- United States

- /

- Construction

- /

- NYSE:ACM

AECOM (ACM) Valuation Check After New 10-Year FAA Infrastructure Contract Win

Reviewed by Simply Wall St

AECOM (ACM) just landed a fresh 10 year IDIQ contract from the Federal Aviation Administration, giving it a long runway of potential task orders tied to critical air traffic infrastructure upgrades.

See our latest analysis for AECOM.

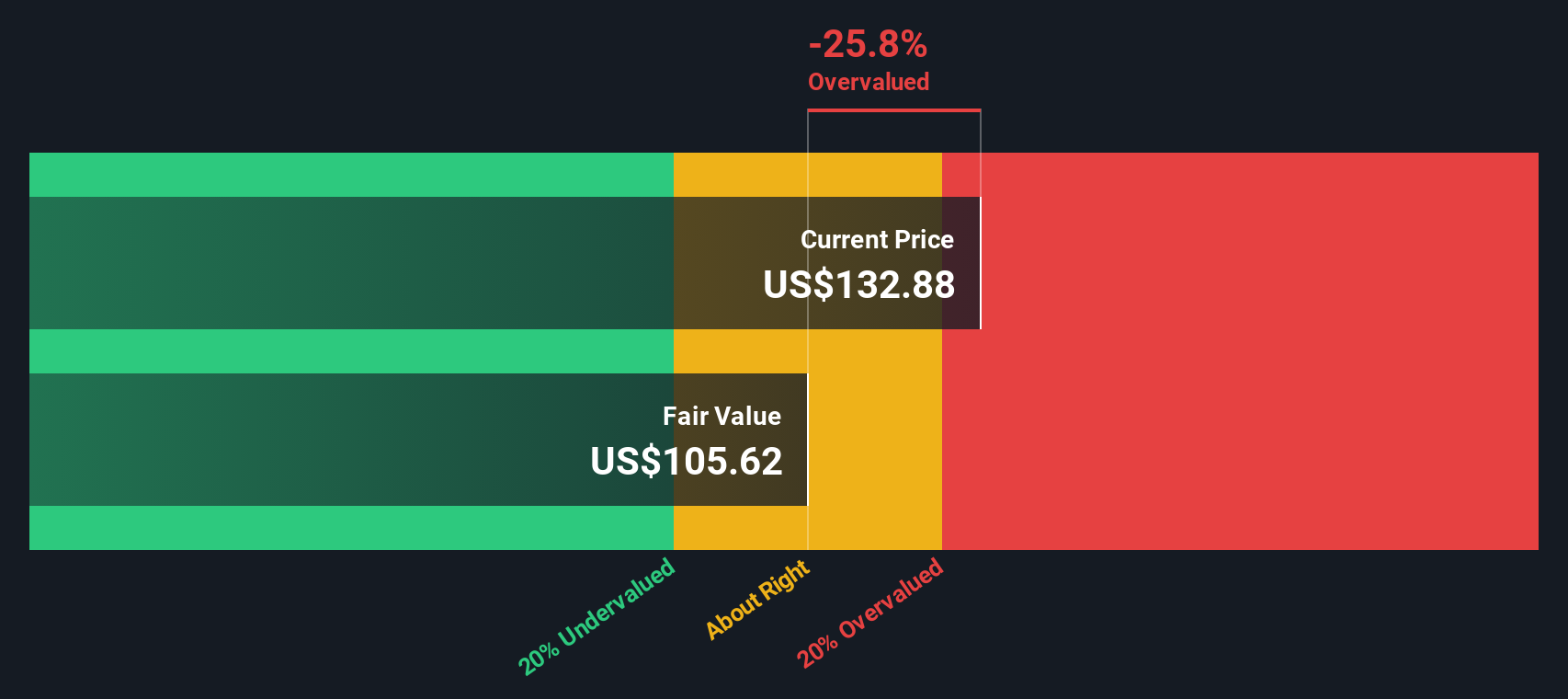

The contract drops at a time when AECOM’s share price has slid to about $98.85, with a sharp 1 month share price return of minus 25.52 percent, but a resilient 5 year total shareholder return of 114.46 percent suggesting longer term momentum is still intact.

If this FAA win has you thinking more broadly about infrastructure and defense exposure, it is worth exploring aerospace and defense stocks as potential companions to AECOM in your watchlist.

With shares now more than 45 percent below the Street’s average target but still boasting strong multi year returns, is AECOM quietly undervalued after this FAA win, or is the market already pricing in that future growth?

Most Popular Narrative Narrative: 31% Undervalued

With AECOM last closing at $98.85, the most followed narrative pegs fair value meaningfully higher at about $143, framing that FAA win in a much richer context.

Strategic, ongoing investment in digital solutions and AI is already showing positive margin impact and is projected to materially enhance operational efficiency, boost utilization, and further support earnings growth in the next 2 to 3 years.

Curious how steady revenue assumptions, firmer margins and a punchy future earnings multiple combine into that valuation gap? The full narrative lays out the playbook in detail.

Result: Fair Value of $143.33 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, AECOM’s heavy reliance on government infrastructure budgets, along with rising wage and compliance costs, could easily pressure margins and blunt that upside narrative.

Find out about the key risks to this AECOM narrative.

Another Angle on Valuation

Our DCF model tells a colder story, putting AECOM’s fair value closer to $83.62. This makes today’s $98.85 price look overvalued rather than discounted. If cash flows are worth less than the narrative implies, is the recent share price slide really a buying window or an early warning?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out AECOM for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 903 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own AECOM Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a personalized view in just minutes: Do it your way.

A good starting point is our analysis highlighting 5 key rewards investors are optimistic about regarding AECOM.

Looking for more investment ideas?

Do not stop with a single infrastructure name. Sharpen your edge by using the Simply Wall St screener to uncover focused opportunities across themes and sectors.

- Capture potential mispricings by reviewing these 903 undervalued stocks based on cash flows where solid cash flow stories might still be trading at a discount.

- Ride structural shifts in healthcare by scanning these 30 healthcare AI stocks for companies pairing medical expertise with powerful AI engines.

- Tap into digital financial disruption by assessing these 80 cryptocurrency and blockchain stocks shaping payments, custody, and blockchain infrastructure worldwide.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ACM

AECOM

Provides professional infrastructure consulting services for governments, businesses, and organizations internationally.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)