- United States

- /

- Commercial Services

- /

- NasdaqGS:TILE

Interface Leads These 3 Undiscovered Gems with Promising Potential

Reviewed by Simply Wall St

The United States market has shown robust performance, climbing 2.2% over the last week and an impressive 33% over the past year, with earnings projected to grow by 15% annually in the coming years. In this thriving environment, identifying stocks with strong fundamentals and growth potential can be key to uncovering hidden opportunities like Interface and other promising contenders.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Eagle Financial Services | 170.75% | 12.30% | 1.92% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Franklin Financial Services | 173.21% | 5.55% | -1.86% | ★★★★★★ |

| Parker Drilling | 46.25% | -0.33% | 53.04% | ★★★★★★ |

| Omega Flex | NA | 0.39% | 2.57% | ★★★★★★ |

| First Northern Community Bancorp | NA | 7.65% | 11.17% | ★★★★★★ |

| Teekay | NA | -3.71% | 60.91% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 7.11% | -35.88% | ★★★★★☆ |

| Pure Cycle | 5.31% | -4.44% | -5.74% | ★★★★★☆ |

| FRMO | 0.13% | 19.43% | 29.70% | ★★★★☆☆ |

We'll examine a selection from our screener results.

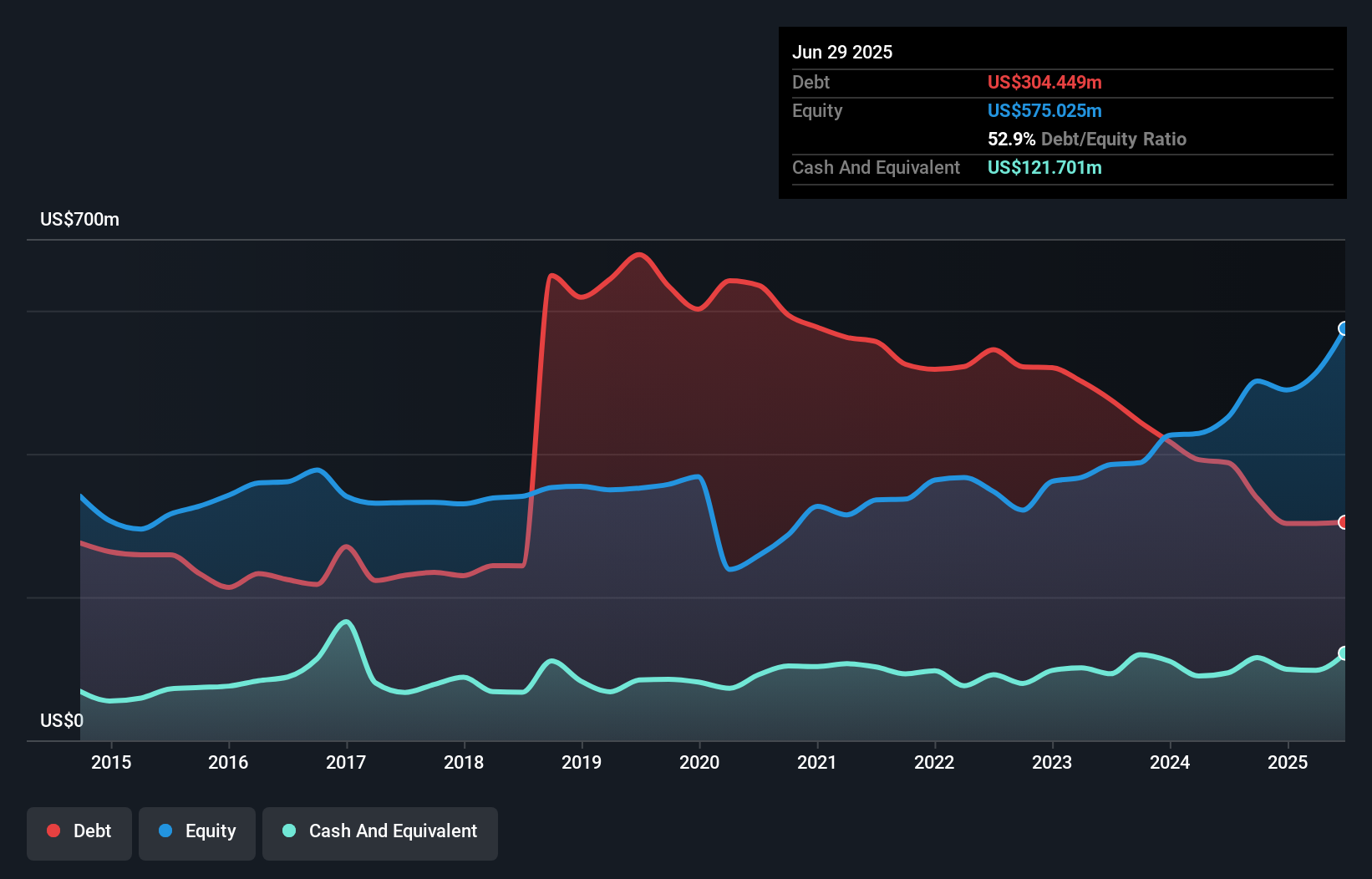

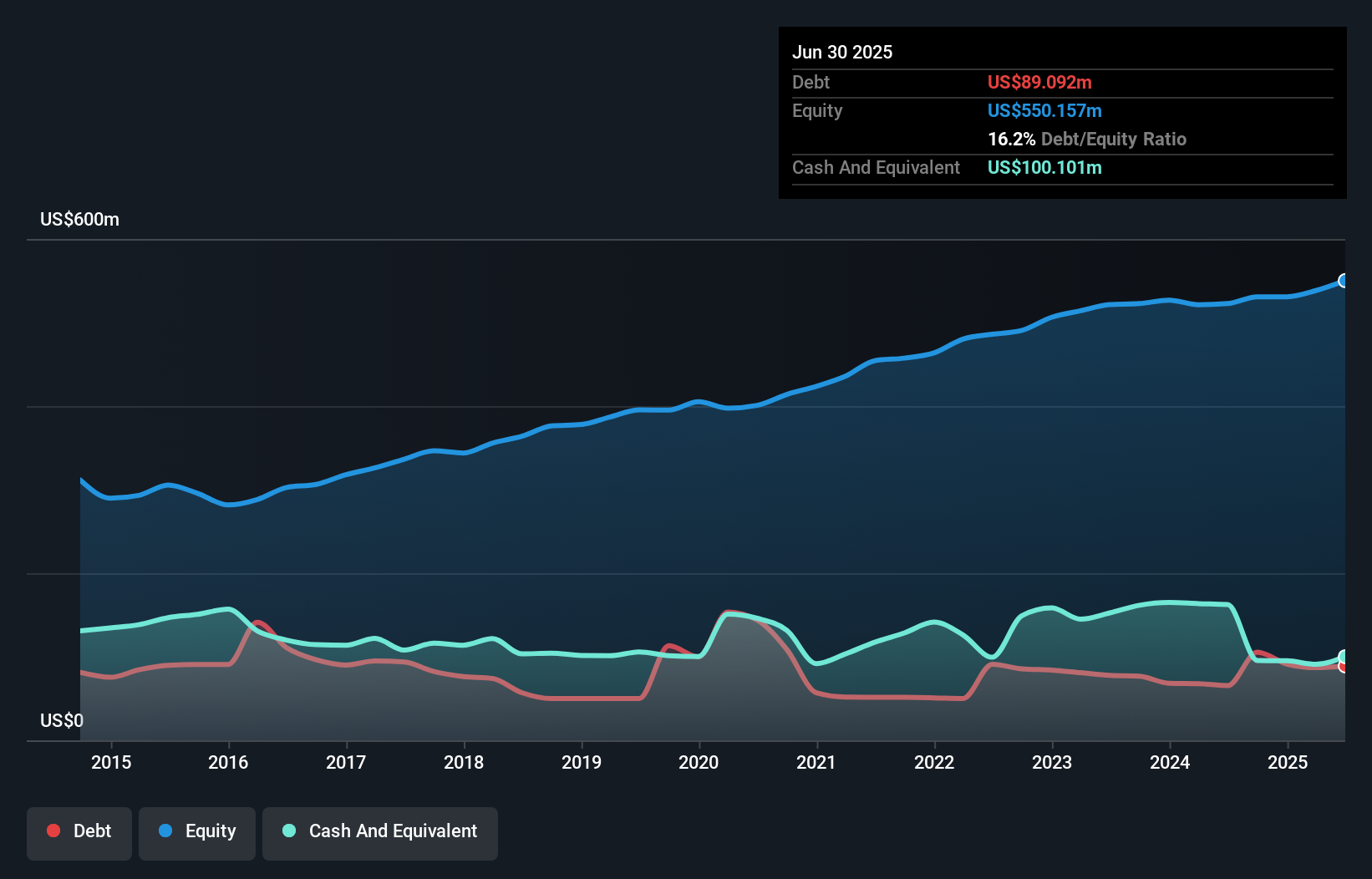

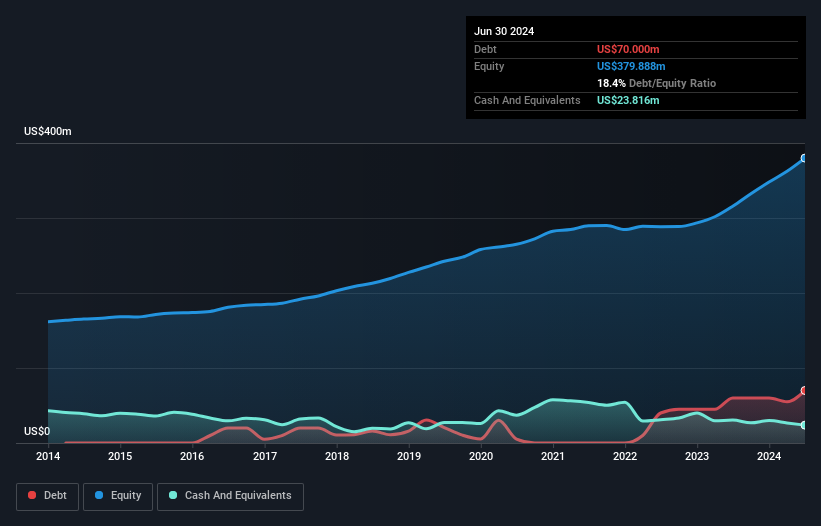

Interface (NasdaqGS:TILE)

Simply Wall St Value Rating: ★★★★★☆

Overview: Interface, Inc. designs, produces, and sells modular carpet products primarily worldwide with a market cap of $1.48 billion.

Operations: Interface generates revenue primarily from its Americas segment, contributing $783.32 million, and the Europe, Africa, Asia, and Australia segment with $522.45 million.

Interface has been making waves with its impressive earnings growth of 10,169% over the past year, significantly outpacing the industry average. The company’s net debt to equity ratio stands at 44.3%, which is considered high but has improved from 177.4% five years ago to 67.4%. Interface's recent product launches, including the norament 926 satura collection and new carpet tile lines like Etched Earth™, highlight its commitment to sustainability and innovation, enhancing its market position in high-traffic areas such as healthcare and education sectors. Despite these strengths, significant insider selling in recent months suggests caution may be warranted for potential investors considering this stock as a viable option within their portfolios.

CTS (NYSE:CTS)

Simply Wall St Value Rating: ★★★★★★

Overview: CTS Corporation manufactures and sells sensors, actuators, and connectivity components across North America, Europe, and Asia with a market capitalization of approximately $1.63 billion.

Operations: CTS generates revenue primarily from its Electronic Components & Parts segment, amounting to $513.03 million.

CTS Corporation, a small player in the electronics industry, is navigating a mixed landscape. Despite negative earnings growth of -0.5% over the past year, its net income rose to US$18.68 million from US$13.97 million year-over-year for Q3 2024, reflecting robust operational improvements and high-quality earnings. The company has successfully diversified with over 52% of revenue now coming from varied markets like aerospace, which may stabilize future profits despite challenges in transportation and medical sectors. With a satisfactory net debt to equity ratio of 1.9%, CTS seems well-positioned financially but faces execution risks that could affect projected growth targets.

Miller Industries (NYSE:MLR)

Simply Wall St Value Rating: ★★★★★☆

Overview: Miller Industries, Inc. manufactures and sells towing and recovery equipment, with a market cap of $822.83 million.

Operations: Miller Industries generates revenue primarily from its auto manufacturers segment, which totaled $1.33 billion. The company's financial performance is highlighted by a notable trend in its net profit margin.

Miller Industries, a dynamic player in the machinery sector, is making waves with its strategic focus on international and military markets. The company reported third-quarter sales of US$314 million, up from US$275 million last year, though net income dipped to US$15 million from US$17 million. Its earnings per share for nine months rose to US$4.62 from US$3.64 previously. Despite challenges like rising costs and market dependency, Miller's robust EBIT coverage of 18.6 times interest payments and satisfactory net debt to equity ratio at 6% underscore financial health amidst growth prospects projected at 8% annually.

Where To Now?

- Unlock our comprehensive list of 229 US Undiscovered Gems With Strong Fundamentals by clicking here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TILE

Interface

Designs, produces, and sells modular carpet products primarily worldwide.

Solid track record with excellent balance sheet.