Stock Analysis

- United States

- /

- Banks

- /

- NYSE:BY

Byline Bancorp Leads Trio Of Undervalued Small Caps With Insider Buying In United States

Reviewed by Simply Wall St

Following a challenging week where the S&P 500 recorded significant declines, the spotlight on smaller-cap stocks grows as they show resilience amidst broader market pressures. In this context, identifying undervalued small caps like Byline Bancorp becomes particularly compelling, especially when insider buying suggests confidence in these companies' potential for growth.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Hanover Bancorp | 8.9x | 2.0x | 46.13% | ★★★★★☆ |

| Thryv Holdings | NA | 0.7x | 28.59% | ★★★★★☆ |

| AtriCure | NA | 2.8x | 46.29% | ★★★★★☆ |

| Franklin Financial Services | 9.3x | 1.9x | 34.77% | ★★★★☆☆ |

| Leggett & Platt | NA | 0.4x | 9.83% | ★★★★☆☆ |

| Chatham Lodging Trust | NA | 1.4x | 15.49% | ★★★★☆☆ |

| Citizens & Northern | 13.0x | 2.9x | 37.07% | ★★★☆☆☆ |

| Community West Bancshares | 18.7x | 2.9x | 42.25% | ★★★☆☆☆ |

| Alta Equipment Group | NA | 0.2x | -216.47% | ★★★☆☆☆ |

| Delek US Holdings | NA | 0.1x | -120.08% | ★★★☆☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

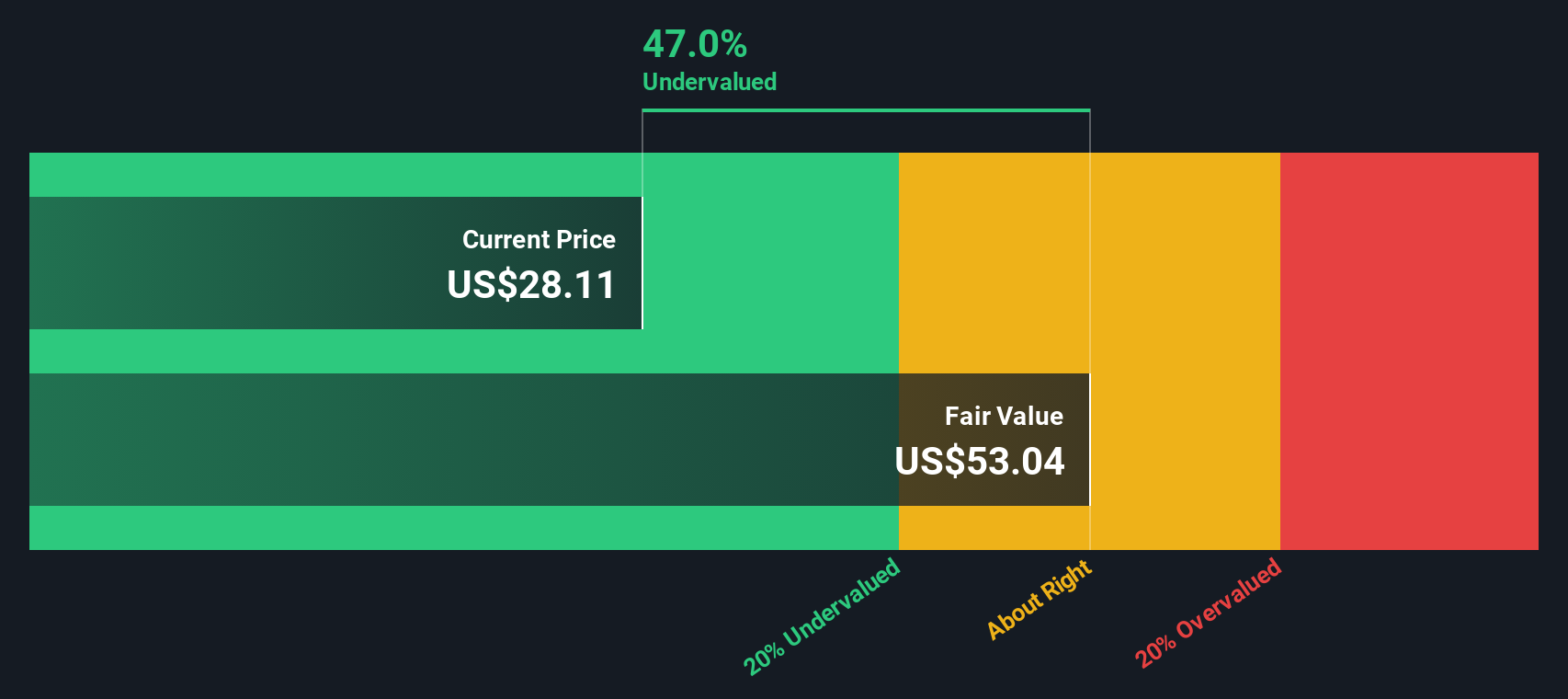

Byline Bancorp (NYSE:BY)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Byline Bancorp is a bank holding company primarily engaged in providing a range of banking services, with a market capitalization of approximately $366.62 million.

Operations: The company generates revenue through banking activities, with a consistent gross profit margin of 100%. Over recent years, the net income margin has improved, reaching 0.31% in the latest reporting period on revenues of $366.62 million.

PE: 10.6x

Byline Bancorp recently enhanced its financial stability by amending a credit agreement, extending a $15 million line of credit until May 2025. This move, coupled with a notable increase in net interest income to US$85.54 million and net income rising to US$30.44 million for Q1 2024, reflects solid operational performance. Despite earnings projected to dip slightly over the next three years, insider confidence remains evident as they recently purchased shares, signaling belief in the company's potential amidst market undervaluations.

- Click here and access our complete valuation analysis report to understand the dynamics of Byline Bancorp.

Gain insights into Byline Bancorp's past trends and performance with our Past report.

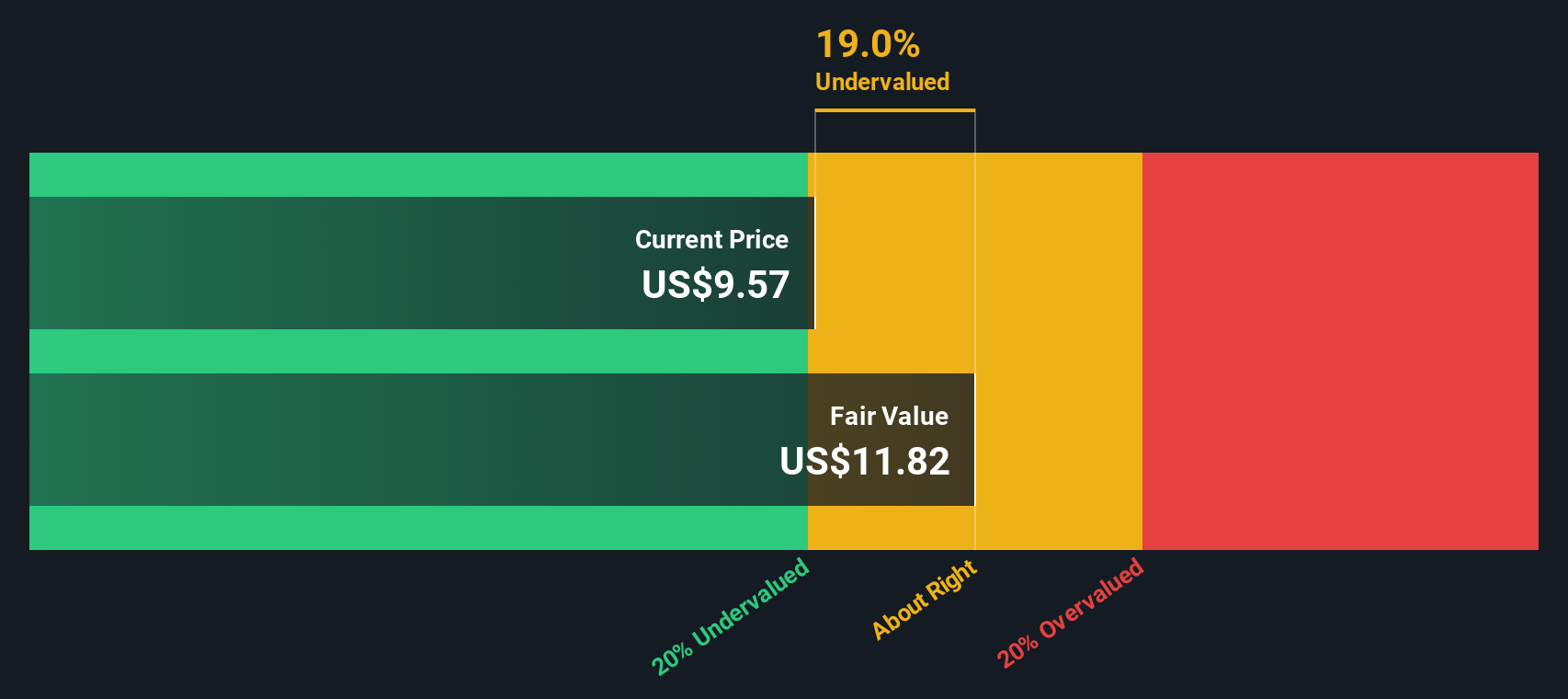

Leggett & Platt (NYSE:LEG)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Leggett & Platt is a diversified manufacturer specializing in engineered components and products found in homes, offices, automobiles, and commercial spaces with a market capitalization of approximately $4.65 billion.

Operations: The company generates revenue from three key segments: Bedding Products ($1.91 billion), Specialized Products ($1.28 billion), and Furniture, Flooring & Textile Products ($1.46 billion). Over recent periods, the gross profit margin has shown variability, with a notable figure of 22.07% in Q2 2015 but a decrease to approximately 17.83% by Q3 2024.

PE: -10.7x

Recently, Leggett & Platt has demonstrated notable insider confidence, with key executives purchasing shares, signaling a strong belief in the company's prospects. Amidst this backdrop, the firm has navigated a complex landscape marked by its removal and addition to different S&P indices and significant leadership changes with Karl G. Glassman reassuming CEO duties. Financially, despite a dip in quarterly dividends and earnings reflecting challenging conditions, their strategic focus on acquisitions and maintaining a solid credit stance underscores resilience and adaptability. These elements collectively suggest that Leggett & Platt is positioned for recovery and growth, making it an attractive consideration for those seeking potential amidst undervalued entities.

- Click here to discover the nuances of Leggett & Platt with our detailed analytical valuation report.

Explore historical data to track Leggett & Platt's performance over time in our Past section.

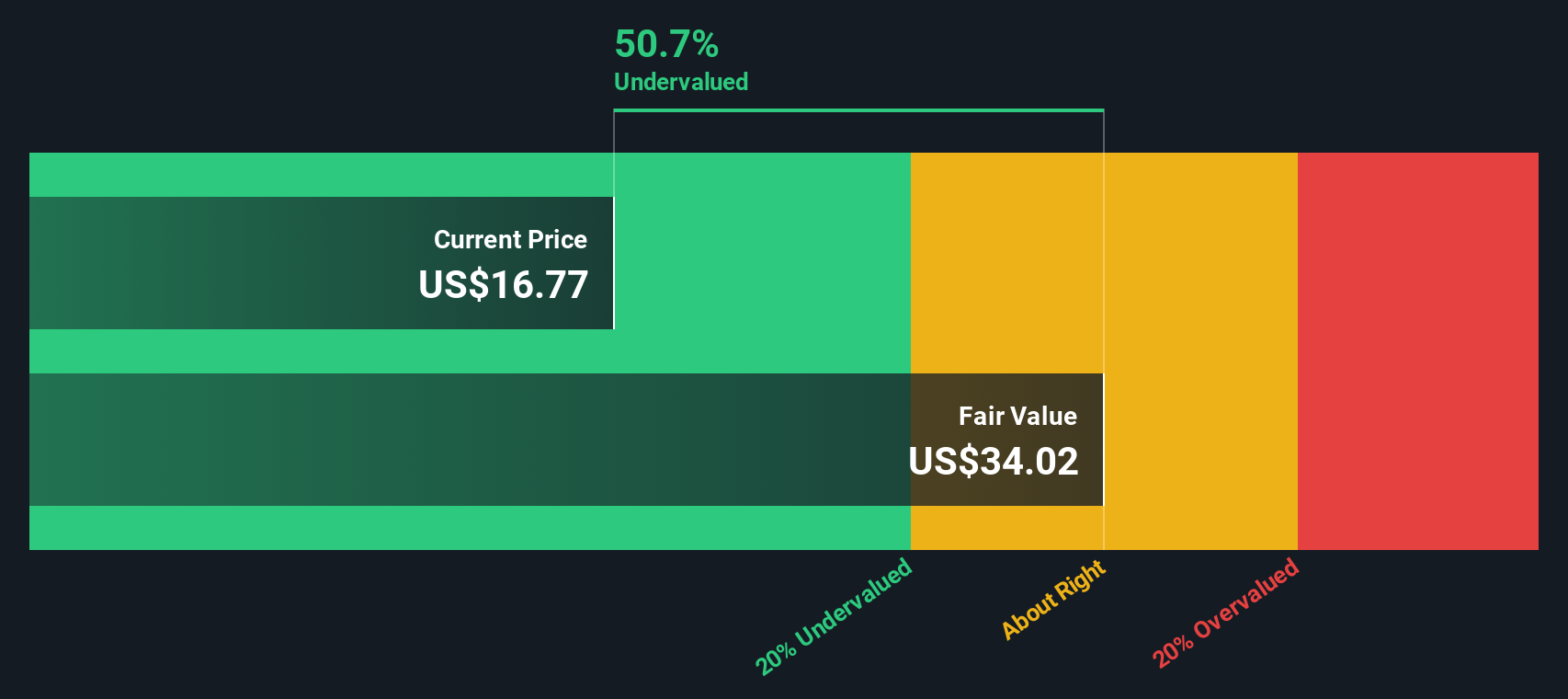

Provident Financial Services (NYSE:PFS)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Provident Financial Services is a financial institution offering traditional banking and other financial services, with a market capitalization of approximately $1.23 billion.

Operations: This entity generates a consistent gross profit margin of 100%, with revenue reaching $441.20 million as of the latest reporting period. Net income has fluctuated, most recently recorded at $119.94 million, reflecting a net income margin of approximately 27.17%.

PE: 11.2x

Provident Financial Services recently enhanced its governance by appointing new directors and executing strategic executive changes, signaling a robust organizational focus. With earnings projected to grow by 54.74% annually, their recent $225 million fixed-income offering strengthens financial foundations, appealing to those seeking firms with solid growth trajectories and proactive management. Insider confidence is evident from recent purchases, underscoring belief in the company’s future prospects amidst its current market undervaluation.

- Get an in-depth perspective on Provident Financial Services' performance by reading our valuation report here.

Learn about Provident Financial Services' historical performance.

Turning Ideas Into Actions

- Click here to access our complete index of 68 Undervalued US Small Caps With Insider Buying.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're helping make it simple.

Find out whether Byline Bancorp is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BY

Byline Bancorp

Operates as the bank holding company for Byline Bank that provides various banking products and services for small and medium sized businesses, commercial real estate and financial sponsors, and consumers in the United States.

Flawless balance sheet with solid track record.