- United States

- /

- Machinery

- /

- NYSE:PLOW

Douglas Dynamics (NYSE:PLOW) Achieves Turnaround With Improved Earnings

Reviewed by Simply Wall St

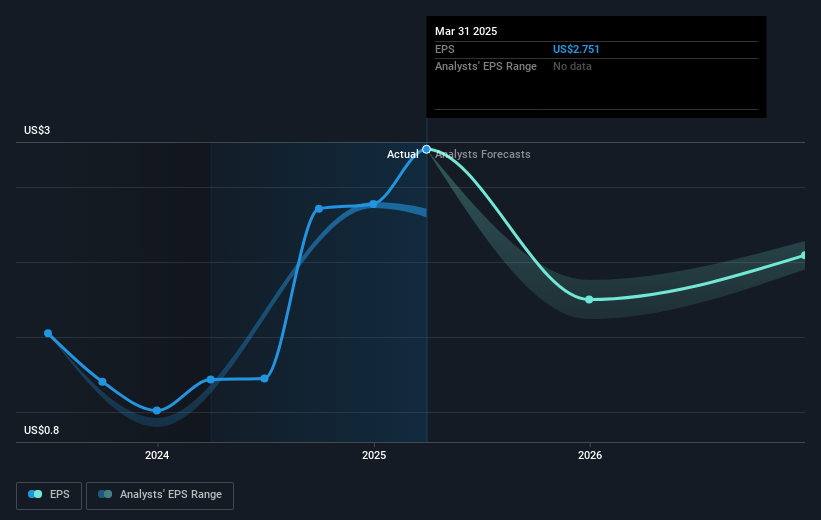

Douglas Dynamics (NYSE:PLOW) experienced a significant share price increase of 25% over the past month. This notable movement aligns with the company's recent developments, including its release of improved quarterly earnings and optimistic full-year 2025 sales guidance. The turnaround from a net loss in the prior year to a modest net income reflects strong operational improvements. Additionally, the leadership transition with Don Sturdivant's appointment as Chairman may have played a role in investor confidence. Despite broader market gains, these specific company achievements likely added substantial weight to Douglas Dynamics's recent upward trajectory.

Douglas Dynamics's recent substantial share price increase of 25% highlights the market's positive reaction to the company's improved quarterly earnings and optimistic guidance for 2025. This momentum, supported by the shift from a net loss to a modest net income and the leadership transition with Don Sturdivant as Chairman, could bolster the company's narrative of growth and operational improvements. The ongoing enhancements in its municipal solutions could pave the way for stable revenue, while strategizing around its attachments segment could yield better profitability as demand fluctuates.

Over the last year, Douglas Dynamics achieved a total return of 18.84%, outperforming the US Machinery industry, which posted a 1.6% return. This robust performance underscores the company's ability to leverage market conditions effectively. While analysts anticipate an earnings decline of 11.4% annually over the next three years to reach US$47.4 million by 2028, the recent price jump suggests confidence in future growth, possibly influenced by the strong backlog in its municipal contracts.

The current share price of US$24.04, while boosted from recent developments, still trades at a 14.5% discount to the consensus price target of US$33.67. This target reflects expectations of a future PE ratio of 20.5x on 2028 earnings, compared to today's 10.1x. The company's focus on leveraging its strong balance sheet for acquisitions and operational leadership has the potential to impact revenue and earnings forecasts positively. As investors weigh these factors, the evolution of Douglas Dynamics's market positioning and future earnings growth remains a focal point for future assessments.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PLOW

Douglas Dynamics

Operates as a manufacturer and upfitter of commercial work truck attachments and equipment in North America.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Salesforce Stock: AI-Fueled Growth Is Real — But Can Margins Stay This Strong?

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)