- United States

- /

- Electrical

- /

- NasdaqCM:OESX

Here's Why Orion Energy Systems (NASDAQ:OESX) Can Afford Some Debt

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Orion Energy Systems, Inc. (NASDAQ:OESX) does carry debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Orion Energy Systems

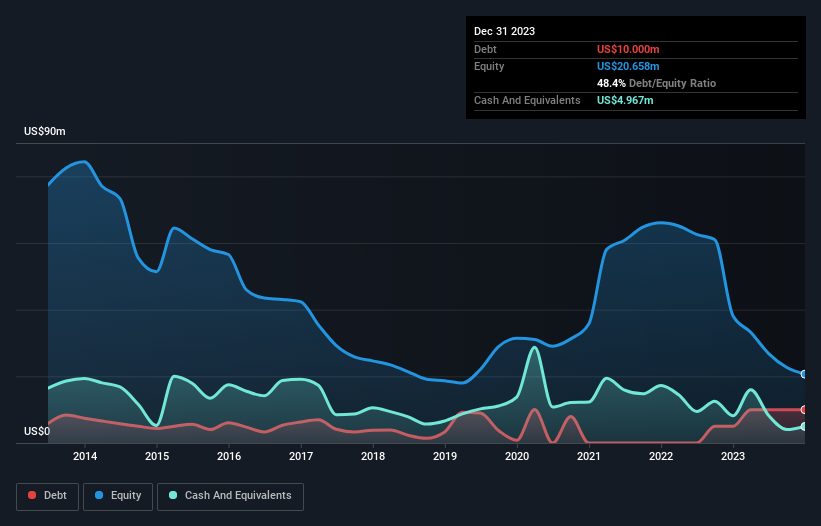

What Is Orion Energy Systems's Net Debt?

As you can see below, at the end of December 2023, Orion Energy Systems had US$10.0m of debt, up from US$5.00m a year ago. Click the image for more detail. On the flip side, it has US$4.97m in cash leading to net debt of about US$5.03m.

How Strong Is Orion Energy Systems' Balance Sheet?

The latest balance sheet data shows that Orion Energy Systems had liabilities of US$30.7m due within a year, and liabilities of US$14.1m falling due after that. On the other hand, it had cash of US$4.97m and US$17.4m worth of receivables due within a year. So its liabilities total US$22.4m more than the combination of its cash and short-term receivables.

This deficit is considerable relative to its market capitalization of US$30.9m, so it does suggest shareholders should keep an eye on Orion Energy Systems' use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Orion Energy Systems's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Over 12 months, Orion Energy Systems reported revenue of US$86m, which is a gain of 10%, although it did not report any earnings before interest and tax. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

Caveat Emptor

Over the last twelve months Orion Energy Systems produced an earnings before interest and tax (EBIT) loss. Indeed, it lost a very considerable US$13m at the EBIT level. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. Another cause for caution is that is bled US$8.2m in negative free cash flow over the last twelve months. So in short it's a really risky stock. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 3 warning signs for Orion Energy Systems you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:OESX

Orion Energy Systems

Researches, designs, develops, manufactures, markets, sells, installs, and implements energy management systems for commercial office and retail, area lighting, industrial applications, and government in North America and Germany.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Community Narratives