Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:UBSI

A Look at United Bankshares’s (UBSI) Valuation Following Strong Q3 Results and Analyst Upgrade

Simply Wall St

Reviewed by Simply Wall St

United Bankshares (UBSI) saw its shares move higher after the company delivered third-quarter results that topped expectations. The company posted solid growth in both revenue and net interest income compared to the previous year.

See our latest analysis for United Bankshares.

The stronger than expected quarterly results gave United Bankshares an immediate boost, with the share price jumping 3.6% in a single day. That momentum follows a year where the 12-month total shareholder return is flat to slightly negative, even as management has highlighted record earnings and repurchased shares, and analysts have started to warm up to the stock. All together, the recent pop hints at growing optimism as the company continues to balance expense discipline with organic growth.

If this shift in sentiment has you searching for other compelling opportunities, now is a great moment to broaden your perspective and discover fast growing stocks with high insider ownership

So after UBSI’s strong quarter and a recent analyst upgrade, is this the window for investors to scoop up shares at an attractive valuation, or has the market already factored in the company’s brighter growth prospects?

Price-to-Earnings of 11.9x: Is it justified?

United Bankshares trades at a price-to-earnings (P/E) ratio of 11.9x, putting it at a slight premium to both the US Banks industry average and peer group. This suggests the stock is not trading at a bargain price relative to its sector peers.

The P/E ratio is a widely used measure, comparing the company’s current share price to its earnings per share. For banks, it reflects expectations for future profitability and growth. A higher P/E can be justified if the market anticipates stronger results ahead.

However, United Bankshares’ current multiple is above both the US Banks industry average (11.2x) and the peer group (11.4x). At the same time, the ratio is below the estimated fair P/E, which stands at 12.3x. This suggests there may still be some room for shares to move higher if earnings continue to impress investors.

Explore the SWS fair ratio for United Bankshares

Result: Price-to-Earnings of 11.9x (ABOUT RIGHT)

However, slowing one-year returns and revenue growth below 7% suggest that headwinds or weaker demand could quickly challenge the current optimism.

Find out about the key risks to this United Bankshares narrative.

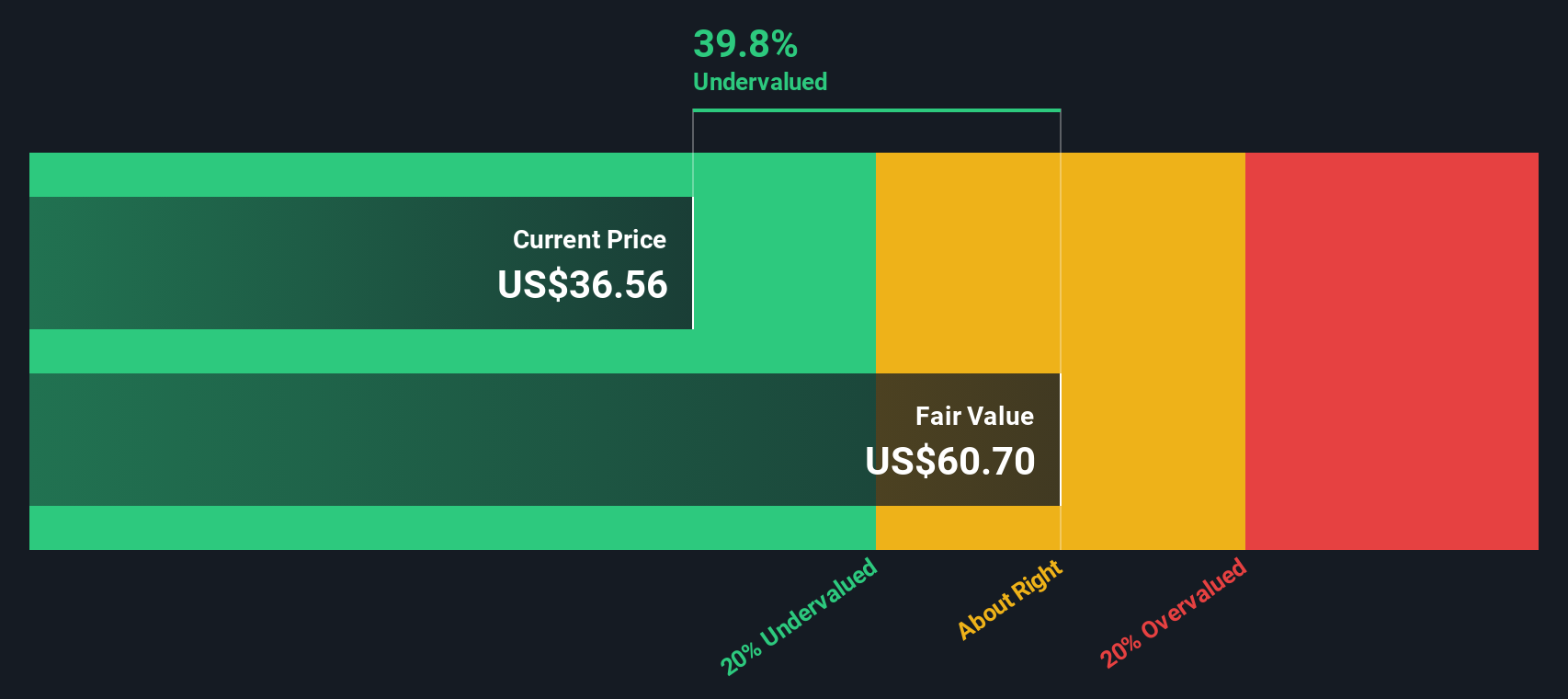

Another View: Discounted Cash Flow Tells a Different Story

The SWS DCF model offers a more optimistic angle and estimates United Bankshares’ fair value at $60.61 per share, nearly 40% higher than its recent trading price. This result is a sharp contrast to signals from its price-to-earnings ratio. Is the market missing something, or is this a value trap in disguise?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out United Bankshares for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own United Bankshares Narrative

If you see the story unfolding differently or want to dive deeper into the numbers yourself, you can shape your own view in just a few minutes. Do it your way

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding United Bankshares.

Looking for More Smart Investment Opportunities?

Step beyond the obvious and give yourself the edge in today's market. Some of the most interesting investment stories are only a click away.

- Turbocharge your search for long-term income by tapping into these 17 dividend stocks with yields > 3%, offering yields above 3% and historically stable payouts.

- Seize an early lead in technology with these 27 AI penny stocks, gaining attention for their breakthroughs and real-world advances in artificial intelligence.

- Ride the next big shift in digital finance by tracking these 80 cryptocurrency and blockchain stocks, as they power new blockchain solutions and future-proof portfolios.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:UBSI

United Bankshares

Through its subsidiaries, provides commercial and retail banking products and services in the United States.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor