Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:SRCE

1st Source (NASDAQ:SRCE) Has Announced That It Will Be Increasing Its Dividend To $0.34

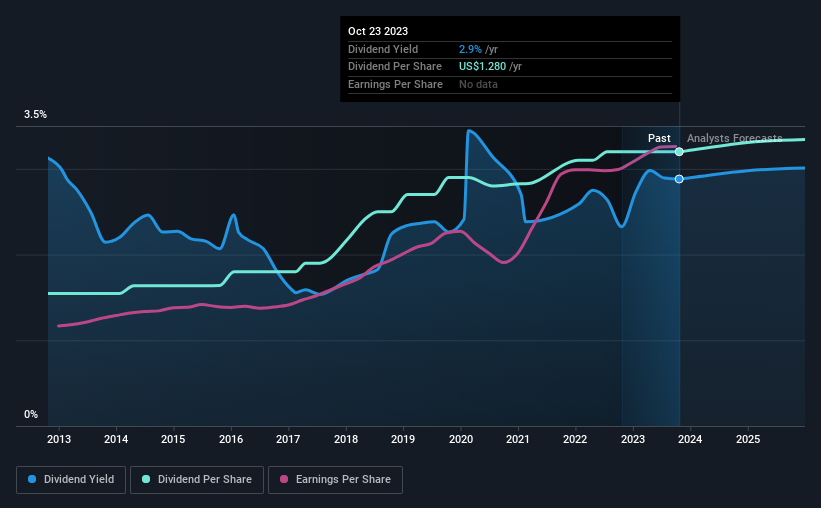

1st Source Corporation (NASDAQ:SRCE) will increase its dividend on the 15th of November to $0.34, which is 6.3% higher than last year's payment from the same period of $0.32. Although the dividend is now higher, the yield is only 2.9%, which is below the industry average.

See our latest analysis for 1st Source

1st Source's Payment Expected To Have Solid Earnings Coverage

Even a low dividend yield can be attractive if it is sustained for years on end.

1st Source has established itself as a dividend paying company with over 10 years history of distributing earnings to shareholders. While past records don't necessarily translate into future results, the company's payout ratio of 6.2% also shows that 1st Source is able to comfortably pay dividends.

Over the next 3 years, EPS is forecast to fall by 34.3%. However, as estimated by analysts, the future payout ratio could be 34% over the same time period, which we think the company can easily maintain.

1st Source Has A Solid Track Record

The company has an extended history of paying stable dividends. The annual payment during the last 10 years was $0.618 in 2013, and the most recent fiscal year payment was $1.28. This works out to be a compound annual growth rate (CAGR) of approximately 7.5% a year over that time. The dividend has been growing very nicely for a number of years, and has given its shareholders some nice income in their portfolios.

The Dividend Looks Likely To Grow

The company's investors will be pleased to have been receiving dividend income for some time. 1st Source has seen EPS rising for the last five years, at 11% per annum. 1st Source definitely has the potential to grow its dividend in the future with earnings on an uptrend and a low payout ratio.

1st Source Looks Like A Great Dividend Stock

Overall, a dividend increase is always good, and we think that 1st Source is a strong income stock thanks to its track record and growing earnings. The distributions are easily covered by earnings, and there is plenty of cash being generated as well. If earnings do fall over the next 12 months, the dividend could be buffeted a little bit, but we don't think it should cause too much of a problem in the long term. All in all, this checks a lot of the boxes we look for when choosing an income stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. As an example, we've identified 1 warning sign for 1st Source that you should be aware of before investing. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:SRCE

1st Source

Operates as the bank holding company for 1st Source Bank that provides commercial and consumer banking services, trust and wealth advisory services, and insurance products to individual and business clients in the United States.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3451.9% undervalued

50 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7104.2% overvalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.654.8% undervalued

34 followersusers have followed this narrative

2 commentsusers have commented on this narrative

16 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£161.9% undervalued

40 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

MO

Momentum_Panda_y9xg on Netflix ·

Netflix's Revenue Surge Will Hit 18% Despite Market Lows

Fair Value:US$158.7254.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’sMost Mispriced AI Story

Fair Value:US$7.551.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BR

browser on Space Exploration Technologies ·

SpaceX: A Sober Look at Catalysts, Risks, and Long‑Term Value After the IPO

Fair Value:US$0.4633.5k% overvalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7443.8% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.1% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

17 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17056.9% undervalued

50 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative