Advertisement

- United States

- /

- Professional Services

- /

- NasdaqGS:CRAI

What CRA International (CRAI)'s Analyst Upgrades and Raised Earnings Forecasts Mean for Shareholders

Simply Wall St

Reviewed by Sasha Jovanovic

- CRA International recently received an upgrade to a Zacks Rank #2 (Buy) as analysts raised earnings estimates, reflecting increased optimism about the consulting firm's financial outlook.

- Notably, multiple analysts revised earnings estimates higher for fiscal 2025, highlighting broadening positive sentiment that could raise the company's profile among institutional investors.

- We'll explore how this improved analyst sentiment could influence CRA International's investment narrative and longer-term positioning.

Find companies with promising cash flow potential yet trading below their fair value.

CRA International Investment Narrative Recap

To be a CRA International shareholder, it’s important to believe in the continued demand for high-value consulting driven by global regulatory complexity and strong M&A activity. The recent upgrade to a Zacks Rank #2 (Buy) and earnings estimate revisions point to improved sentiment, which could act as a short-term catalyst, potentially supporting stock performance if analyst optimism proves justified. However, none of these developments directly address the company’s exposure to cyclical shifts in dealmaking or the risk of revenue volatility during slower corporate activity periods.

Among recent announcements, CRA International’s raised revenue guidance for fiscal 2025 to US$730 million to US$745 million stands out, indicating strong visibility into near-term demand. While this aligns with the catalyst of heightened global deal activity, it does not reduce sensitivity to sector slowdowns or risks tied to talent retention, which may increase long-term earnings volatility.

In contrast, investors should be aware that the company’s concentrated exposure to antitrust and litigation support could mean...

Read the full narrative on CRA International (it's free!)

CRA International's outlook anticipates revenues of $822.0 million and earnings of $60.0 million by 2028. This is based on analysts' expectations for a 4.9% annual revenue growth rate and a $3.6 million increase in earnings from the current $56.4 million.

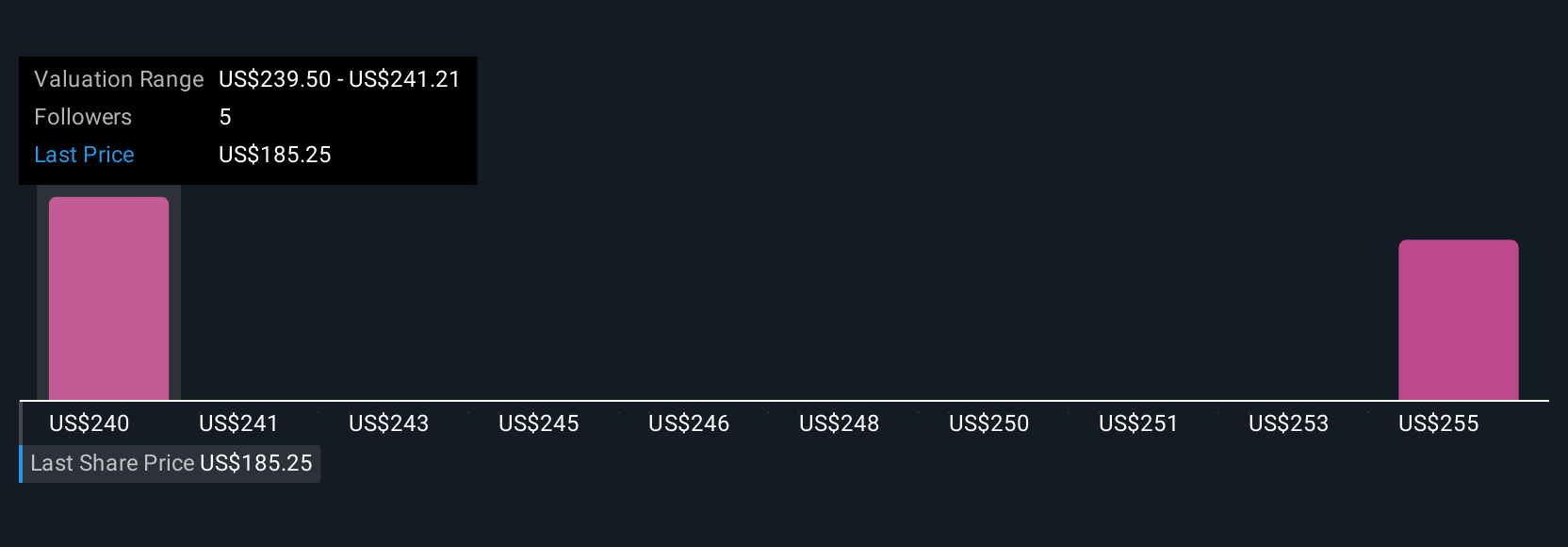

Uncover how CRA International's forecasts yield a $239.50 fair value, a 22% upside to its current price.

Exploring Other Perspectives

Two Simply Wall St Community members estimated CRA International’s fair value from US$239.50 to US$256.78 per share. While estimates vary, many remain focused on robust demand from global regulatory and M&A trends, inviting you to weigh different interpretations on what could drive future results.

Explore 2 other fair value estimates on CRA International - why the stock might be worth just $239.50!

Build Your Own CRA International Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your CRA International research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free CRA International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CRA International's overall financial health at a glance.

Interested In Other Possibilities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 33 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CRAI

CRA International

Provides economic, financial, and management consulting services worldwide.

Outstanding track record and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|30.4% undervalued

MA

Community Contributor

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.0% undervalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|20.4% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor