Advertisement

- United States

- /

- Machinery

- /

- NasdaqGM:HLMN

We Ran A Stock Scan For Earnings Growth And Hillman Solutions (NASDAQ:HLMN) Passed With Ease

The excitement of investing in a company that can reverse its fortunes is a big draw for some speculators, so even companies that have no revenue, no profit, and a record of falling short, can manage to find investors. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like Hillman Solutions (NASDAQ:HLMN). While profit isn't the sole metric that should be considered when investing, it's worth recognising businesses that can consistently produce it.

Hillman Solutions' Improving Profits

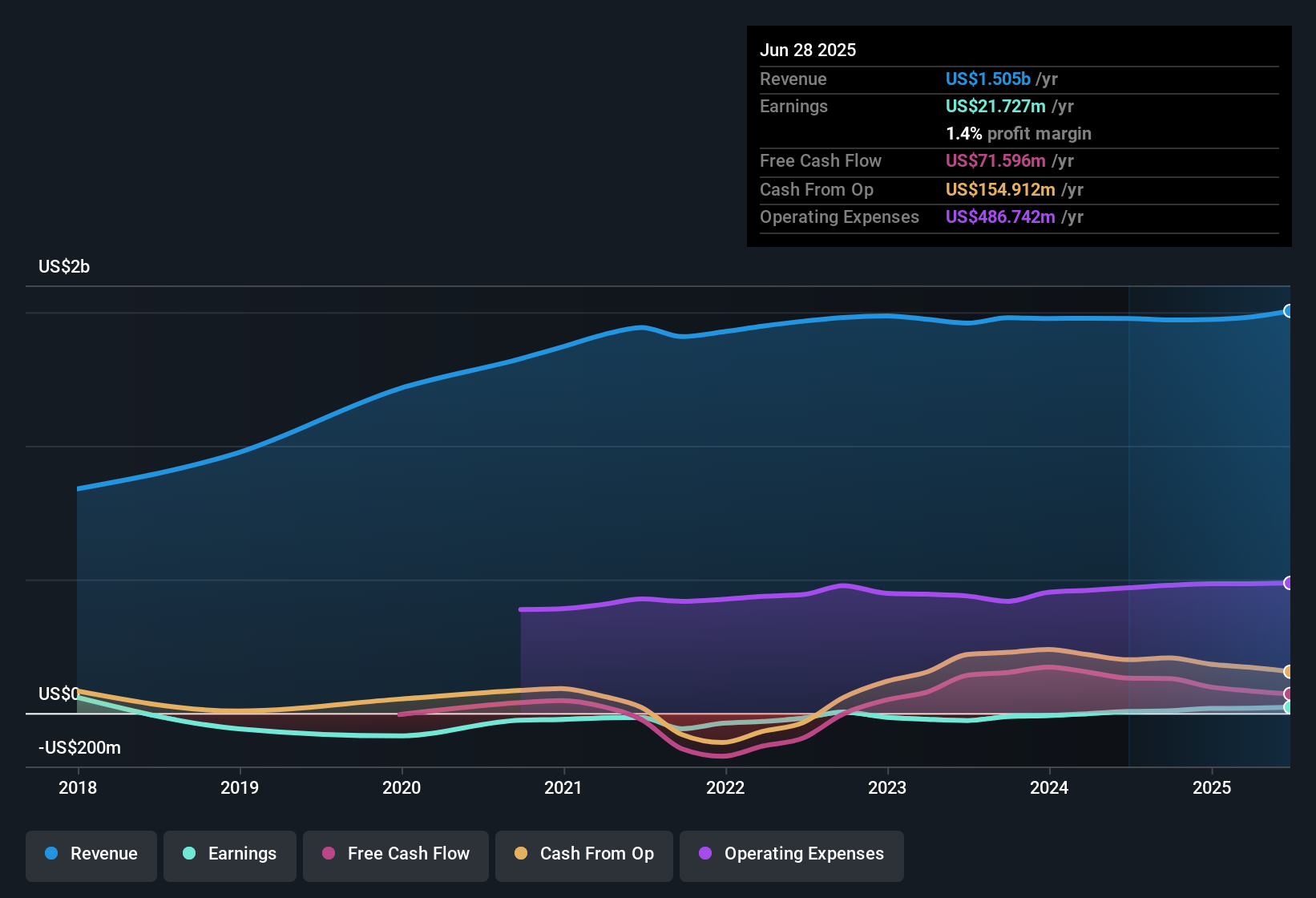

In business, profits are a key measure of success; and share prices tend to reflect earnings per share (EPS) performance. So for many budding investors, improving EPS is considered a good sign. It is awe-striking that Hillman Solutions' EPS went from US$0.03 to US$0.11 in just one year. When you see earnings grow that quickly, it often means good things ahead for the company.

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it's a great way for a company to maintain a competitive advantage in the market. It was a year of stability for Hillman Solutions as both revenue and EBIT margins remained have been flat over the past year. That's not bad, but it doesn't point to ongoing future growth, either.

You can take a look at the company's revenue and earnings growth trend, in the chart below. Click on the chart to see the exact numbers.

See our latest analysis for Hillman Solutions

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of Hillman Solutions' forecast profits?

Are Hillman Solutions Insiders Aligned With All Shareholders?

Investors are always searching for a vote of confidence in the companies they hold and insider buying is one of the key indicators for optimism on the market. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. Of course, we can never be sure what insiders are thinking, we can only judge their actions.

We did see some selling in the last twelve months, but that's insignificant compared to the whopping US$993k that the CFO & Treasurer, Robert Kraft spent acquiring shares. The average price paid was about US$7.09. Big purchases like that are well worth noting, especially for those who like to follow the insider money.

The good news, alongside the insider buying, for Hillman Solutions bulls is that insiders (collectively) have a meaningful investment in the stock. To be specific, they have US$20m worth of shares. That's a lot of money, and no small incentive to work hard. While their ownership only accounts for 1.0%, this is still a considerable amount at stake to encourage the business to maintain a strategy that will deliver value to shareholders.

While insiders are apparently happy to hold and accumulate shares, that is just part of the big picture. The cherry on top is that the CEO, JMA Adinolfi is paid comparatively modestly to CEOs at similar sized companies. The median total compensation for CEOs of companies similar in size to Hillman Solutions, with market caps between US$1.0b and US$3.2b, is around US$5.5m.

The CEO of Hillman Solutions only received US$1.7m in total compensation for the year ending December 2024. First impressions seem to indicate a compensation policy that is favourable to shareholders. While the level of CEO compensation shouldn't be the biggest factor in how the company is viewed, modest remuneration is a positive, because it suggests that the board keeps shareholder interests in mind. It can also be a sign of a culture of integrity, in a broader sense.

Is Hillman Solutions Worth Keeping An Eye On?

Hillman Solutions' earnings per share growth have been climbing higher at an appreciable rate. To sweeten the deal, insiders have significant skin in the game with one even acquiring more. This quick rundown suggests that the business may be of good quality, and also at an inflection point, so maybe Hillman Solutions deserves timely attention. Don't forget that there may still be risks. For instance, we've identified 1 warning sign for Hillman Solutions that you should be aware of.

Keen growth investors love to see insider activity. Thankfully, Hillman Solutions isn't the only one. You can see a a curated list of companies which have exhibited consistent growth accompanied by high insider ownership.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if Hillman Solutions might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:HLMN

Hillman Solutions

Provides hardware-related products and related merchandising services in the United States, Canada, Mexico, Latin America, and the Caribbean.

Solid track record and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.9% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|4.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|39.4% undervalued

TR

Community Contributor