Advertisement

- United States

- /

- Aerospace & Defense

- /

- NYSE:LMT

How Investors May Respond To Lockheed Martin (LMT) Analyst Upgrades and Record Backlog Momentum

Simply Wall St

Reviewed by Sasha Jovanovic

- In recent days, Lockheed Martin has received analyst upgrades and renewed coverage driven by robust international order backlogs, new production capacity, and major contract wins, with its dominant role in the F-35 program highlighted.

- Lockheed Martin's expanded dividends and buyback authorization signal increased confidence in ongoing shareholder returns amid resurging demand and geopolitical catalysts.

- Next, we'll examine how Lockheed Martin's record backlog and improved execution affect the company's forward-looking investment narrative.

Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Lockheed Martin Investment Narrative Recap

To be a shareholder in Lockheed Martin, you need to believe that advanced military platforms, global defense demand, and a record US$179 billion backlog can drive future growth, even as government budgets shift. The latest analyst upgrades and contract wins further reinforce the importance of international orders as the most important short-term catalyst, but ongoing regulatory and legal headwinds, like the US$4.6 billion IRS tax dispute, remain the largest risk, and the recent news does not materially change this outlook.

Among the recent announcements, Lockheed Martin’s increase in its quarterly dividend by 5%, marking 23 consecutive years of growth, stands out and is relevant in the context of strengthening short-term demand and analyst optimism. This move, combined with a US$2 billion boost to its buyback authorization, is a visible signal of management’s prioritization of shareholder returns as backlog and order visibility increase.

In contrast, investors should be aware that even with strong new orders, unresolved regulatory risks including the company’s ongoing tax dispute with the IRS could…

Read the full narrative on Lockheed Martin (it's free!)

Lockheed Martin's outlook anticipates $81.0 billion in revenue and $7.1 billion in earnings by 2028. This scenario assumes 4.1% annual revenue growth and a $2.9 billion increase in earnings from today's $4.2 billion level.

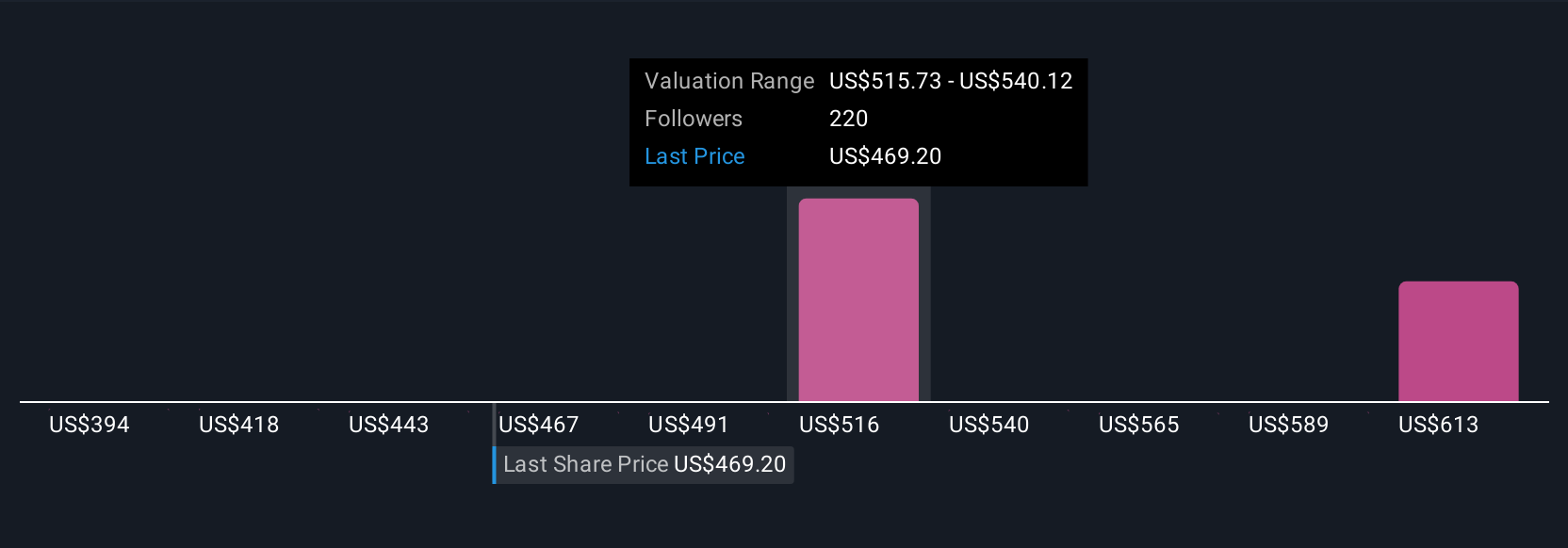

Uncover how Lockheed Martin's forecasts yield a $528.17 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Twenty-five members of the Simply Wall St Community have estimated Lockheed Martin’s fair value between US$389 and US$629 per share. While many see potential given the current backlog and technology leadership, others weigh ongoing legal and margin risks that may affect future performance, explore these diverse opinions to inform your own view.

Explore 25 other fair value estimates on Lockheed Martin - why the stock might be worth 15% less than the current price!

Build Your Own Lockheed Martin Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Lockheed Martin research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Lockheed Martin research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Lockheed Martin's overall financial health at a glance.

Curious About Other Options?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 35 companies in the world exploring or producing it. Find the list for free.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:LMT

Lockheed Martin

An aerospace and defense company, engages in the research, design, development, manufacture, integration, and sustainment of technology systems, products, and services worldwide.

Undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

10 followersusers have followed this narrative

5 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

YE

Yellow_fever on China Starch Holdings ·

China Starch Holdings eyes a revenue growth of 4.66% with a 5-year strategic plan

Fair Value:HK$0.562.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Power Solutions International ·

PSIX The timing of insider sales is a serious question mark

Fair Value:US$37.3845.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Marvell Technology ·

The Great Strategy Swap – Selling "Old Auto" to Buy "Future Light"

Fair Value:US$155.3740.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.6% undervalued

946 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.2% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative