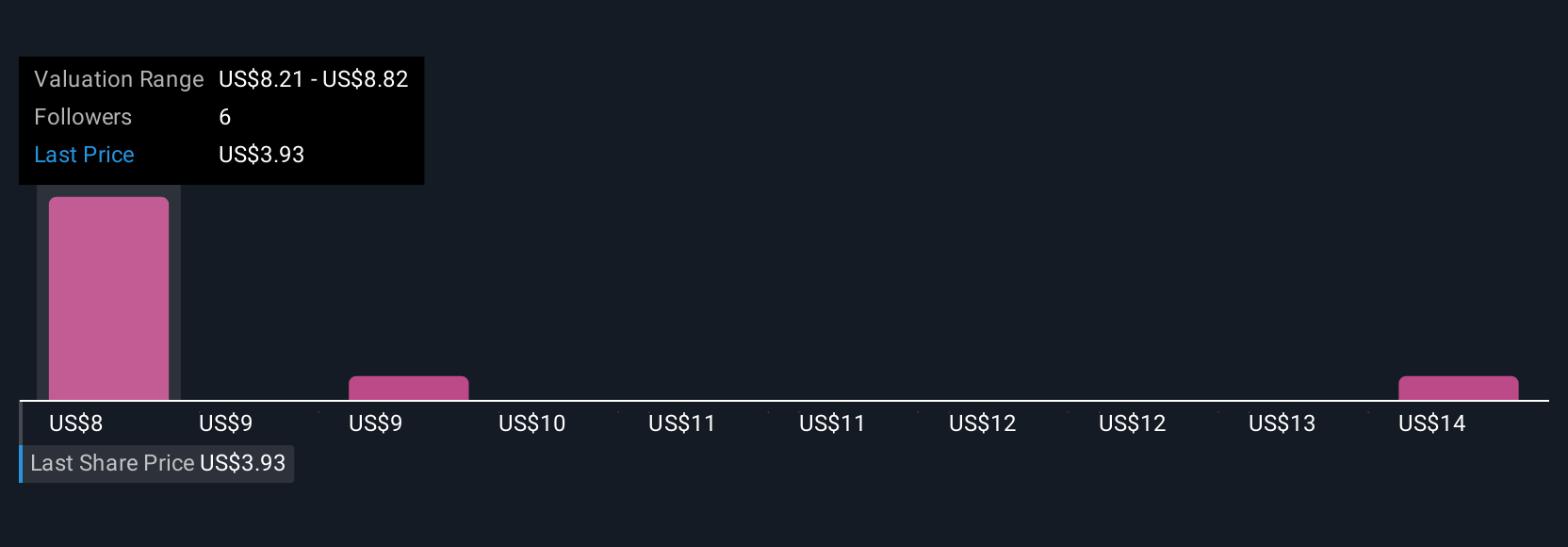

Uncover how Alight's forecasts yield a $8.21 fair value, a 112% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members valued Alight between US$8.21 and US$14.13, based on three independent approaches. While these views show broad optimism, recall that persistent delays in client signings may weigh heavily on the company’s ability to realize near-term growth, consider alternate outlooks before forming your own perspective.

Explore 3 other fair value estimates on Alight - why the stock might be worth just $8.21!

Build Your Own Alight Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Alight research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Alight research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Alight's overall financial health at a glance.

No Opportunity In Alight?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Find companies with promising cash flow potential yet trading below their fair value.

- This technology could replace computers: discover 23 stocks that are working to make quantum computing a reality.

- AI is about to change healthcare. These 27 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ALIT

Undervalued with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

Gaxos.ai: Early-Stage AI Innovator in Gaming & Health

Fair Value US$2.21|6.3% undervalued

JO

Community Contributor

After the AI Party: A Sobering Look at Microsoft's Future

Fair Value US$500.00|0.9% overvalued

PI

Community Contributor

Amazon's Future Rises as Stock Price Falls: A Long-Term Investment Vision

Fair Value US$234.75|2.9% undervalued

ZW

Community Contributor