- United States

- /

- Aerospace & Defense

- /

- NYSE:LHX

L3Harris Technologies (LHX) Reports Increased Q2 Earnings With US$458 Million Net Income

Reviewed by Simply Wall St

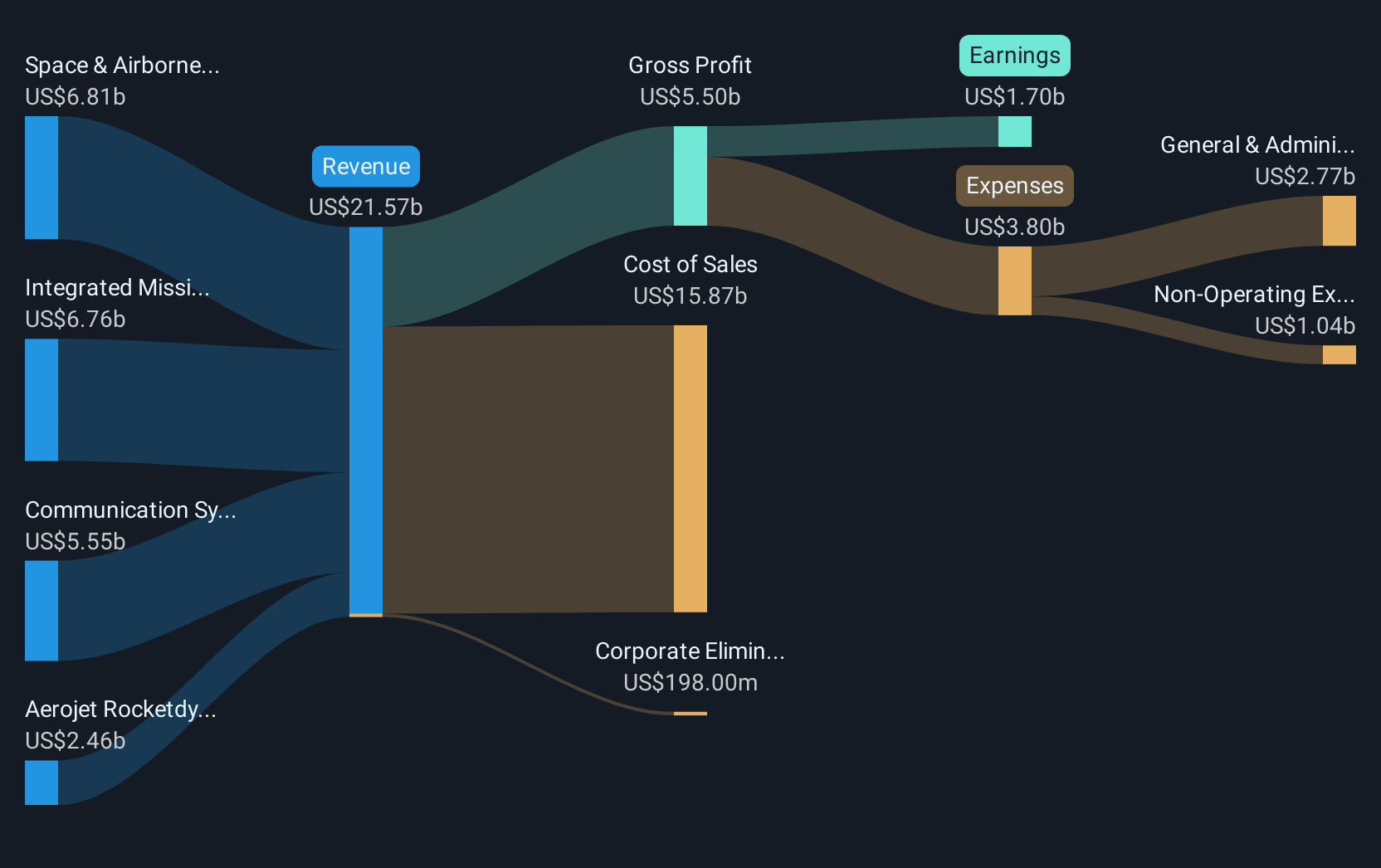

L3Harris Technologies (LHX) recently announced robust financial results for the second quarter of 2025, reporting strong growth in sales and net income, which likely influenced its stock performance. The company also affirmed a quarterly dividend, and launched new products that span electronic warfare and kinetic platforms, enhancing its position in the defense sector. Additionally, its plans for a substantial expansion of manufacturing capabilities reflect commitment to future growth. During the quarter, LHX shares rose 25%, while the broader market increased 18%. The company's performance likely aligned with prevalent market trends, bolstering investor confidence and contributing to its impressive stock performance.

We've discovered 1 risk for L3Harris Technologies that you should be aware of before investing here.

The recent strong performance of L3Harris Technologies' stock, rising 25% during the quarter, highlights investor optimism following robust sales growth and product launches. This momentum is supported by solid financial results for the second quarter of 2025, which could enhance the company's revenue and earnings prospects. With an ongoing commitment to expansion, the news is likely to bolster future revenue streams, particularly within the defense sector.

Over a five-year period, the company's total shareholder return, which includes share price appreciation and dividends, reached 72.62%. Despite underperforming the US Aerospace & Defense industry over the past year, the company's recent quarterly growth suggests a potential rebound. However, in the last year, the stock underperformed both the US market's 17.7% and industry’s 41.7% gains.

The forecasted revenue growth of 4.4% annually over the next three years aligns with strategic initiatives like LHX NeXt and international demand. These, alongside potential earnings reaching US$2.5 billion by 2028, underpin a positive growth outlook. The share price's proximity to the analyst price target of US$273.22 suggests limited upside potential in the short term, reflecting the market's perception of it being fairly priced at current levels.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:LHX

L3Harris Technologies

Provides mission-critical solutions for government and commercial customers worldwide.

Established dividend payer with proven track record.

Similar Companies

Market Insights

Community Narratives