Advertisement

Mike Popielec became the CEO of Ultralife Corporation (NASDAQ:ULBI) in 2010, and we think it's a good time to look at the executive's compensation against the backdrop of overall company performance. This analysis will also assess whether Ultralife pays its CEO appropriately, considering recent earnings growth and total shareholder returns.

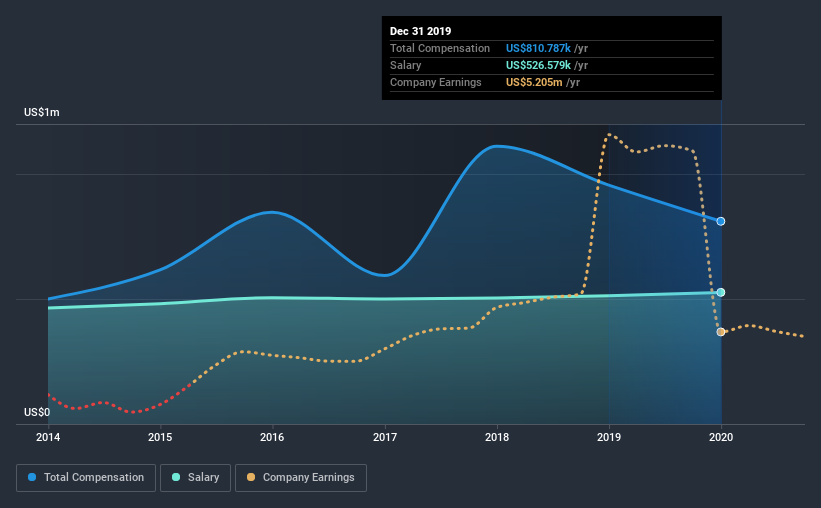

View our latest analysis for Ultralife

Comparing Ultralife Corporation's CEO Compensation With the industry

According to our data, Ultralife Corporation has a market capitalization of US$105m, and paid its CEO total annual compensation worth US$811k over the year to December 2019. That's a notable decrease of 15% on last year. We note that the salary portion, which stands at US$526.6k constitutes the majority of total compensation received by the CEO.

On comparing similar-sized companies in the industry with market capitalizations below US$200m, we found that the median total CEO compensation was US$441k. This suggests that Mike Popielec is paid more than the median for the industry. Furthermore, Mike Popielec directly owns US$1.8m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2019 | 2018 | Proportion (2019) |

| Salary | US$527k | US$513k | 65% |

| Other | US$284k | US$443k | 35% |

| Total Compensation | US$811k | US$956k | 100% |

On an industry level, around 31% of total compensation represents salary and 69% is other remuneration. Ultralife is paying a higher share of its remuneration through a salary in comparison to the overall industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Ultralife Corporation's Growth Numbers

Over the last three years, Ultralife Corporation has shrunk its earnings per share by 6.2% per year. Its revenue is up 13% over the last year.

Few shareholders would be pleased to read that EPS have declined. There's no doubt that the silver lining is that revenue is up. But it isn't sufficiently fast growth to overlook the fact that EPS has gone backwards over three years. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Ultralife Corporation Been A Good Investment?

Ultralife Corporation has not done too badly by shareholders, with a total return of 6.0%, over three years. But they would probably prefer not to see CEO compensation far in excess of the median.

In Summary...

As previously discussed, Mike is compensated more than what is normal for CEOs of companies of similar size, and which belong to the same industry. Meanwhile, EPS has not been growing sufficiently to impress us, over the last three years. And while shareholder returns have been respectable, they have hardly been superb. So you may want to delve deeper, because we don't think the amount Mike makes is justifiable.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. We did our research and spotted 1 warning sign for Ultralife that investors should look into moving forward.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

When trading Ultralife or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NasdaqGM:ULBI

Ultralife

Designs, manufactures, installs, and maintains power, and communication and electronics systems worldwide.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|28.9% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|46.3% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|35.8% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|56.1% undervalued

AX

Community Contributor