Advertisement

- United States

- /

- Real Estate

- /

- NYSE:CWK

US Stocks Estimated To Be Trading Below Intrinsic Value In December 2024

Simply Wall St

Reviewed by Simply Wall St

As of December 2024, the United States stock market is experiencing a remarkable surge, with the Nasdaq Composite surpassing the 20,000 mark for the first time thanks to a rally in major technology stocks. Amidst this bullish environment, identifying stocks trading below their intrinsic value can provide investors with opportunities to capitalize on potential growth. In such a climate, understanding fundamental analysis and assessing intrinsic value becomes crucial for investors aiming to make informed decisions about potentially undervalued stocks.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Clear Secure (NYSE:YOU) | $27.38 | $53.40 | 48.7% |

| UMB Financial (NasdaqGS:UMBF) | $124.97 | $244.29 | 48.8% |

| West Bancorporation (NasdaqGS:WTBA) | $23.94 | $46.42 | 48.4% |

| Equity Bancshares (NYSE:EQBK) | $47.67 | $92.84 | 48.7% |

| U.S. Physical Therapy (NYSE:USPH) | $95.66 | $187.03 | 48.9% |

| First Advantage (NasdaqGS:FA) | $19.81 | $39.49 | 49.8% |

| DoubleVerify Holdings (NYSE:DV) | $20.77 | $41.28 | 49.7% |

| VSE (NasdaqGS:VSEC) | $115.51 | $226.68 | 49% |

| Carter Bankshares (NasdaqGS:CARE) | $19.30 | $38.28 | 49.6% |

| Marcus & Millichap (NYSE:MMI) | $41.47 | $81.20 | 48.9% |

Underneath we present a selection of stocks filtered out by our screen.

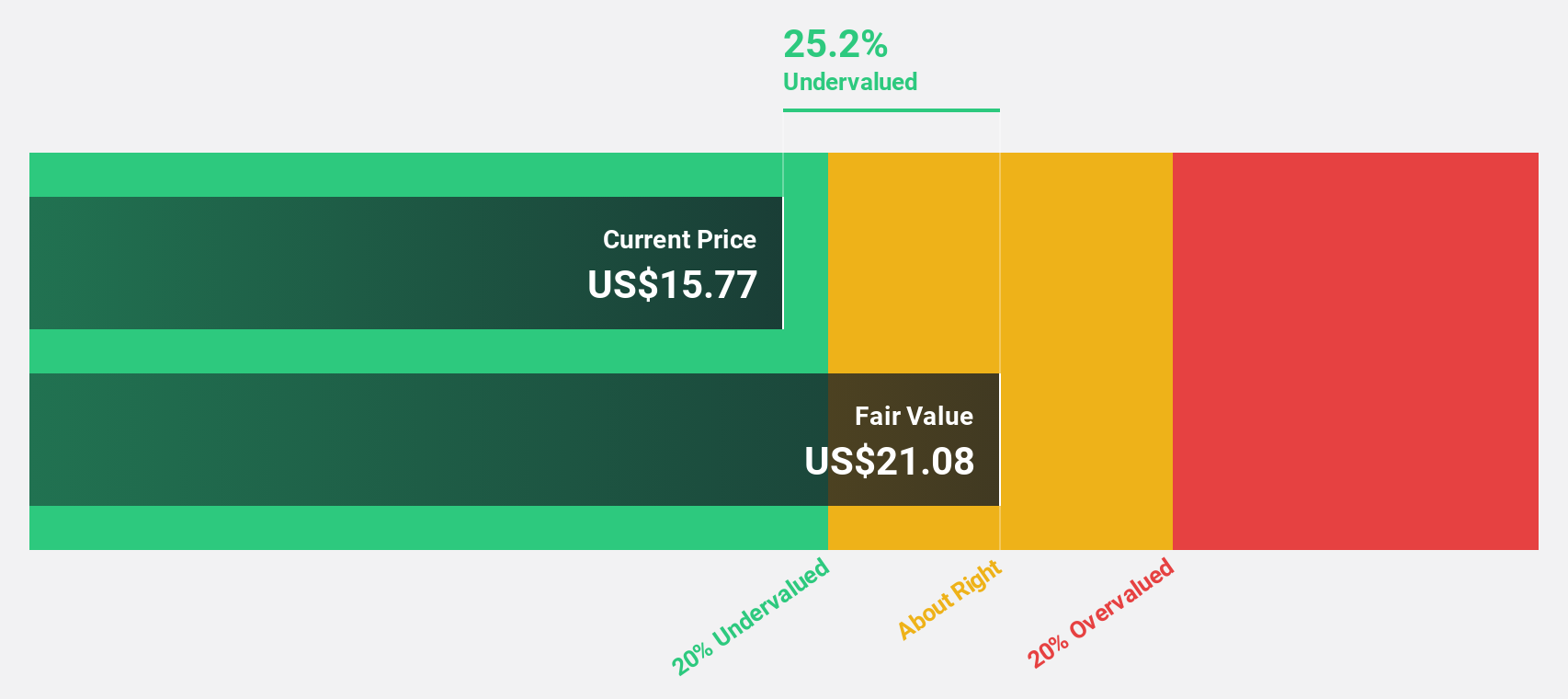

Rocket Lab USA (NasdaqCM:RKLB)

Overview: Rocket Lab USA, Inc. is a space company offering launch services and space systems solutions for the space and defense industries, with a market cap of approximately $11.42 billion.

Operations: The company's revenue is derived from two main segments: Space Systems, generating $272.33 million, and Launch Services, contributing $91.49 million.

Estimated Discount To Fair Value: 19.2%

Rocket Lab USA is trading at US$23.35, below its estimated fair value of US$28.89, indicating it may be undervalued based on discounted cash flow analysis. Despite recent volatility and shareholder dilution, the company is poised for significant revenue growth at 30.4% annually, surpassing market averages. Recent contracts with the U.S. Department of Commerce and defense sectors highlight Rocket Lab's strategic position in space-grade technology development, potentially enhancing future cash flows as it scales operations to meet demand.

- Our earnings growth report unveils the potential for significant increases in Rocket Lab USA's future results.

- Take a closer look at Rocket Lab USA's balance sheet health here in our report.

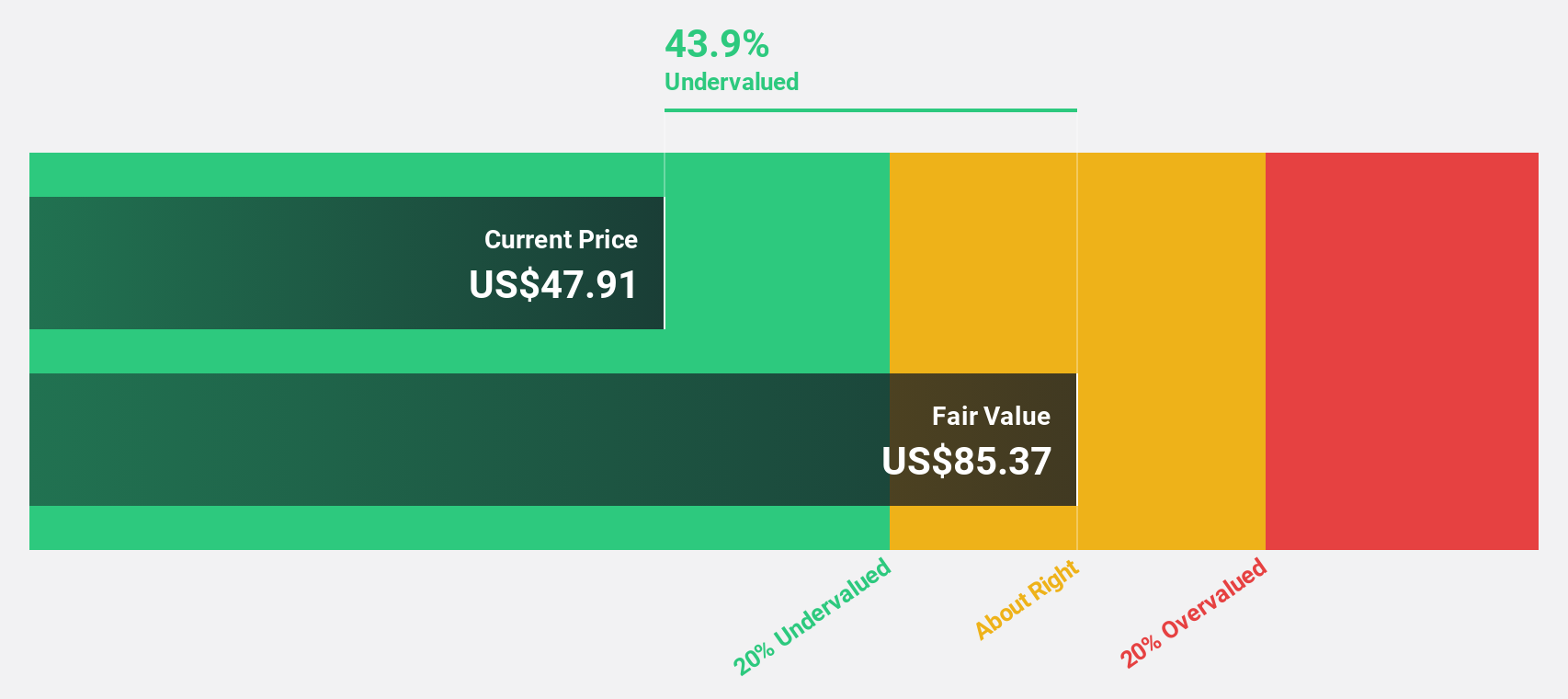

Symbotic (NasdaqGM:SYM)

Overview: Symbotic Inc., with a market cap of $15.72 billion, is an automation technology company that develops technologies to enhance operating efficiencies in modern warehouses.

Operations: The company's revenue is primarily derived from its Industrial Automation & Controls segment, which generated $1.79 billion.

Estimated Discount To Fair Value: 43.2%

Symbotic, currently trading at US$26.68, is significantly undervalued with an estimated fair value of US$46.94 based on discounted cash flow analysis. Despite recent legal challenges and delayed SEC filings, the company reported substantial revenue growth to US$1.82 billion for the fiscal year 2024. Forecasts suggest a robust annual revenue growth rate of 20.8%, exceeding market averages, with profitability expected within three years as it expands internationally into markets like Mexico through strategic partnerships with major retailers like Walmart de Mexico y Centroamerica.

- The growth report we've compiled suggests that Symbotic's future prospects could be on the up.

- Get an in-depth perspective on Symbotic's balance sheet by reading our health report here.

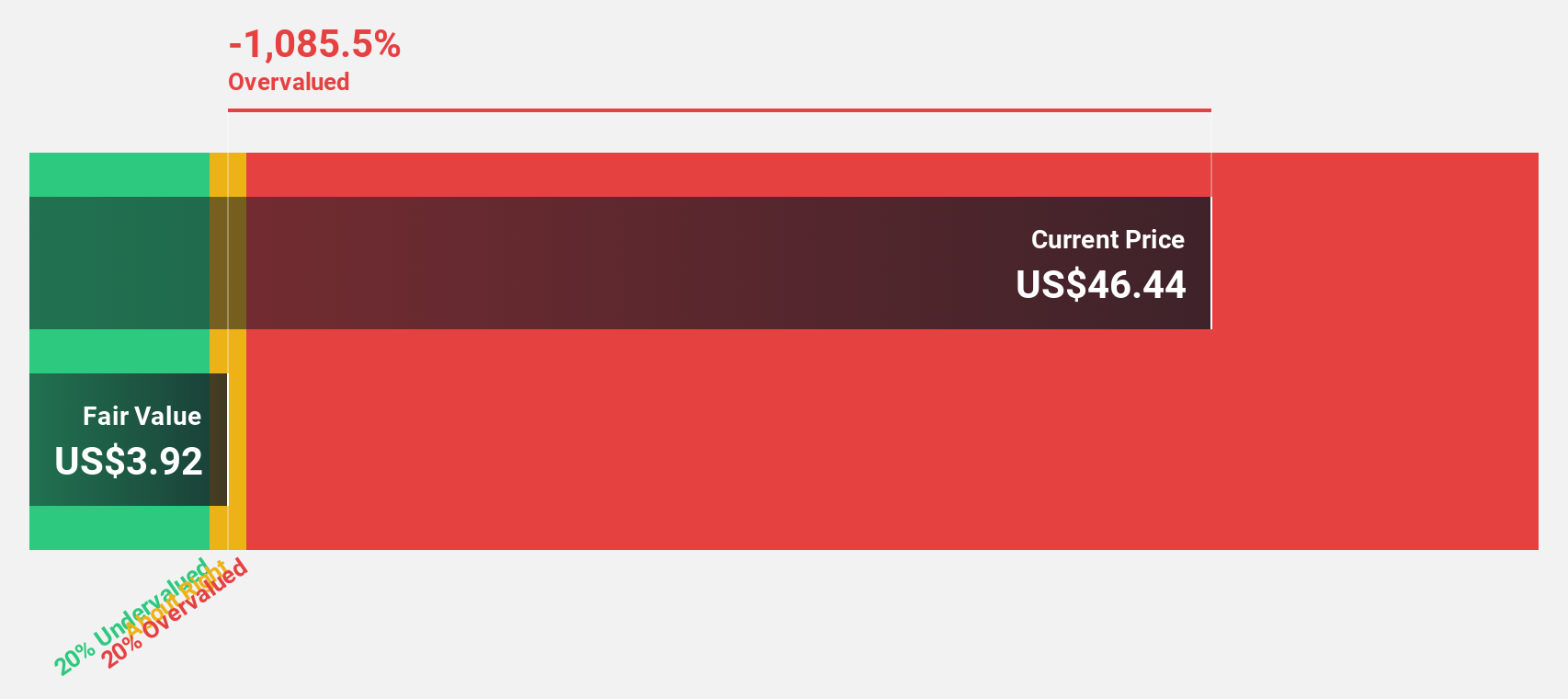

Cushman & Wakefield (NYSE:CWK)

Overview: Cushman & Wakefield plc, operating under its brand, offers commercial real estate services across the United States, Australia, the United Kingdom, and internationally with a market cap of $3.47 billion.

Operations: The company's revenue segments are comprised of $1.46 billion from APAC, $950.80 million from EMEA, and $6.96 billion from the Americas.

Estimated Discount To Fair Value: 17.9%

Cushman & Wakefield, trading at US$15.29, is undervalued compared to its fair value estimate of US$18.63 based on discounted cash flow analysis. The company recently became profitable, reporting a net income of US$33.7 million for Q3 2024, reversing a net loss from the previous year. While earnings are expected to grow significantly at 27% annually, revenue growth is projected to lag behind market averages at 5.8% per year.

- Our expertly prepared growth report on Cushman & Wakefield implies its future financial outlook may be stronger than recent results.

- Navigate through the intricacies of Cushman & Wakefield with our comprehensive financial health report here.

Taking Advantage

- Delve into our full catalog of 193 Undervalued US Stocks Based On Cash Flows here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CWK

Cushman & Wakefield

Provides commercial real estate services under the Cushman & Wakefield brand in the Americas, Europe, Middle East, Africa, and Asia Pacific.

Undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

77 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

91 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

928 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative