- United States

- /

- Building

- /

- NYSE:GFF

Griffon (GFF): Revisiting Valuation After Strong Recent Share Price Momentum

Reviewed by Simply Wall St

Griffon (GFF) has quietly outperformed the broader market over the past week and month, and that steady climb is starting to draw attention from investors looking for durable industrial exposure.

See our latest analysis for Griffon.

The recent 1 month share price return of 7.88 percent, on top of a robust 3 year total shareholder return of 144.18 percent, suggests momentum is still firmly on Griffon’s side as investors reassess its growth and cash generation story.

If Griffon’s run has you thinking more broadly about where capital could compound next, now is a good time to explore fast growing stocks with high insider ownership.

With Griffon still trading at a sizeable discount to analyst targets despite strong multi year returns, investors face a key question: is this an underappreciated compounder, or is the market already baking in the next leg of growth?

Most Popular Narrative: 24.9% Undervalued

Compared to Griffon’s last close at $77.23, the most followed narrative pegs fair value materially higher, framing the current discount as a forward looking opportunity.

The analysts have a consensus price target of $100.286 for Griffon based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $115.0, and the most bearish reporting a price target of just $90.0.

Want to see what kind of profit margin reset, earnings ramp, and future multiple could justify that higher value, all discounted at a single, precise rate? Dive in and unpack the assumptions powering this fair value view.

Result: Fair Value of $102.83 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent weak consumer demand and elevated inventories, especially in Consumer and Professional Products, could pressure margins and interrupt the recent positive earnings trend.

Find out about the key risks to this Griffon narrative.

Another Lens on Value

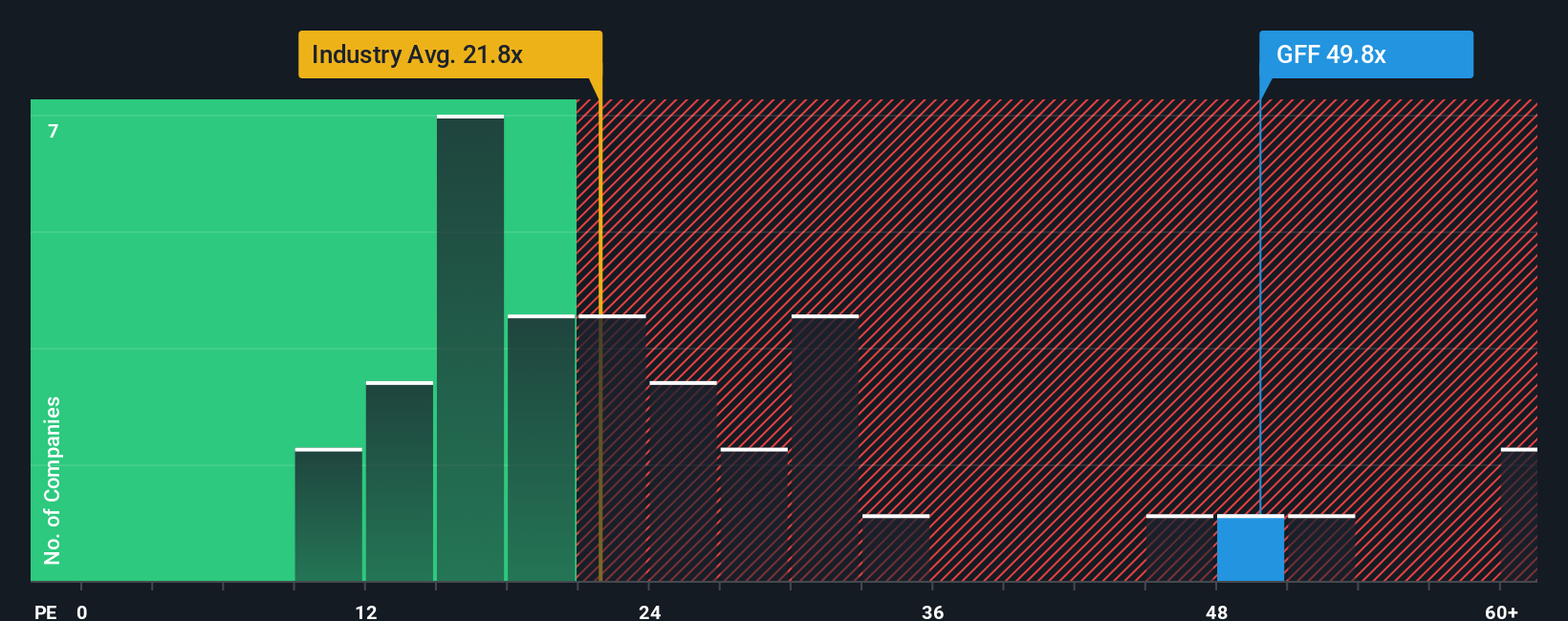

While analyst targets and narratives flag Griffon as 24.9 percent undervalued, our earnings based yardstick sends a very different signal. At 69.9 times earnings versus a US Building industry average of 19.8 times and a fair ratio of 36 times, the stock screens richly priced and raises the question of how much upside is already in the multiple.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Griffon Narrative

If you see the story differently or want to pressure test the numbers yourself, you can build a fresh narrative in minutes: Do it your way.

A great starting point for your Griffon research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Ready for more investment ideas?

Before you move on, consider your next potential opportunity by scanning focused stock shortlists built to uncover specific ideas that many investors might overlook.

- Explore potential multi baggers early by scanning these 3607 penny stocks with strong financials where solid fundamentals back up those small share prices.

- Consider companies involved in transformative innovation by reviewing these 25 AI penny stocks that are built around real revenue, scalable models and demand for intelligent solutions.

- Review these 12 dividend stocks with yields > 3% to find stocks that pair dividend income with balance sheets designed to support ongoing payouts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:GFF

Griffon

Through its subsidiaries, provides home and building, and consumer and professional products in the United States, Europe, Canada, Australia, and internationally.

Reasonable growth potential and fair value.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Trending Discussion