- United States

- /

- Commercial Services

- /

- NYSE:BV

Undervalued Small Caps With Insider Action In April 2025

Reviewed by Simply Wall St

In April 2025, the U.S. stock market is experiencing heightened volatility, with recent tariff announcements by President Trump causing significant fluctuations across major indices. The S&P 600, a key benchmark for small-cap stocks, has been particularly sensitive to these developments as investors assess the potential economic impact of trade policies on smaller companies. In such an environment, identifying promising small-cap stocks requires careful consideration of factors like financial health and strategic positioning within their industries.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Shore Bancshares | 10.4x | 2.3x | 8.42% | ★★★★☆☆ |

| First United | 9.5x | 2.5x | 48.22% | ★★★★☆☆ |

| MVB Financial | 11.1x | 1.5x | 29.06% | ★★★★☆☆ |

| S&T Bancorp | 10.9x | 3.7x | 42.17% | ★★★★☆☆ |

| West Bancorporation | 13.8x | 4.2x | 44.47% | ★★★☆☆☆ |

| Franklin Financial Services | 14.2x | 2.3x | 32.91% | ★★★☆☆☆ |

| Union Bankshares | 15.6x | 2.9x | 40.59% | ★★★☆☆☆ |

| Thryv Holdings | NA | 0.7x | 19.64% | ★★★☆☆☆ |

| Delek US Holdings | NA | 0.1x | -248.52% | ★★★☆☆☆ |

| Titan Machinery | NA | 0.1x | -340.51% | ★★★☆☆☆ |

Let's explore several standout options from the results in the screener.

Petco Health and Wellness Company (NasdaqGS:WOOF)

Simply Wall St Value Rating: ★★★★★☆

Overview: Petco Health and Wellness Company operates as a retailer specializing in pet products and services, with a market capitalization of approximately $2.52 billion.

Operations: Petco Health and Wellness Company generates revenue primarily through its retail specialty segment, with recent figures showing $6.12 billion. The company's cost of goods sold (COGS) is significant, amounting to $3.79 billion, impacting its gross profit margin which has shown a declining trend to 38.00%. Operating expenses are substantial as well, reaching approximately $2.31 billion in the latest period analyzed. The net income margin has fluctuated over time and was recorded at -1.66% in the most recent data point available.

PE: -9.1x

Petco Health and Wellness Company, a smaller player in the U.S. market, recently reported a decrease in quarterly revenue to US$1.55 billion from US$1.67 billion year-over-year, yet narrowed its net loss significantly to US$13.84 million from US$22.58 million. Despite volatile share prices over the past three months, insider confidence was reflected through recent share purchases by executives in February 2025, suggesting potential optimism for future growth amidst ongoing financial restructuring efforts led by new CFO Sabrina Simmons and strategic leadership changes.

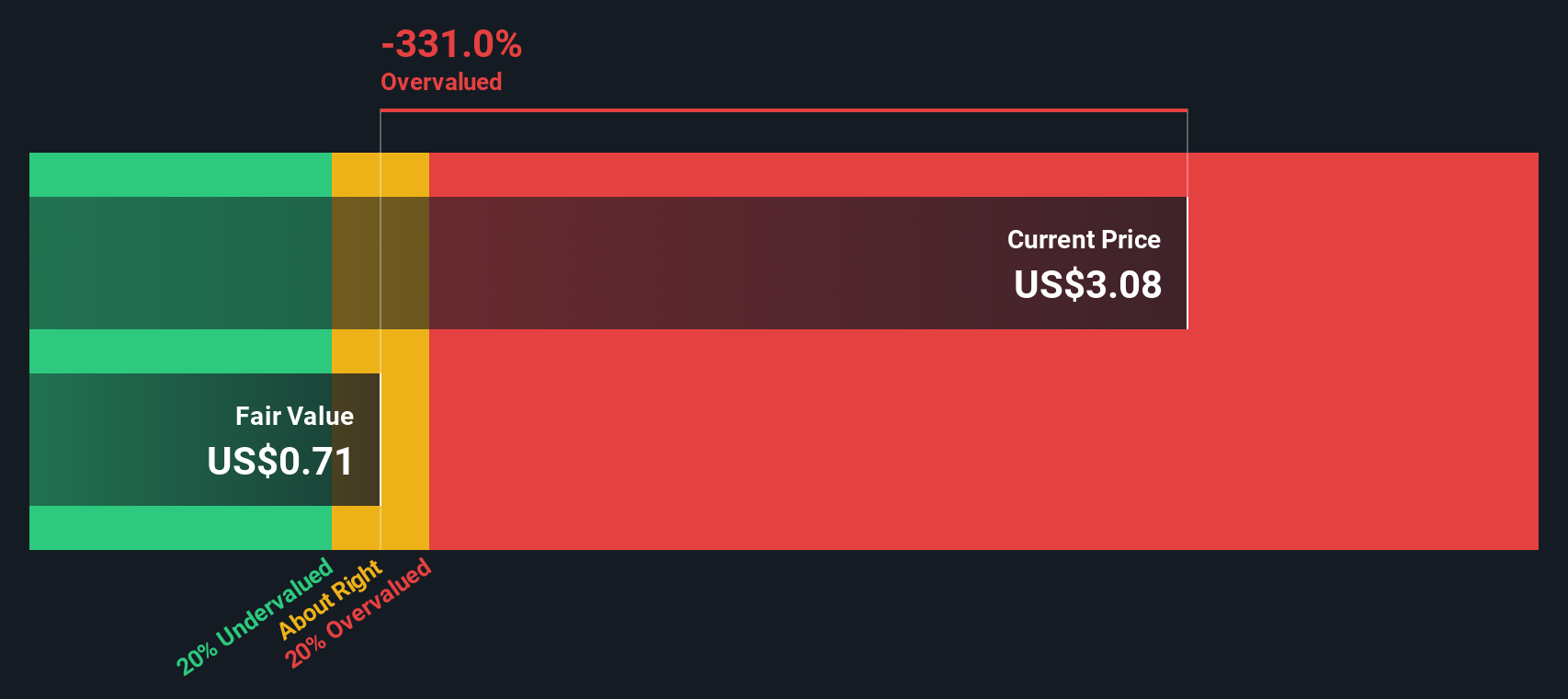

BrightView Holdings (NYSE:BV)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: BrightView Holdings operates as a commercial landscaping services provider, offering maintenance and development services, with a market capitalization of approximately $1.15 billion.

Operations: BrightView Holdings generates revenue primarily from Maintenance Services ($1.93 billion) and Development Services ($815.20 million). The company's cost of goods sold (COGS) consistently impacts its gross profit margin, which was 23.31% as of December 2024. Operating expenses, including significant general and administrative costs, further affect profitability.

PE: 50.1x

BrightView Holdings, a company with a focus on landscaping services, is navigating its financial landscape with strategic moves. Earnings are projected to grow by 60% annually, offering potential for future value. The company recently announced a US$100 million share repurchase program, demonstrating confidence in its stock's worth. Insider confidence is evident as Kurtis Barker acquired 40,000 shares valued at US$530,044 in March 2025. Despite reporting a net loss of US$10.4 million for Q1 2025, BrightView's proactive debt management and dividend payments indicate efforts to strengthen financial health and shareholder value.

- Click to explore a detailed breakdown of our findings in BrightView Holdings' valuation report.

Gain insights into BrightView Holdings' past trends and performance with our Past report.

Centuri Holdings (NYSE:CTRI)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Centuri Holdings operates in the utility infrastructure services sector, providing gas and electric solutions across the U.S. and Canada, with a market capitalization of approximately $2 billion.

Operations: Centuri Holdings generates revenue primarily from U.S. Gas, Canadian Gas, Union Electric, and Non-Union Electric segments. In recent periods, the company's gross profit margin has shown variability, with a notable figure of 10.98% in early 2021 decreasing to 8.37% by late 2024. Operating expenses have fluctuated but generally remained a significant portion of total costs alongside non-operating expenses impacting net income margins negatively in recent periods.

PE: -233.5x

Centuri Holdings, a smaller U.S. company, is capturing attention with its recent client announcements totaling over $850 million in new awards and renewals across diverse markets. Despite a net loss of US$6.72 million in 2024, significantly improved from the previous year's US$186.18 million loss, insider confidence remains high with notable share purchases throughout early 2025. The company's focus on expanding utility and energy infrastructure projects positions it for potential growth as earnings are projected to rise by over 90% annually.

- Click here to discover the nuances of Centuri Holdings with our detailed analytical valuation report.

Understand Centuri Holdings' track record by examining our Past report.

Make It Happen

- Explore the 93 names from our Undervalued US Small Caps With Insider Buying screener here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade BrightView Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if BrightView Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BV

BrightView Holdings

Through its subsidiaries, provides commercial landscaping services in the United States.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Community Narratives