- United States

- /

- Banks

- /

- NasdaqCM:PCSB

PCSB Financial's (NASDAQ:PCSB) Shareholders Are Down 27% On Their Shares

Many investors define successful investing as beating the market average over the long term. But its virtually certain that sometimes you will buy stocks that fall short of the market average returns. We regret to report that long term PCSB Financial Corporation (NASDAQ:PCSB) shareholders have had that experience, with the share price dropping 27% in three years, versus a market return of about 46%. And the ride hasn't got any smoother in recent times over the last year, with the price 26% lower in that time. There was little comfort for shareholders in the last week as the price declined a further 4.4%.

View our latest analysis for PCSB Financial

There is no denying that markets are sometimes efficient, but prices do not always reflect underlying business performance. One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

Although the share price is down over three years, PCSB Financial actually managed to grow EPS by 79% per year in that time. Given the share price reaction, one might suspect that EPS is not a good guide to the business performance during the period (perhaps due to a one-off loss or gain). Or else the company was over-hyped in the past, and so its growth has disappointed.

It's worth taking a look at other metrics, because the EPS growth doesn't seem to match with the falling share price.

The modest 1.1% dividend yield is unlikely to be guiding the market view of the stock. We note that, in three years, revenue has actually grown at a 3.8% annual rate, so that doesn't seem to be a reason to sell shares. It's probably worth investigating PCSB Financial further; while we may be missing something on this analysis, there might also be an opportunity.

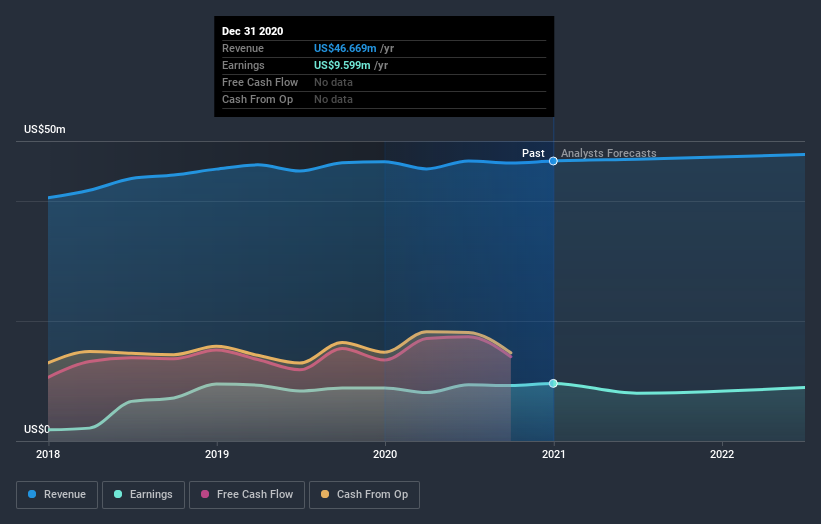

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

We like that insiders have been buying shares in the last twelve months. Even so, future earnings will be far more important to whether current shareholders make money. So it makes a lot of sense to check out what analysts think PCSB Financial will earn in the future (free profit forecasts).

A Different Perspective

Over the last year, PCSB Financial shareholders took a loss of 25%, including dividends. In contrast the market gained about 25%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. The three-year loss of 8% per year isn't as bad as the last twelve months, suggesting that the company has not been able to convince the market it has solved its problems. We would be wary of buying into a company with unsolved problems, although some investors will buy into struggling stocks if they believe the price is sufficiently attractive. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. To that end, you should be aware of the 1 warning sign we've spotted with PCSB Financial .

PCSB Financial is not the only stock insiders are buying. So take a peek at this free list of growing companies with insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

If you decide to trade PCSB Financial, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqCM:PCSB

PCSB Financial

PCSB Financial Corporation operates as the bank holding company for PCSB Bank that provides financial services to individuals and businesses in Putnam, Southern Dutchess, Rockland, and Westchester Counties in New York.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Community Narratives