Advertisement

- United States

- /

- Machinery

- /

- NYSE:CMI

Cummins (CMI) Is Up 5.4% After Widespread Analyst Upgrades Reflect Industry Confidence – Has the Bull Case Changed?

Simply Wall St

Reviewed by Sasha Jovanovic

- In late November 2025, Cummins saw a wave of analyst upgrades and improved ratings from major research firms, reflecting rising confidence in the company's outlook in heavy-duty engines and power solutions.

- This widespread analyst optimism highlights a shift in sentiment, suggesting growing expectations for Cummins' ability to adapt to industry changes and future demand drivers.

- To understand the impact of this increased analyst confidence, we'll explore how it informs Cummins' current investment narrative and long-term prospects.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Cummins Investment Narrative Recap

To be a Cummins shareholder today, you need to believe in the company’s ability to leverage its strength in heavy-duty engines and power solutions, while successfully expanding into cleaner energy markets amid significant industry transition. The recent surge in analyst upgrades and price targets reinforces optimism around Cummins’ positioning, but the immediate pressure from weaker North American truck demand remains the most important catalyst and risk. This wave of confidence does not materially shift that core dynamic in the short term.

One recent announcement that stands out is Cummins’ ongoing expansion in Power Systems, particularly to serve data center growth. This is significant as it underpins the company’s revenue diversification and supports the case for margin stability even as core trucking markets soften. Developments like these make the analyst upgrades more relevant to investors hoping for resilience during cyclical downturns.

However, against this backdrop of positive momentum, investors should still be mindful of the risk if sustained weakness in North American truck demand persists...

Read the full narrative on Cummins (it's free!)

Cummins' outlook anticipates $40.6 billion in revenue and $4.3 billion in earnings by 2028. This scenario requires a 6.4% annual revenue growth rate and a $1.4 billion increase in earnings from the current $2.9 billion level.

Uncover how Cummins' forecasts yield a $510.05 fair value, in line with its current price.

Exploring Other Perspectives

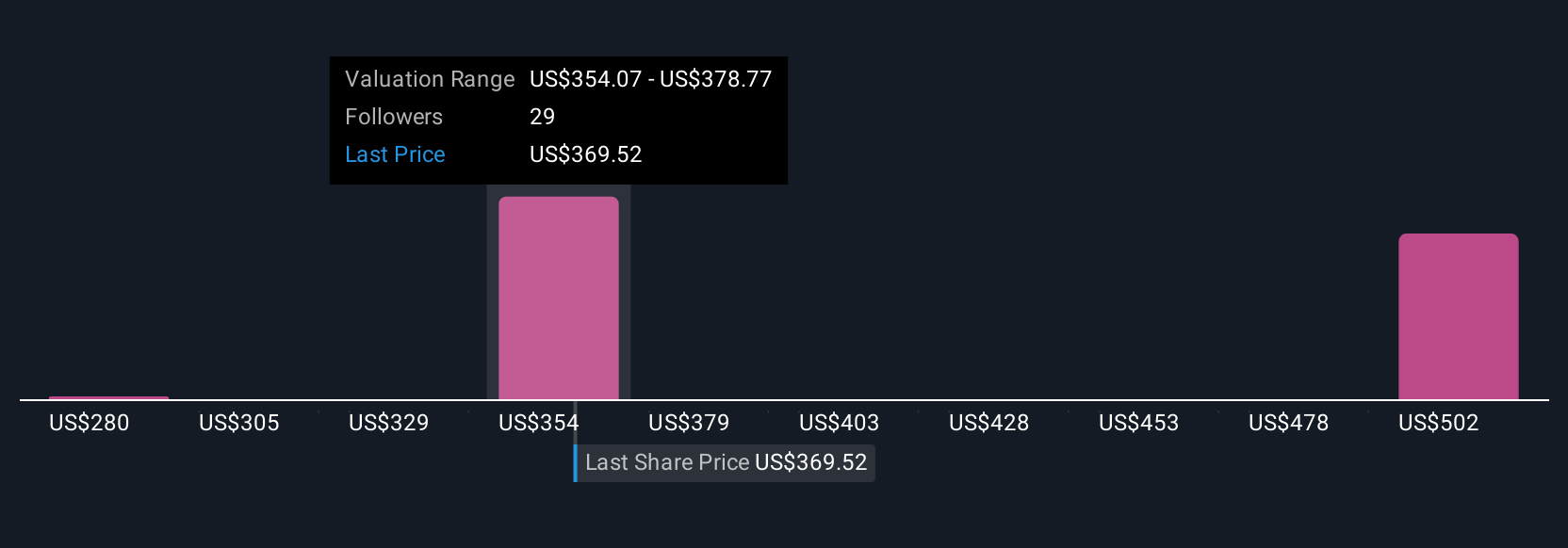

Five community member fair value estimates for Cummins range widely from US$280 to US$633, with the highest outlook nearly double the lowest. As industry trends pivot toward cleaner energy, some see potential, while others remain concerned about cyclical risks and market competition, check out these differing viewpoints to see where you align.

Explore 5 other fair value estimates on Cummins - why the stock might be worth as much as 27% more than the current price!

Build Your Own Cummins Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Cummins research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Cummins research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Cummins' overall financial health at a glance.

Looking For Alternative Opportunities?

Our top stock finds are flying under the radar-for now. Get in early:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 35 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CMI

Outstanding track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

932 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

139 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative