Advertisement

- United States

- /

- Professional Services

- /

- NasdaqGS:PCTY

Paylocity (PCTY): Evaluating Valuation After High-Profile NHL Partnerships Expand Industry Presence

Simply Wall St

Reviewed by Kshitija Bhandaru

Paylocity Holding (PCTY) has drawn attention with its new partnerships across the NHL, including multi-year deals with major teams. These collaborations highlight its HR technology and expand its profile in the enterprise sector.

See our latest analysis for Paylocity Holding.

Momentum for Paylocity has been mixed lately, as high-profile NHL partnerships and new tech features have not yet turned around a challenging run for the shares. Despite recent buzz, the year-to-date share price return sits at -22.85%. The 1-year total shareholder return of -8.5% reflects ongoing headwinds, though the company is still posting healthy long-term gains on efficiency and capital use.

If you're curious about which other innovative platforms are capturing investor interest, this is a great moment to broaden your search and discover fast growing stocks with high insider ownership

With shares trading well below analyst targets and long-term growth metrics telling a mixed story, the real question is whether Paylocity is now undervalued or if the market has already priced in its future prospects, leaving little room for upside.

Most Popular Narrative: 31.6% Undervalued

Paylocity’s most popular valuation narrative pegs its fair value well above today’s $150.49 share price, highlighting strong upside potential according to consensus forecasts. This perspective draws a sharp contrast between a discounted stock and ambitious growth and profitability assumptions for the years ahead.

Expansion of Paylocity's unified HR and finance platform, coupled with advanced AI-powered features, is enhancing automation and streamlining complex workflows for clients. This positions the company to capture growing demand from businesses undergoing digital transformation and is likely to drive higher recurring revenue and average revenue per client over time.

Which numbers are powering this bullish target? The narrative is built on aggressive projections for revenue growth, margin expansion, and profitability improvements. Want to see what makes this thesis tick? The boldest financial leap is hidden in its future earnings formula. Take a look at the full narrative to spot what sets these predictions apart.

Result: Fair Value of $220.16 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, slowing revenue growth or slower than expected adoption of new products like Paylocity for Finance could challenge the optimistic outlook presented by analysts.

Find out about the key risks to this Paylocity Holding narrative.

Another View: What Do Market Ratios Suggest?

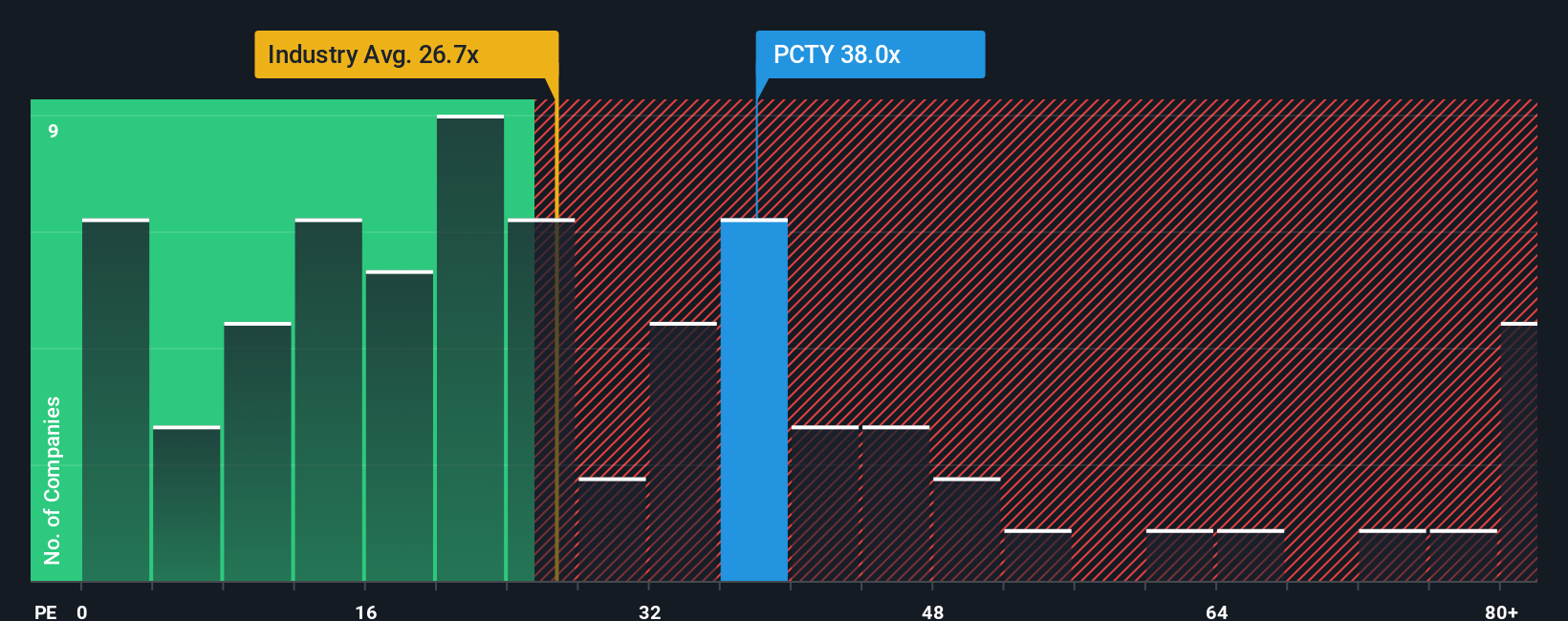

While analyst targets point to upside, traditional price-to-earnings ratios offer a more cautious perspective. Paylocity trades at 36.5x earnings, notably higher than both its peer average of 23.9x and the Professional Services industry’s 25.2x. Our fair ratio signals the market could reset closer to 27.4x, rather than remain at today's premium. Does this indicate froth built on optimism, or room for fundamentals to catch up?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Paylocity Holding Narrative

Feel free to take a closer look at the numbers and shape your own interpretation. Dig into the details and see what story you uncover. If you want to build your own thesis in just a few minutes, Do it your way

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Paylocity Holding.

Looking for more investment ideas?

You don’t want to miss these emerging trends and unique opportunities. Take your next step toward smarter investing with the Simply Wall Street Screener tools below.

- Target rising returns and future-focused businesses by starting with these 19 dividend stocks with yields > 3%, where yield meets financial strength above 3%.

- Capitalize on AI’s explosive potential by scanning for market leaders in the field with these 24 AI penny stocks as they advance the next tech wave.

- Capture outstanding value by reviewing these 898 undervalued stocks based on cash flows to screen for quality companies priced below their cash flow potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:PCTY

Paylocity Holding

Provides cloud-based human capital management, payroll software, and spend management solutions for the workforce in the United States.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor