Advertisement

- United States

- /

- Construction

- /

- NYSE:FLR

Does Fluor’s (FLR) NuScale Share Sale Signal a Shift in Its Capital Allocation Priorities?

Simply Wall St

Reviewed by Sasha Jovanovic

- Fluor Corporation recently completed the sale of 15 million shares of NuScale Power Corporation and announced that most proceeds will go toward its ongoing share repurchase program.

- Despite selling a portion of its NuScale holdings, Fluor continues to hold 111 million Class B units and is actively seeking ways for shareholders to benefit more directly from this investment.

- We'll examine how Fluor’s focus on share repurchases following its NuScale share sale may alter its longer-term investment outlook.

The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Fluor Investment Narrative Recap

As a Fluor shareholder, you need to have confidence in the company’s ability to convert its significant backlog and client wins into steady cash flow, while managing exposure to project delays and cost overruns. The recent sale of 15 million NuScale shares, with proceeds directed toward further share repurchases, does not materially affect the chief near-term catalyst, Fluor’s focus on improving earnings through cash generation, or lessen the short-term risk stemming from unpredictability in project timing and collection of receivables.

One recent development especially connected to catalysts is Fluor’s continued execution of its share repurchase program; with over 4.7 million shares bought back in Q2 and the NuScale sale funding additional buybacks, there is clear emphasis on boosting EPS and delivering direct returns to shareholders. This approach fits alongside recent contract wins in core markets, supporting optimism that the company can achieve sustained improvements in margin and value creation for investors.

However, despite the progress on returning cash to shareholders, investors should keep in mind the contrast that Fluor is still contending with delays and increased costs on large projects, especially considering ...

Read the full narrative on Fluor (it's free!)

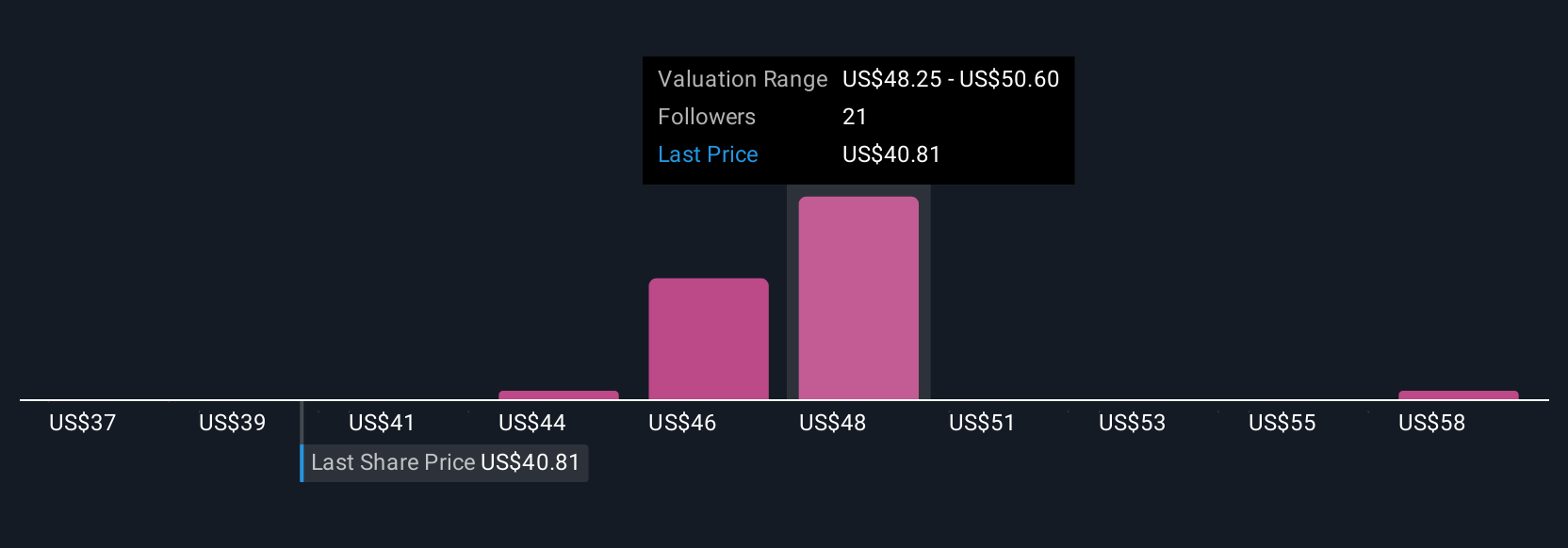

Fluor's narrative projects $19.6 billion in revenue and $511.6 million in earnings by 2028. This requires 6.2% yearly revenue growth and a $3.6 billion decrease in earnings from the current $4.1 billion.

Uncover how Fluor's forecasts yield a $49.89 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Six community members valued Fluor between US$45.61 and US$60, showing a wide span of fair value opinions. While Fluor emphasizes returns through cash flow and share buybacks, shifting project timelines continue to influence broader outlooks, see how these perspectives compare.

Explore 6 other fair value estimates on Fluor - why the stock might be worth just $45.61!

Build Your Own Fluor Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Fluor research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Fluor research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Fluor's overall financial health at a glance.

Seeking Other Investments?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 35 best rare earth metal stocks of the very few that mine this essential strategic resource.

- These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:FLR

Fluor

Provides engineering, procurement, and construction (EPC); fabrication and modularization; and project management services worldwide.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor