- United States

- /

- Electrical

- /

- NYSE:ROK

Rockwell Automation (NYSE:ROK) Powers Finland's Hydroelectric AI Transformation With Cutting-Edge Control Tech

Reviewed by Simply Wall St

In recent developments, Rockwell Automation (NYSE:ROK) announced an innovative industrial computing technology that enhances water-turbine control at PVO-Vesivoima's plants, leading to improved efficiency and compliance with stringent Finnish regulations. This announcement, coupled with the launch of new products and a revised earnings guidance, may have added positive momentum to the company's noteworthy 32% share price increase over the past month. The broader market environment, which has seen a 5% increase, provided a supportive backdrop. Despite a decline in revenue and net income, the share buyback program and new product initiatives likely bolstered investor confidence.

We've spotted 1 possible red flag for Rockwell Automation you should be aware of.

Outshine the giants: these 29 early-stage AI stocks could fund your retirement.

The recent technological advances by Rockwell Automation, especially the improved industrial computing technology for water-turbine controls, align well with its narrative of enhancing resilience and operational effectiveness. Such innovations can boost revenue growth, especially in the Software & Control segment, accelerating market opportunities. Over the past three years, Rockwell Automation's total shareholder return, including share price and dividends, was 65.34%, reflecting solid investor sentiment despite revenue and net income declines.

In contrast to a more recent period, where its share price increased 32% in one month, this three-year performance offers a broader perspective on its sustained growth. Within the past year, Rockwell faced challenges, underperforming the US Electrical industry, which returned 15.3%. This divergence emphasizes the importance of continuing to address operational and market challenges.

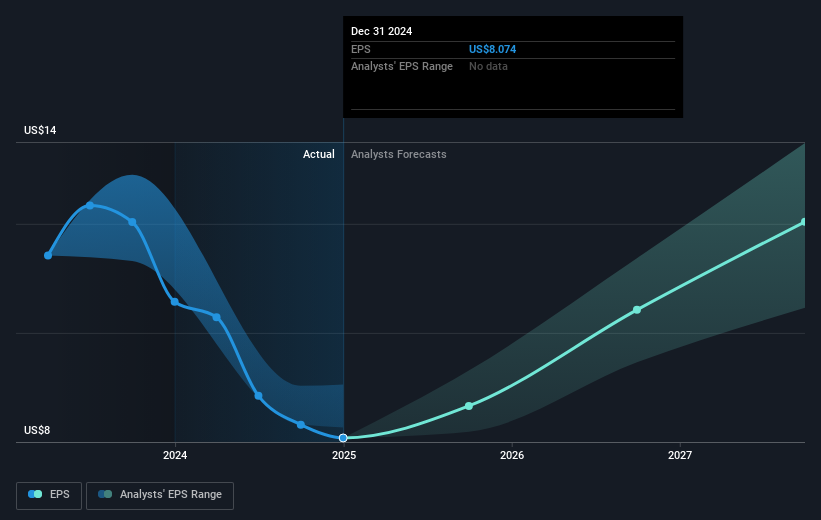

The new advancements could positively impact future revenue and earnings forecasts, aligning with analyst expectations of revenue reaching US$9.4 billion and earnings of US$1.4 billion by 2028. While the share price currently sits at US$253.05, it is approaching analyst consensus price targets of US$278.97, suggesting potential but moderated growth expectations. This context underscores the nuanced task Rockwell faces in satisfying market expectations amid industry shifts and macroeconomic uncertainties.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ROK

Rockwell Automation

Provides industrial automation and digital transformation solutions in North America, Europe, the Middle East, Africa, the Asia Pacific, and Latin America.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Community Narratives