Advertisement

- United States

- /

- Construction

- /

- NYSE:GVA

Are Robust Financials Driving The Recent Rally In Granite Construction Incorporated's (NYSE:GVA) Stock?

Granite Construction (NYSE:GVA) has had a great run on the share market with its stock up by a significant 13% over the last month. Since the market usually pay for a company’s long-term fundamentals, we decided to study the company’s key performance indicators to see if they could be influencing the market. Particularly, we will be paying attention to Granite Construction's ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

We've discovered 1 warning sign about Granite Construction. View them for free.How To Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Granite Construction is:

14% = US$142m ÷ US$1.0b (Based on the trailing twelve months to March 2025).

The 'return' is the yearly profit. So, this means that for every $1 of its shareholder's investments, the company generates a profit of $0.14.

See our latest analysis for Granite Construction

What Has ROE Got To Do With Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

Granite Construction's Earnings Growth And 14% ROE

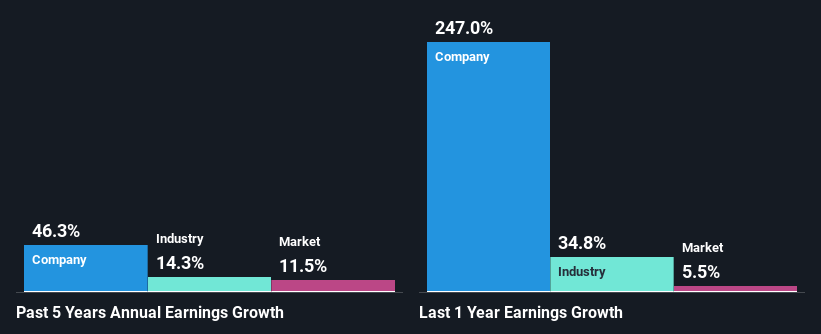

To begin with, Granite Construction seems to have a respectable ROE. Further, the company's ROE is similar to the industry average of 14%. This probably goes some way in explaining Granite Construction's significant 46% net income growth over the past five years amongst other factors. We reckon that there could also be other factors at play here. For instance, the company has a low payout ratio or is being managed efficiently.

As a next step, we compared Granite Construction's net income growth with the industry, and pleasingly, we found that the growth seen by the company is higher than the average industry growth of 14%.

Earnings growth is an important metric to consider when valuing a stock. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. Doing so will help them establish if the stock's future looks promising or ominous. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Granite Construction is trading on a high P/E or a low P/E, relative to its industry.

Is Granite Construction Making Efficient Use Of Its Profits?

The three-year median payout ratio for Granite Construction is 44%, which is moderately low. The company is retaining the remaining 56%. By the looks of it, the dividend is well covered and Granite Construction is reinvesting its profits efficiently as evidenced by its exceptional growth which we discussed above.

Moreover, Granite Construction is determined to keep sharing its profits with shareholders which we infer from its long history of paying a dividend for at least ten years.

Conclusion

Overall, we are quite pleased with Granite Construction's performance. In particular, it's great to see that the company is investing heavily into its business and along with a high rate of return, that has resulted in a sizeable growth in its earnings. We also studied the latest analyst forecasts and found that the company's earnings growth is expected be similar to its current growth rate. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:GVA

Granite Construction

Operates as an infrastructure contractor in the United States.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor