- United States

- /

- Electrical

- /

- NYSE:NRGV

News Flash: 6 Analysts Think Energy Vault Holdings, Inc. (NYSE:NRGV) Earnings Are Under Threat

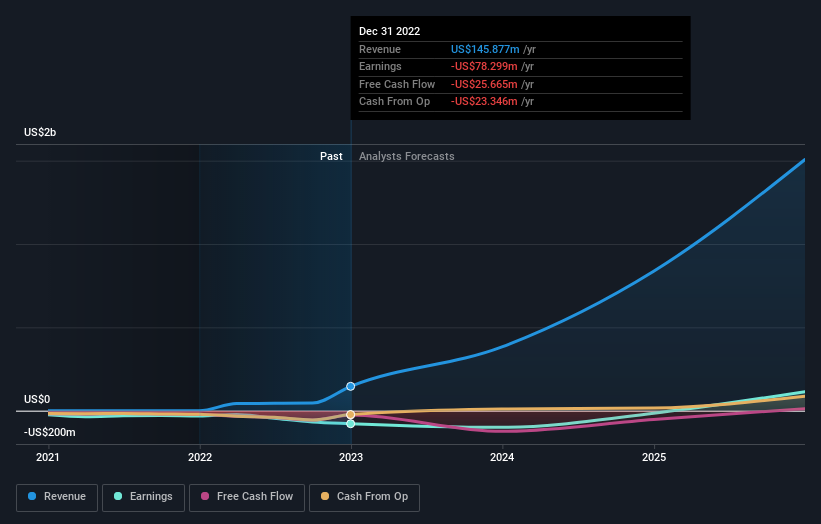

The analysts covering Energy Vault Holdings, Inc. (NYSE:NRGV) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for this year. Both revenue and earnings per share (EPS) estimates were cut sharply as analysts factored in the latest outlook for the business, concluding that they were too optimistic previously.

Following the downgrade, the current consensus from Energy Vault Holdings' six analysts is for revenues of US$383m in 2023 which - if met - would reflect a huge 162% increase on its sales over the past 12 months. The loss per share is expected to ameliorate slightly, reducing to US$0.55. Yet prior to the latest estimates, the analysts had been forecasting revenues of US$548m and losses of US$0.45 per share in 2023. So there's been quite a change-up of views after the recent consensus updates, with the analysts making a serious cut to their revenue forecasts while also expecting losses per share to increase.

View our latest analysis for Energy Vault Holdings

The consensus price target fell 24% to US$6.80, with the analysts clearly concerned about the company following the weaker revenue and earnings outlook. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. The most optimistic Energy Vault Holdings analyst has a price target of US$12.00 per share, while the most pessimistic values it at US$2.50. So we wouldn't be assigning too much credibility to analyst price targets in this case, because there are clearly some widely differing views on what kind of performance this business can generate. With this in mind, we wouldn't rely too heavily on the consensus price target, as it is just an average and analysts clearly have some deeply divergent views on the business.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. The analysts are definitely expecting Energy Vault Holdings' growth to accelerate, with the forecast 162% annualised growth to the end of 2023 ranking favourably alongside historical growth of 131% per annum over the past three years. Compare this with other companies in the same industry, which are forecast to grow their revenue 8.9% annually. Factoring in the forecast acceleration in revenue, it's pretty clear that Energy Vault Holdings is expected to grow much faster than its industry.

The Bottom Line

The most important thing to note from this downgrade is that the consensus increased its forecast losses this year, suggesting all may not be well at Energy Vault Holdings. Unfortunately, analysts also downgraded their revenue estimates, although our data indicates revenues are expected to perform better than the wider market. Given the scope of the downgrades, it would not be a surprise to see the market become more wary of the business.

That said, the analysts might have good reason to be negative on Energy Vault Holdings, given dilutive stock issuance over the past year. For more information, you can click here to discover this and the 1 other risk we've identified.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you're looking to trade Energy Vault Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Energy Vault Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:NRGV

Adequate balance sheet low.