- United States

- /

- Professional Services

- /

- NasdaqGS:EXLS

Does ExlService Holdings (NASDAQ:EXLS) Have A Healthy Balance Sheet?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies ExlService Holdings, Inc. (NASDAQ:EXLS) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for ExlService Holdings

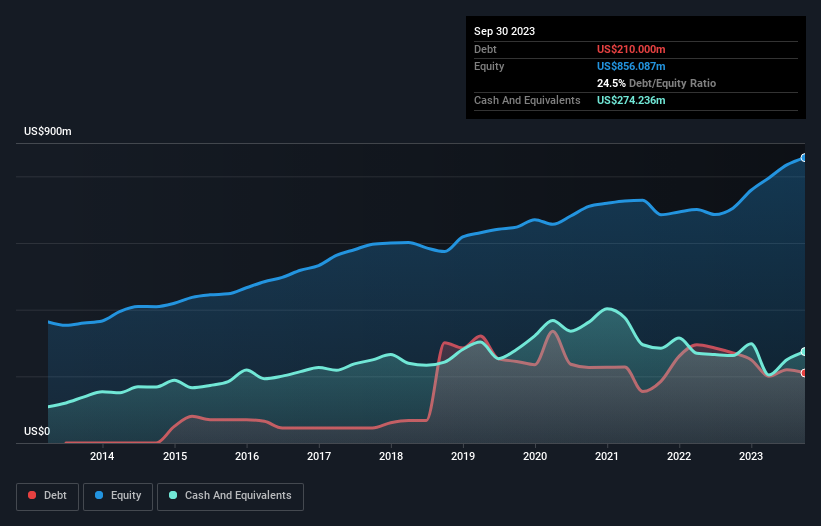

How Much Debt Does ExlService Holdings Carry?

As you can see below, ExlService Holdings had US$210.0m of debt at September 2023, down from US$270.0m a year prior. But it also has US$274.2m in cash to offset that, meaning it has US$64.2m net cash.

How Healthy Is ExlService Holdings' Balance Sheet?

According to the last reported balance sheet, ExlService Holdings had liabilities of US$306.1m due within 12 months, and liabilities of US$240.3m due beyond 12 months. On the other hand, it had cash of US$274.2m and US$321.7m worth of receivables due within a year. So it can boast US$49.5m more liquid assets than total liabilities.

Having regard to ExlService Holdings' size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the US$4.89b company is struggling for cash, we still think it's worth monitoring its balance sheet. Succinctly put, ExlService Holdings boasts net cash, so it's fair to say it does not have a heavy debt load!

In addition to that, we're happy to report that ExlService Holdings has boosted its EBIT by 33%, thus reducing the spectre of future debt repayments. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine ExlService Holdings's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While ExlService Holdings has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last three years, ExlService Holdings produced sturdy free cash flow equating to 75% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Summing Up

While it is always sensible to investigate a company's debt, in this case ExlService Holdings has US$64.2m in net cash and a decent-looking balance sheet. And we liked the look of last year's 33% year-on-year EBIT growth. So is ExlService Holdings's debt a risk? It doesn't seem so to us. We'd be very excited to see if ExlService Holdings insiders have been snapping up shares. If you are too, then click on this link right now to take a (free) peek at our list of reported insider transactions.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if ExlService Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:EXLS

ExlService Holdings

Operates as a data analytics, and digital operations and solutions company in the United States and internationally.

Excellent balance sheet with reasonable growth potential.