- United States

- /

- Trade Distributors

- /

- NasdaqCM:CAPS

Capstone Holding (NASDAQ:CAPS) Is Scaling Up In Building Materials With Smart M&A And Growing Profitability

Sponsored Content

Key Takeaways

- Capstone is building a scalable platform in specialty construction materials, focusing on thin veneer masonry in the U.S. Midwest and Northeast.

- With a strategy of tuck-in acquisitions, innovative proprietary products, and regional growth, revenue could triple by 2030.

- Operational improvements and strong brand traction are driving better margins and positioning Capstone for scalable growth.

- The fragmented market and opportunities to capitalize on scale-driven advantages give Capstone the potential to grow into a national leader in its space.

To follow this analysis and see a visual representation of the valuation, check out the narrative here! Scaling up in building materials with smart M&A and growing profitability

About Capstone Holding Corp.

Capstone Holding Corp. (NASDAQ: CAPS) is a specialty construction materials company focused on distributing natural and manufactured thin veneer stone and related masonry products. Its primary subsidiary, Instone, is a wholesale distributor that serves contractors, retailers, and construction professionals in the Northeast and Midwest U.S.

Formerly a biotech company, Capstone pivoted in 2022 to become a public platform for consolidating small building product suppliers. Its leadership team now includes distribution and M&A specialists with experience in fragmented industries.

The company operates in a niche of the construction supply chain that benefits from design trends favoring stone finishes and lightweight cladding solutions. Veneer products are commonly used in both residential and commercial renovations, providing Capstone with access to multiple end markets.

Catalysts

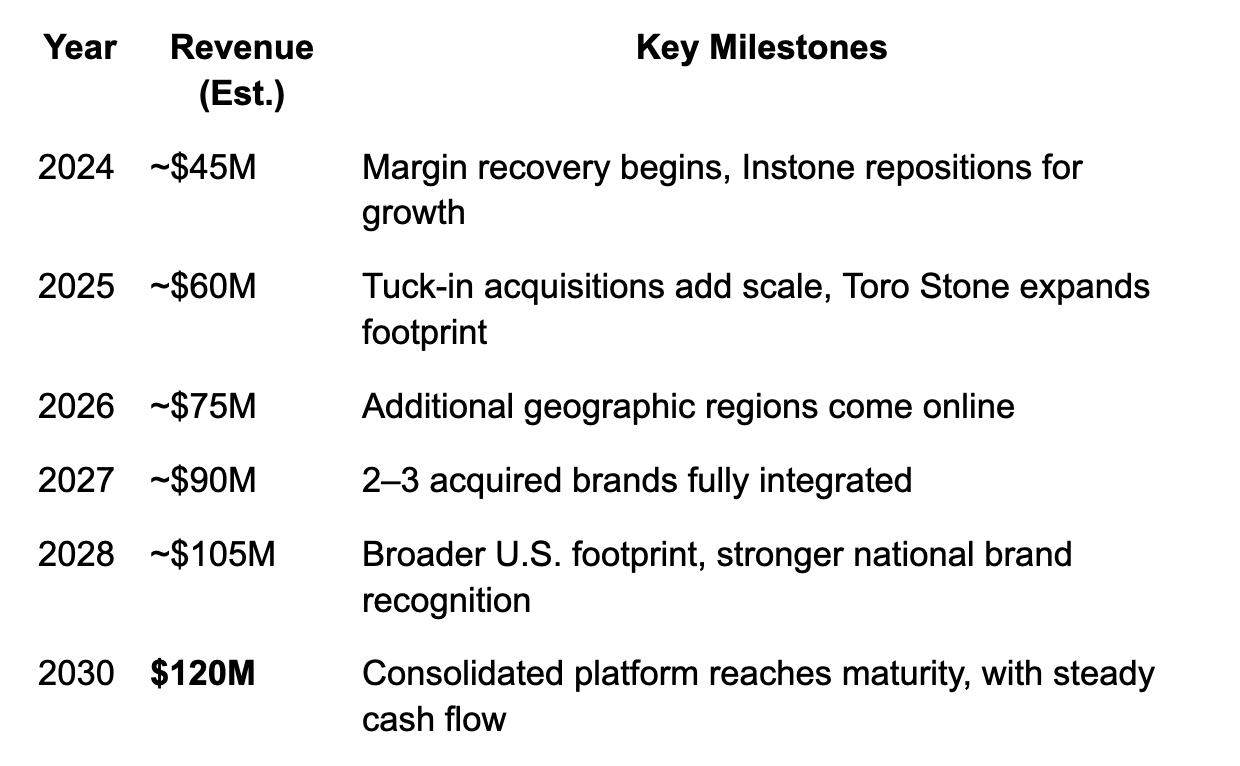

Capstone’s Plan to Triple Revenue by 2030

Capstone is targeting both organic and acquisition-led growth to expand its revenue base from ~$45 million in 2024 to $120 million by 2030. Some of its key initiatives include:

- Tuck-In Acquisitions

- Capstone is evaluating a steady pipeline of acquisition targets in the thin veneer and broader masonry supply space. These deals typically involve small regional distributors, and Capstone plans to pay 20–45% of deal value in stock or earn-outs, reducing upfront capital needs.

- Even 2–3 well-executed acquisitions could increase revenue by $30–50 million over the next few years.

- New Product Innovation

- New proprietary brands like Toro Stone are helping Capstone move up the value chain. These products not only carry higher margins but also differentiate the company’s offering from commodity stone suppliers.

- Toro’s modern “Linear Brick” format has gained attention from dealers and designers, and has already driven >30% YoY sales growth in its category.

- Geographic Expansion

- Capstone is actively expanding Instone’s reach into the Southeast and Mountain states, which offer year-round construction activity and less saturation by competitors. Establishing distribution in these regions unlocks a new customer base and increases logistical efficiency as the company scales nationally.

- Margin Recovery

- In 2024, Instone exited high-cost inventory acquired during the inflationary COVID period and cut SG&A costs by over $1.5 million. With this cleaner cost base and a more efficient structure, gross margins have recovered, and the company expects EBITDA margins to rise from ~5% to 7–8% over the next two years.

Large, Fragmented Market with Room to Scale

Capstone operates in a $675M+ stone veneer market that is projected to grow ~4% CAGR through 2032. Within that market, adhered thin veneer (Capstone’s specialty) is expanding fastest due to lower cost, ease of installation, and strong aesthetic appeal.

Most competitors in this space are small, privately held businesses with limited geographic coverage and little brand equity. Capstone is using its public listing to acquire and integrate these targets into a centralized but locally responsive platform.

This mirrors successful strategies used by players like SiteOne Landscape Supply, which consolidated regional landscaping suppliers into a national powerhouse. Capstone’s strategy is still in the early innings, offering plenty of space for growth.

5-Year Outlook: Steady Execution to $120M in Sales

This outlook assumes measured execution of Capstone’s M&A pipeline, modest organic growth, and continued traction for proprietary product lines.

This path assumes an average compound annual growth rate (CAGR) of ~21% through 2030, which is realistic given Capstone’s stated goal of reaching a $100M run-rate by 2026.

Valuation

Assumptions & Rationale

- 2030 Revenue: $120 million

- This estimate reflects a conservative case where Capstone grows revenue at ~21% annually from a $45 million base in 2024. It assumes mid-single-digit organic growth, 2–3 successful acquisitions, and steady market tailwinds. While Capstone has publicly targeted a $100M run-rate by 2026, this $120M figure assumes moderate execution and does not rely on aggressive M&A or booming construction activity.

- Net Profit Margin: 6%

- This reflects improving gross margins (via proprietary brands) and better SG&A leverage as the business scales. While some distributors operate at 3–5% net margins, Capstone’s margin-enhancing product mix and efficiency gains support this higher range. 6% also accounts for modest public company overhead and integration costs.

- 2030 Net Income: $7.2 million

- At a 6% margin on $120M of sales, Capstone would deliver ~$7.2M in bottom-line earnings. That would represent a significant turnaround from breakeven levels in 2023–2024, and aligns with management’s near-term EBITDA goals (e.g. $10M run-rate by 2026).

- Forward P/E Multiple: 15x

- While many building products distributors trade closer to 18–20x earnings, we apply a 15x multiple to account for Capstone’s micro-cap status, potential liquidity risk, and integration uncertainty. It’s a reasonable midpoint between value-oriented multiples (12–14x) and growth-oriented ones (18–22x).

- Some other building materials distributors like NYSE:SITE ($6bn market cap) and NYSE:BLDR ($13bn) trade on PE multiples of 26x and 13x, respectively. While they’re much bigger and more established than CAPS, their expected growth rates are lower. Plus, they show that M&A-driven growth in fragmented construction niches can command premium valuations. If execution is strong, a premium multiple could eventually be justified.

- 2030 Market Cap : $108 million

- Applying 15x to $7.2M in earnings implies a $108M equity value in 2030. This does not factor in any net debt/cash assumptions but presumes Capstone finances acquisitions conservatively via cash flow and stock.

- Discount Rate: 15%

- Small-cap stocks, especially those in early growth phases with acquisition risk, demand a higher return threshold. A 15% discount rate captures this risk premium and offers a cushion for uncertainty. If execution de-risks over time, future valuations could warrant a lower rate.

- Present Fair Value (2025): ~$53.7 million

- Discounting the $108M future value over 5 years at 15% gives a present value of just under $54 million. This compares favorably to Capstone’s current market cap of ~$10 million.

Risks

The following risk factors are based on information provided in Capstone’s recent SEC filings.

Dependence on Credit Facility: Capstone relies on a revolving credit facility to manage its liquidity. While it’s a useful resource, if the company doesn’t meet the required financial targets, it could limit its access to this funding.

Potential for Share Dilution: To fund growth or acquisitions, Capstone may issue additional shares. If managed well, this can support long-term growth, but too much dilution could reduce the value of existing shares if not paired with clear, tangible results.

Economic Sensitivity: Capstone’s business is tied to the construction industry, which can fluctuate with changes in housing activity, interest rates, and material costs. Economic slowdowns can reduce demand for products and impact profit margins, especially if costs remain high.

Stock Price Volatility: As a smaller company, Capstone’s stock may experience larger-than-average price swings. This is common with micro-cap stocks and can happen around key announcements, earnings reports, or shifts in market sentiment.

Risks of Acquisitions: Capstone’s growth strategy involves acquiring other businesses. While this can be a significant opportunity, delays, overpaying, or integration challenges could slow progress or impact overall value.

Competitive Industry: Capstone faces competition from both large national players and smaller, local businesses. Staying competitive requires ongoing innovation and a focus on meeting customer needs.

Reliance on Key Personnel: The company’s success depends on the leadership team and key employees. Losing any critical team members could impact Capstone’s ability to execute its strategy and grow effectively.

Conclusion

Capstone offers an under-the-radar growth opportunity in a niche building materials segment undergoing rapid modernization. With its current valuation implying minimal growth, even a conservative execution scenario presents meaningful upside.

Under this more measured scenario, Capstone reaches $120M in annual revenue by 2030, generates ~$7.2M in net income, and trades at ~15x earnings, resulting in a fair equity value of ~$108M by 2030. Valuing that in today’s dollars at a 15% discount rate gives a present value of $54m, more than 5x higher than where it trades today.

The story is still early, but the plan is clear: combine operational improvement, smart M&A, and proprietary products to turn a small regional distributor into a national brand. If Capstone keeps executing, patient investors may see the upside as margins expand and acquisitions compound.

Disclaimer

CMCVentures is an investor relations firm working with Capstone Holding. Simply Wall St has no position in the company(s) mentioned. These narratives are general in nature and explore scenarios and estimates created by the authors. These narrative do not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company’s future performance and are exploratory in the ideas they cover. The fair value estimate’s are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author’s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

This article has been sponsored by Capstone Holding (the Sponsor), which has paid Simply Wall St a fee for its publication on our platform and subsequent promotion. Any relationship between Simply Wall St and Capstone Holding does not influence how we produce or moderate other content on this website. The Sponsor has a financial interest in the subject matter of this narrative. Simply Wall St has not independently verified any statements or projections made by the author, and does not endorse or guarantee the accuracy or completeness of the information provided.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

CMCVentures

About NasdaqCM:CAPS

Capstone Holding

Engages in the distribution of masonry stone products in the Midwest and Northeast United States.

Moderate risk and slightly overvalued.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Trending Discussion